JHVEPhoto

Financial Investment Thesis

Alphabet Inc. aka Google ( NASDAQ: GOOG, NASDAQ: GOOGL) continues to be an extremely lucrative and growth-oriented business, with the most current Q4 incomes report settling a strong 2023 for the company.

While development has actually slowed compared to pre-pandemic years, Alphabet’s companies stay appropriate within its their different sectors in spite of increasing competitive pressures from the similarity Apple ( AAPL), Microsoft ( MSFT) and Amazon ( AMZN).

Present appraisals appear to have not yet priced-in 2024 development with shares underestimated by 30% in my base-case computations.

For that reason, I rank Alphabet a tentative Buy at present time.

Business Photo

Alphabet Inc. is an innovation corporation that owns Google and numerous other business that run in different domains, such as web search, expert system, biotechnology, cloud computing, cybersecurity, and more.

Alphabet’s companies is Google, who run the world’s most popular online search engine and likewise provides product or services such as Gmail, Android, Google Cloud and more.

Alphabet likewise has an enormous collection of other companies under their umbrella. More current additions consist of Fitbit, Mandiant cyber security, Waymo self-governing driving taxis and even Verily, a life sciences and health care business.

Financial Moat– Thorough Analysis

Alphabet has a mega financial moat that is driven both by the variety and by the interconnectedness of their various organization systems in addition to what I view as some irreplicable intangible properties.

Alphabet’s core organization, Google Solutions, gain from a favorable feedback loop of more users producing more information which draws in more marketers hence creates more income.

This effective scale and network result has actually permitted Google Browse and YouTube to become definitely vital aspects of the web experience for the majority of users.

These network and scale impacts produces a high barrier to entry for rivals and a devoted user base for Alphabet.

While Microsoft’s Bing has actually taken the battle to Google Browse over the last twelve months, Google has actually started quickly incorporating their own AI and artificial intelligence into the Browse organization which must even the playing field significantly.

Google Browse as a company likewise takes pleasure in a market leading position within the market which the term to “google something” having actually ended up being understood throughout the world.

This strong brand name identity and combination into everyday terminology must not be ignored and highlights simply how effective of a position Google has actually developed for their flagship search item.

Google provides a range of other online services that match its core search and marketing companies, such as Gmail, Google Maps, Google Photos, Drive and Chrome.

These services improve the user experience and commitment, develop cross-selling and bundling chances, and create extra income streams for Alphabet.

Additionally, these services gather important user information that feed into Google’s expert system and artificial intelligence abilities, which enhance the quality and importance of its product or services.

I likewise see the Android os as producing genuine moatiness to Alphabet’s organization as a whole. Android is the world’s most popular mobile os, with a market share of over 70%

The os provides Alphabet a tactical benefit in the mobile area, as it enables the business to disperse its apps and services to billions of users and gadgets, and to monetize them through marketing and in-app purchases.

Android likewise allows Alphabet to cultivate an open and varied environment of designers, producers, and partners, who develop and provide a wide variety of applications, material, and hardware for Android users.

Additionally, Android assists Alphabet to counter the information supremacy danger from Apple, which has its own exclusive os, iOS.

The Google Cloud organization section likewise creates considerable moatiness thanks to its scale, development, and combination with other Google Solutions.

Google Cloud is a platform that provides cloud computing services, such as facilities (IaaS), platform (PaaS), information analytics, expert system, and software application (SaaS) services.

The platform takes on other significant cloud companies, such as Amazon Web Solutions and Microsoft Azure, in what has quickly end up being an enormously lucrative and competitive market.

I when again see Google Cloud taking advantage of the big and faithful user base of Google Solutions, which supplies it with information, feedback, and cross-selling chances.

Google Cloud likewise leverages its know-how and management in expert system and artificial intelligence. The combination of AI and artificial intelligence into Google Cloud will be an important action for the company to complete straight with Microsoft Azure and drive cloud adoption and distinction within business.

If the company drags in the abilities of their IaaS, PaaS and SaaS services, there is a genuine danger of the whole Google Cloud organization section having a hard time to grow even more in the future.

Lastly, Other Bets are a collection of Alphabet’s moonshot jobs and endeavors that run in different domains, such as self-driving innovation, life sciences, web gain access to, and cybersecurity.

A Few Of the most popular Other Bets are Waymo, Verily and Calico Other Bets’ financial moat originates from their development, vision, and capacity.

All of the Other Bets companies benefit straight from Alphabet’s monetary and technical resources, which allow them to experiment and scale.

Other Bets likewise have the prospective to create considerable worth and returns for Alphabet, if they prosper in their objectives and monetize their product or services.

Nevertheless, the keyword here is if they prosper. Thinking about the fundamental danger associated start-up companies, I can award no genuine moatiness to Alphabet from Other Bets as a sector.

In General, Google has an enormous and robust financial moat that is extremely hard to duplicate. The distinct network impacts produced by Google Solutions, Cloud and Other Bets interacting produces for an effective set of intangible properties and information which creates genuine competitive benefits for the company.

Monetary Analysis– Complete Year 2023

Alphabet has 5Y (FY23-FY19) typical ROA, ROE and ROIC of 16.75%, 23.31% and 20.53% respectively. These returns are fairly favorable in my viewpoint with the company exceeding inflation conveniently with their returns on both properties, equity and invested capital.

When compared to primary market competitors nevertheless, the Alphabet falls back. Both Apple’ s and Microsoft‘s ROAs, ROEs and ROICs for the very same duration of 22.69%, 109.15% and 40.91%, and 18.30%, 43.09% and 28.09% respectively beat Alphabet’s metrics by in between 3-9pp.

Rather just, Alphabet is less reliable at producing returns on their invested capital relative to these 2 completing business. This mostly originates from Alphabet’s higher financial investment into R&D as a portion of profits relative to its rivals primarily due to their Other Bets section.

Nonetheless, the company’s WACC is presently around 10.81% which highlights that Alphabet quickly creates greater returns on their financial investment than it costs the business to raise the capital required for stated financial investment.

Alphabet likewise has 5Y average (as determined from FY23-FY19) gross, running and net margins of 55.58%, 25.34% and 23.41% respectively. These strong margins are primarily in line with those of Apple and Microsoft and highlight simply how lucrative Alphabet’s core operations.

GOOG FY23 Q4 News Release

Alphabet provided a strong 2023 efficiency, with income and revenue development throughout its sectors, specifically in Google Cloud and Other Bets. Nevertheless, the business likewise dealt with some headwinds in its advertisement organization, in addition to restructuring and realty expenses.

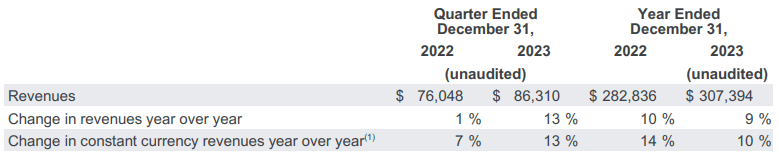

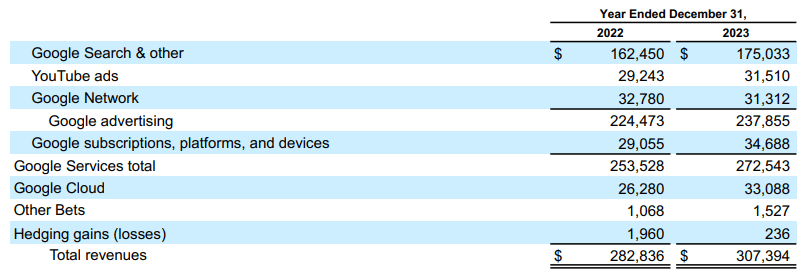

Overall income for 2023 was $307 billion, up 9% year-over-year, driven by strong development in Google Browse, YouTube, Google Cloud, and Other Bets.

GOOG FY23 Q4 10K

Google Solutions had the biggest YoY income development publishing a boost of 13% to over $272.6 B. Browse and YouTube advertisements likewise grew at a strong rate attaining simply over 10.1 % development YoY.

Within the services section Google advertisement income for 2023 was $237.9 billion, up 11% year over year, showing the healing of the online marketing market and the strength of business even in the middle of a difficult macro environment.

Google Cloud income for 2023 was $33.1 billion, up 46% year over year, showing the increased need for cloud services and services in the middle of the digital improvement pattern.

While the Browse development rate has actually slowed compared to previous years, probably as an outcome of Bing ending up being boosted with AI, Google is still certainly the search leader.

GOOG FY23 Q4 10K

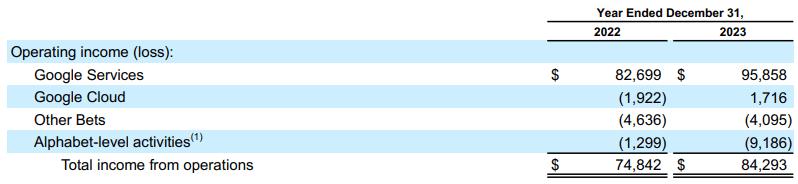

Alphabet’s operating earnings for 2023 was $95.9 billion, up 30% year-over-year, and its operating margin enhanced from 22% to 25%. This was mostly thanks to an enhancement in the income mix thanks to Google Cloud producing favorable operating earnings of $1.7 B compared to unfavorable $1.9 B at the end of FY22.

Alphabet’s earnings for 2023 was $73.8 billion, or $5.80 per diluted share up 23% YoY thanks to strong topline income development and considerable expense controls by removing a big part of unneeded labor force.

This left Alphabet dealing with around $2B in one-off charges associated with contract terminations in addition to another $1.8 B due for early lease exists on a few of their office complex.

While these expenses are regrettable, I see Alphabet’s choice to best size business headcount and workplace in the name of performance to be a great method and one which might expand margins in years to come.

Looking For Alpha|GOOG|Success

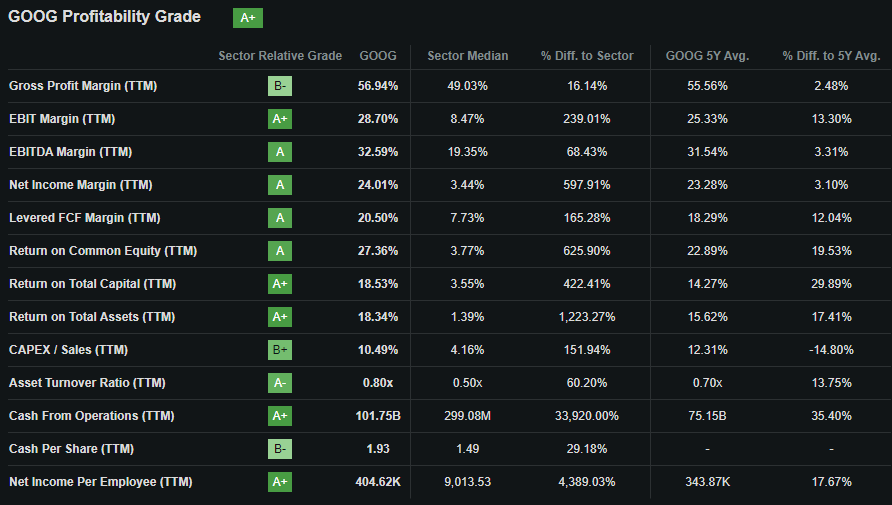

Looking for Alpha’s Quant determines an “ A+” success score for Alphabet which I think to be a precise relative assessment of the company’s existing financial circumstance provided their strong FY23 efficiency.

By evaluating Alphabet’s balance sheet, we can see the company has $171B in overall existing properties while overall existing liabilities total up to simply $81.8 B. This huge short-term liquidity leaves Alphabet with an outstanding fast ratio of 1.94 x and an outstanding existing ratio of 2.10 x.

Overall properties for Alphabet total up to $402B with overall liabilities being $119B. Alphabet likewise has $284B in overall typical equity. This leaves the company with an outstanding financial obligation equity ratio of 0.10 x.

GOOG FY23 Q4 10K

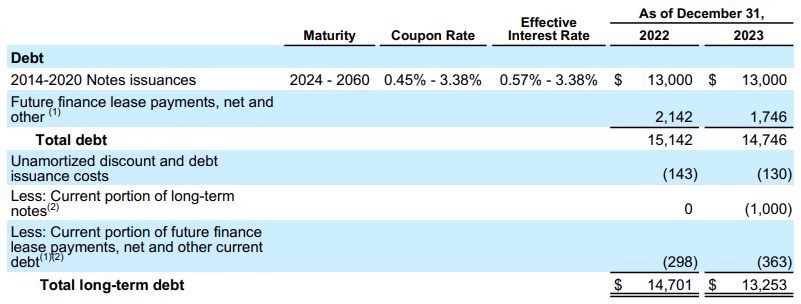

Alphabet’s long-lasting financial obligation profile is outstanding with the fixed-rate senior unsecured commitments having actually been worked out at good reliable rates of interest which permit the company’s financial resources to stay well separated from the greater rates of interest environment.

GOOG FY23 Q4 10K

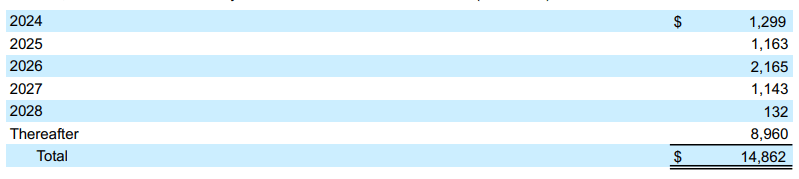

Alphabet’s financial obligation maturity profile is likewise really appealing with a bulk of debentures growing after 2028. While some maturities in between 2024-2028 are rather big, the company’s genuinely enormous unlevered FCF in FY23 of $58.9 B implies the company must deal with no difficulties funding these commitments as they emerge.

Moody’s scores firm verified an Aa2 credit score for Alphabet’s senior unsecured domestic notes while designating a P-1 score for the company’s short-term domestic business paper. The outlook stays steady. Moody’s categorizes “Aa2” credit scores as being of “high financial investment grade” while “P-1” is specified as being of the greatest “Prime” quality.

Appraisal

Looking For Alpha|GOOG|Appraisal

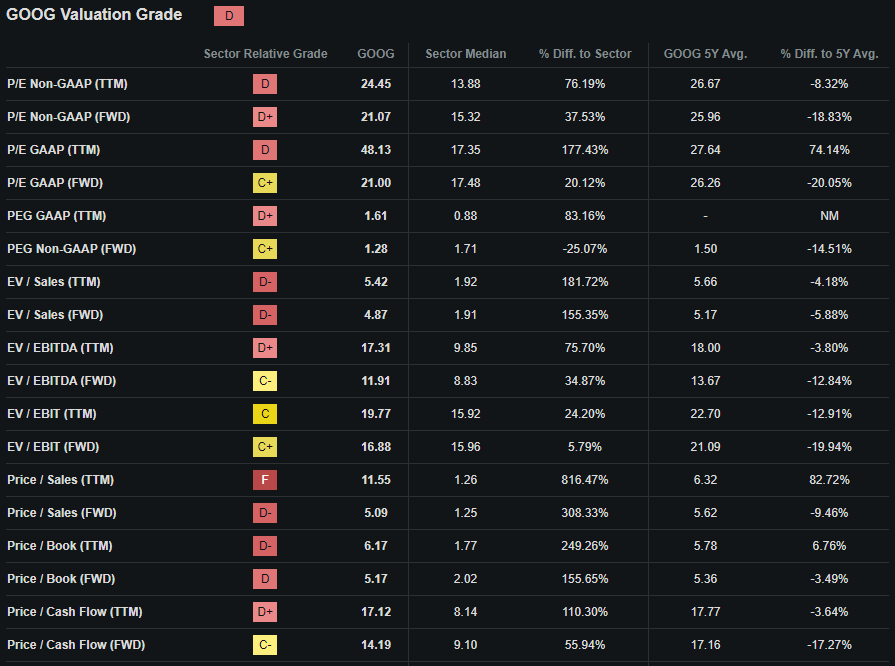

Looking for Alpha’s Quant appoints Alphabet with a “ D” Appraisal grade. I think this letter grade might be an exceedingly cynical representation of the worth present within the stock provided their strong development potential customers.

The company presently trades at a P/E GAAP FWD ratio of 21.00 x. This represents an enormous 20% decline in the company’s GAAP P/E ratio compared to their running 5Y average and is considerably lower than that of Apple or Microsoft.

Alphabet’s P/CF TTM of 17.12 x is sensible while their Price/Sales FWD of 5.09 x is more in line with what I would anticipate provided the somewhat softer outlook for their development potential customers as Google has actually fallen somewhat behind Microsoft in the AI race.

Looking For Alpha|GOOG|5Y Advanced Chart

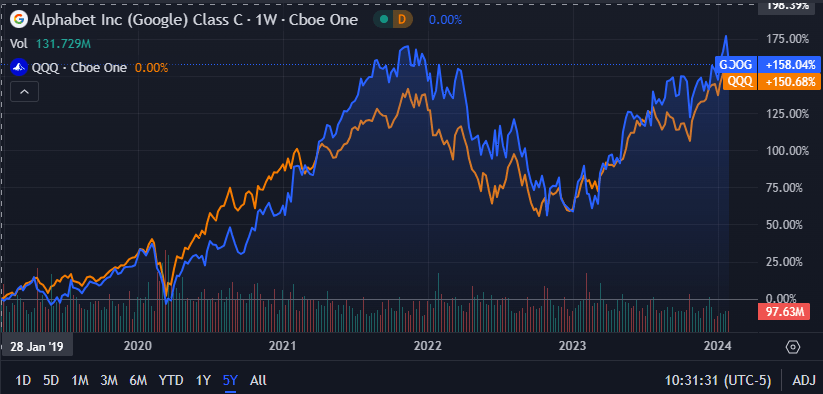

From an outright viewpoint, Alphabet shares are trading near all-time highs with existing share rates of around $143 only simply falling shy of the peak attained a couple of days prior to the writing of this post.

Nonetheless, Alphabet shares have actually basically matched the 5Y efficiency of the Nasdaq 100-Index ( NDX)- tracking Invesco QQQ Trust ETF ( QQQ), which highlights simply how well the company has actually rewarded investors with its stock cost gratitude.

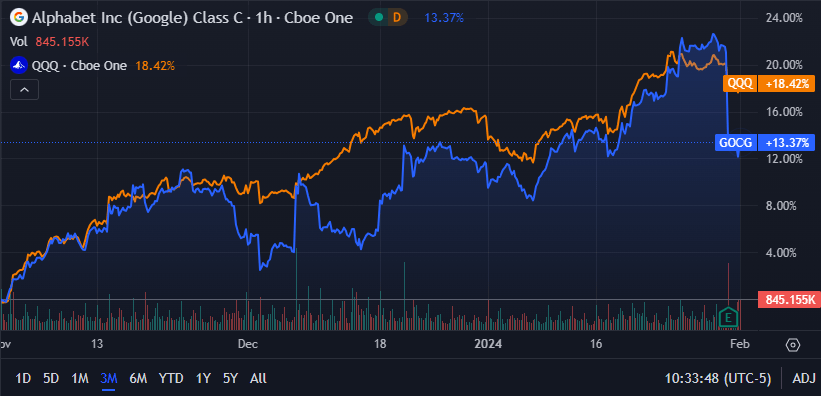

Looking For Alpha|GOOG|3M Advanced Chart

Over the last 3 months, Alphabet stock has actually carried out extremely well rallying up over 22% till the over night correction after the company reported incomes.

I think the abrupt drop in share rates came as an outcome of markets remedying an over-bought condition and due to the more hawkish than anticipated tone originating from Jerome Powell at the current FED conference.

The Worth Corner

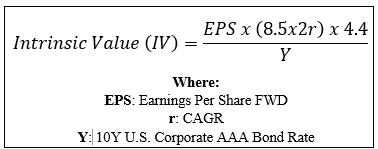

By using our specifically developed Intrinsic Appraisal Estimation, we can comprehend what worth exists in the business from a more unbiased viewpoint.

Utilizing the company’s existing share cost of $143, an approximated 2024 EPS of $6.73, a sensible “r” worth of 0.12 (12%) and the existing Moody’s Seasoned AAA Corporate Bond Yield ratio of 4.74 x, I obtain a base-case IV of $203. This represents a considerable 30% undervaluation in shares.

Even when utilizing a more cynical CAGR worth for r of 0.07 (7%) to show a circumstance where an internationally covering economic crisis triggers Alphabet to enormously miss out on income development price quotes, shares are valued at around $140.60 recommending a reasonable assessment in shares.

Thinking about the assessment metrics, outright assessment and intrinsic worth estimation, I think that Alphabet is presently trading someplace in between a reasonable assessment and a 30% undervaluation in shares.

In the short-term (3-12 months), practically anything might occur to share rates as markets tend to act more like voting makers instead of weighing scales over short-time durations. Nonetheless, I do see the hawkish tone originating from the FED in addition to the over-bought nature of lots of tech stocks possibly positioning down pressure on Alphabet stock for a minimum of 2-4 months.

In the long-lasting (2-10 years), I think Alphabet will continue to see their Google companies establish at fast rate to catch-up to the AI running start Microsoft has actually attained with ChatGPT, Bing and Copilot.

In spite of the intense competitors presently occurring throughout the Cloud and AI companies, I do think Google has all the best resources to complete and win versus their competitors.

Alphabet Danger Profile

Alphabet deals with some intense dangers occurring especially from high levels of competitors throughout their organization sectors in addition to some intense ESG issues.

Alphabet’s Google items all deal with considerable competitors from the similarity Apple and Microsoft. Both competitors have their own product and services communities that are pitted straight versus Google’s own offerings.

Current successes by Microsoft’s Azure and Bing, Amazon’s AWS and even Apple’s supremacy in the smart device market highlights simply just how much competitors Google is confronting with their core Cloud and Solutions items.

Moreover, while the Browse organization appeared bulletproof for a very long time, Microsoft’s dive forwards with Bing appeared to have actually captured Google sleeping. While I do think the company can revitalize and reinforce this crucial organization, Alphabet should guarantee its companies stay at the leading edge of the development race.

Reports Apple might be dealing with their own Online search engine locations more pressure on Google’s crucial income stream as the loss of native promo of Apple gadgets would considerably harm Alphabet’s bottom line.

From an ESG viewpoint, Alphabet likewise deals with genuine dangers from governance problems surrounding their organization endeavors.

To start with, Alphabet has a really incomprehensible quantity of delicate user information on their consumers which should stay definitely personal. Any information breach might have huge reputational and financial effects for the company.

Alphabet’s huge size has actually likewise put the company in hot waters with different antitrust cases and lawsuits being brought versus the company for supposed unreasonable organization practices.

The company likewise deals with a genuine governance danger from any future mergers or acquisitions as any more sideways growth into brand-new companies might be considered as exceedingly monopolistic.

While these ESG issues are genuine, I still think Alphabet’s proactive technique to environment preservation and promise for office equality suffices to make the company a terrific ESG mindful choice.

Obviously, viewpoints might differ with concerns to ESG product and I urge you to perform your own ESG and sustainability research study before buying the business if these matters are of issue to you.

Summary

Alphabet has actually had a difficult number of years leading up to 2023. Thankfully for the company, numerous executional wins and a viewed enhancement in the company’s own AI capacity has actually manifested itself with a strong incomes efficiency in 2023.

Nonetheless, the company is still dealing with a few of the biggest competitive obstacles and a difficult macroeconomic environment heading into 2024 with a prospective souring in financier beliefs taking place after the complete year 2023 outcomes.

Appraisals have not yet appeared to cost in 2024 development with shares relatively underestimated by 30% presuming aced execution throughout the year. Obviously, my bear-case situation sees shares relatively valued must Alphabet development fall around 30% except expectations.

For that reason, I rank Alphabet, Inc. stock a Buy at present time and think the post-earnings depression has actually produced simply enough margin of security for a GARP oriented financiers to start developing a position.