Alfribeiro/iStock Editorial by way of Getty Pictures

Symbol: Coca-Cola FEMSA Brazil supply truck

Coca-Cola Funding Thesis – Striking IRS Declare To One Aspect

I prior to now printed a piece of writing on The Coca-Cola Corporate (NYSE:KO), “Coca-Cola: Debt Ranges Lowered, Horny More than one, Improve From Grasp To Purchase” on Oct. 9, 2023, forward of Q3-2023 profits liberate on Oct. 24, 2023. Therefore, Coca-Cola persevered its longer term of profits beats with a beat of $0.05 for Q3-2023. SA Top class analysts’ consensus EPS estimates for 2023 have additionally greater by means of $0.05 from $2.64 to $2.69. On the other hand, SA Top class analysts’ consensus EPS estimates for 2024 have remained unchanged at $2.81, a modest build up of four.5% over 2023 estimated EPS. Analysts’ consensus EPS estimates for 2025 and 2026 display little trade from ultimate October. My trade from Grasp to Purchase ranking again in October 2023 has been justified by means of an build up of 13.35% within the percentage worth from $52.88 on the time of my earlier article to $59.94 at shut on Feb. 6, 2024. On the other hand, the upper percentage worth leads to the dividend yield lowering from 3.35% to a few.06%. And on the upper percentage worth, without a trade in EPS estimate for 2024, the ahead P/E ratio for 2024 has greater from 19.81 ultimate October to 22.62 these days. The present 22.62 continues to be under my changed long-term reasonable P/E ratio calculation of 23.70 for Coca-Cola, and on that foundation I can take care of a Purchase ranking. However I don’t be expecting the proportion worth to develop on the identical top price it has completed since my October 2023 article. A extra detailed Monetary Research and Remark phase in toughen of those conclusions seems additional under.

Caveat Re IRS Billions Tax Cost Declare

The foregoing assumes Coca-Cola control is right kind in believing they’ll win their enchantment towards an IRS declare for probably billions in retrospective tax bills associated with the Coca-Cola FEMSA Brazilian operations. Luck by means of the IRS would additionally imply a better annual tax burden affecting profits going ahead. From operating with engineers right through my mining trade days, I am conversant in the ideas of chance and outcome. From an engineering standpoint, a chance that is very low however has doable very impactful penalties, is noticed as a better chance than some other chance that is top however has minor penalties. So design of a concrete slab for a suspension bridge can be thought to be way more essential relating to avoidance of chance of failure than chance of a slab on floor creating a crack. The danger and outcome of the IRS declare seem to be extra within the suspension bridge class.

The IRS declare, and penalties if now not overturned on enchantment, are mentioned intimately under.

Coca-Cola Litigation – IRS Declare For Billions In Again tax

Coca-Cola’s Place at the Billions IRS Declare

This can be a long-standing subject as in step with quite a lot of decided on excerpts under from Coca-Cola’s SEC filings appearing the ancient timeline:

- From 2015 10-Ok – On September 17, 2015, the Corporate won a Statutory Realize of Deficiency (“Realize”) from the IRS for the tax years 2007 thru 2009, after a five-year audit. Within the Realize, the IRS claims that the Corporate’s United States taxable source of revenue will have to be greater by means of an quantity that creates a doable further federal source of revenue tax legal responsibility of roughly $3.3 billion for the duration, plus passion… The Corporate firmly believes that the IRS’ claims are with out benefit and plans to pursue all to be had administrative and judicial treatments important to get to the bottom of this subject.

- From 2016 10-Ok – As a result, if this dispute had been to be in the end made up our minds adversely to us, the extra tax, passion and any doable consequences may have a subject material adversarial affect at the Corporate’s monetary place, result of operations and money flows.

- From 2017 10-Ok – A trial date has been set for March 5, 2018.

- From 2020 10-Ok – On November 18, 2020, the U.S. Tax Courtroom (“Tax Courtroom”) issued an opinion (“Opinion”) predominantly siding with the IRS. Even supposing the Corporate disagrees with the destructive parts of the Opinion and intends to vigorously shield its place, making an allowance for all avenues of enchantment, there’s no assurance that the courts will in the end rule within the Corporate’s want.

- From 2022 10-Ok – We concluded, in keeping with the technical and felony deserves of the Corporate’s tax positions, that it’s much more likely than now not the Corporate’s tax positions will in the end be sustained on enchantment.

- From Coca-Cola’s September 29, 2023, Q3-2023 10-Q submitting – We’re these days in litigation with the IRS for tax years 2007 thru 2009. On November 18, 2020, the Tax Courtroom issued the opinion wherein it predominantly sided with the IRS; alternatively, a call continues to be pending and the timing of such resolution isn’t these days identified. The Corporate strongly disagrees with the IRS’ positions and the parts of the Opinion declaring such positions and intends to vigorously shield our positions using each to be had road of enchantment. Whilst the Corporate believes that it’s much more likely than now not that we can in the end succeed on this litigation upon enchantment, it’s conceivable that every one, or some portion of, the changes proposed by means of the IRS and sustained by means of the Tax Courtroom may in the end be upheld. Within the tournament that all the changes proposed by means of the IRS had been to be in the end upheld for tax years 2007 thru 2009 and the IRS, with the consent of the federal courts, had been to come to a decision to use the underlying method (“Tax Courtroom Method”) to the following years as much as and together with 2022, the Corporate these days estimates that the possible combination incremental tax and passion legal responsibility may well be roughly $14 billion as of December 31, 2022. Further source of revenue tax and passion would proceed to accrue till the time this kind of doable legal responsibility, or portion thereof, had been to be paid. The Corporate estimates the affect of the continuing utility of the Tax Courtroom Method for the 9 months ended September 29, 2023 would build up the possible combination incremental tax and passion legal responsibility by means of roughly $1.2 billion….The Corporate does now not know when the Tax Courtroom will factor its opinion in regards to the impact of Brazilian felony restrictions at the cost of royalties by means of the Corporate’s licensee in Brazil for the 2007 thru 2009 tax years. After the Tax Courtroom problems its opinion at the Corporate’s Brazilian licensee, the Corporate and the IRS will likely be supplied time to agree at the tax affect of each critiques, and then the Tax Courtroom would render a call within the case. The Corporate can have 90 days thereafter to report a realize of enchantment to the U.S. Courtroom of Appeals for the 11th Circuit and pay the tax legal responsibility and passion associated with the 2007 thru 2009 tax years. The Corporate these days estimates that the cost to be made at the moment associated with the 2007 thru 2009 tax years, which is incorporated within the above estimate of the possible combination incremental tax and passion legal responsibility, can be roughly $5.6 billion (together with passion accumulated thru September 29, 2023), plus any further passion accumulated in the course of the time of cost. Some or all of this quantity can be refunded if the Corporate had been to succeed on enchantment….Whilst we imagine it’s much more likely than now not that we can succeed within the tax litigation mentioned above, we’re assured that, between our skill to generate money flows from running actions and our skill to borrow price range at affordable rates of interest, we will be able to set up the variety of conceivable results within the ultimate answer of the subject.

Tax Courtroom’s Upholds Coca-Cola Switch Pricing Adjustment – November 8, 2023

On November 8, 2023, the Tax Courtroom discovered towards Coca-Cola in its resolution with regards to The Coca-Cola Corporate and Subsidiaries, Petitioner v. Commissioner of Inside Income, Respondent, as follows –

In sum, petitioner has failed to meet its burden of evidence in two main respects. It has introduced no proof that will permit us to resolve what portion of the transfer-pricing adjustment is resulting from exploitation of the non-trademark IP, which we’ve got discovered be essentially the most precious phase of the intangibles from the Brazilian provide level’s financial viewpoint. And petitioner has introduced inadequate proof to permit us to resolve what portion of the transfer-pricing adjustment is resulting from exploitation of the 8 authentic core-product logos, versus the 60 different core-product logos and all of the universe of non-core-product logos. As a result of petitioner has failed to ascertain what portion of the combination transfer-pricing adjustment could be resulting from exploitation of the 8 grandfathered logos, we don’t have any choice however to maintain that adjustment in complete.

To put in force the foregoing, Resolution will likely be entered below Rule 155.

Coca-Cola’s Reaction To November 8, 2023 Tax Courtroom Ruling

Excerpted from November 9, 2023 Coca-Cola press liberate on Tax Courtroom ruling.

Whilst we disagree with the court docket’s interpretation of the information and legislation on this case, we’re happy to transport nearer to a last answer of the Tax Courtroom case in order that we will be able to pursue an enchantment, the place we will be able to assert our claims and vigorously shield the corporate’s place…. We don’t be expecting the leads to this fresh supplemental resolution to switch the methodologies we’ve got used to calculate the tax reserve we’ve got taken or the possible combination incremental tax and passion legal responsibility we’ve got disclosed associated with the dispute with the IRS or our efficient tax price.

Forbes Article Suggests Coca-Cola Not going To Win In opposition to IRS Declare For Billions

In line with excerpts under from a November 27, 2023 article, “IRS Does not Want The Blocked Source of revenue Tax Laws In Coca-Cola“, Forbes Contributor, Ryan Finley, steered Coca-Cola’s possibilities of eventual good fortune are dim.

The Tax Courtroom’s new opinion deciding the blocked source of revenue query raised in Coca-Cola v. Commissioner, T.C. Memo. 2023-135, means that Coca-Cola’s possibilities of eventual good fortune are dim, whether or not the blocked source of revenue rules are upheld on enchantment or now not. …The supplemental opinion, which additionally facets with the IRS, might be the ultimate step within the Coca-Cola case prior to it heads to an inevitable enchantment.

Coca-Cola Enchantment of Tax Courtroom Rulings

From the corporate filings and press liberate detailed above –

- Coca-Cola will wish to interact with the IRS to agree at the quantity of tax that will be payable if the Tax Courtroom’s resolution had been carried out. It’s presumed that is already in educate and extra data will most likely develop into to be had within the upcoming This fall-2023 profits liberate scheduled for pre-market Feb., 13, 2024 and the 10-Ok typically launched round every week later.

- After settlement with the IRS at the quantum of the cost, Coca-Cola can have 90 days to report a realize of enchantment. Assuming the cost quantity has already been agreed then the enchantment would wish to be lodged in all probability in Might 2024.

- As a way to enchantment, Coca-Cola must originally pay the portion of the possible combination incremental tax and passion legal responsibility associated with the 2007 thru 2009 tax years. Coca-Cola estimates this quantity to be in way over $5.6 billion.

- Coca-Cola has said it stays assured of successful this example on enchantment and does now not intend to switch its methodologies for calculating its tax reserve. Accordingly, 2023 complete yr effects are not likely to be impacted by means of the 8 November 2023 Tax Courtroom resolution.

Coca-Cola is because of liberate its complete yr 2023 effects pre-market on Feb. 13, 2024, and an replace at the IRS declare can also be anticipated. A extra complete replace can also be anticipated with the 10-Ok annual document prone to be launched round Feb. 20, 2024, in keeping with previous timing. Any enchantment and provisional tax cost can be disclosed as a post-balance date tournament.

Have an effect on on Coca-Cola the Corporate of Lack of Enchantment In opposition to IRS Tax Cost Declare

The corporate has expressed self assurance in an final win towards the IRS declare. On the identical time, the corporate has not at all dominated out the potential of the IRS maintaining its declare, leading to billions in more tax bills. As a way to enchantment the case the corporate will have to finally first pay $5.6 billion prematurely. That seems to be prone to happen within the first part of 2024. The corporate seems effectively located to tackle some other $5.6 billion in debt or to satisfy this cost out of its huge money and investments steadiness. Since December 2020 internet debt as a share of internet debt plus fairness has lowered from 62.3% to 50.1% at finish September 2023. The $5.6 billion cost, if additionally booked as an expense, may well be anticipated to extend internet debt as a share of internet debt plus fairness to ~61%, nonetheless under 2020 stage of 62.3%. If the $14 billion cost had been made within the close to time period and booked as a price, internet debt as a share of internet debt plus fairness may well be anticipated to extend to ~77%. On the other hand, a court docket ruling on any enchantment is prone to take ~3 years and during the last 3 years Coca-Cola has decreased internet debt by means of ~$5.5 billion and greater shareholders’ fairness by means of ~$7 billion. Assuming an identical development over the following 3 years and the tax cost declare expanding to $17 billion in 3 years’ time, internet debt as a share of internet debt plus fairness may well be anticipated to extend to ~70% on the time of cost of the $17 billion. There would even be an affect on long run every year profits and EPS because of the continued upper tax bills. Lowered liquidity may lead to a discount in percentage repurchases with an adversarial affect on EPS due upper percentage depend. Decrease EPS, decreased liquidity and better percentage depend may prohibit dividend expansion.

Conclusion:

I imagine the view of the corporate expressed within the excerpts above is affordable, viz.,

…we’re assured that, between our skill to generate money flows from running actions and our skill to borrow price range at affordable rates of interest, we will be able to set up the variety of conceivable results within the ultimate answer of the subject.

Have an effect on on Coca-Cola Shareholders of Lack of Enchantment In opposition to IRS Tax Cost Declare

Whilst, it is believed the worst-case result for the corporate does now not provide whatsoever an existential risk, the affect for shareholders may manifest in quite a few tactics. The rapid affect would most likely be a vital dip within the percentage worth. The secondary affects may well be in decreased long run EPS expansion and a limitation on dividend expansion, or perhaps a aid in dividends. Those in flip may adversely affect long run percentage worth expansion.

Conclusion:

Any enchantment may most likely take ~3 years or extra prior to a verdict is passed down. Given this subject, and the related doable dangers and penalties, had been disclosed way back to 2015 with common updates within the intervening duration, it can be the danger is already mirrored within the percentage worth. On the other hand, because the case progresses, better consciousness would possibly start to put downward drive at the percentage worth. The lack of the enchantment by means of Coca-Cola in November 2023 does now not seem to have been broadly reported. It’s going to be fascinating to look if there’s any affect at the percentage worth when Coca-Cola supplies an replace at the IRS declare and Tax Courtroom ruling and any enchantment within the 4th quarter profits liberate and the 2023 annual document.

Monetary Research and Remark

On the lookout for marketplace mispricing of shares

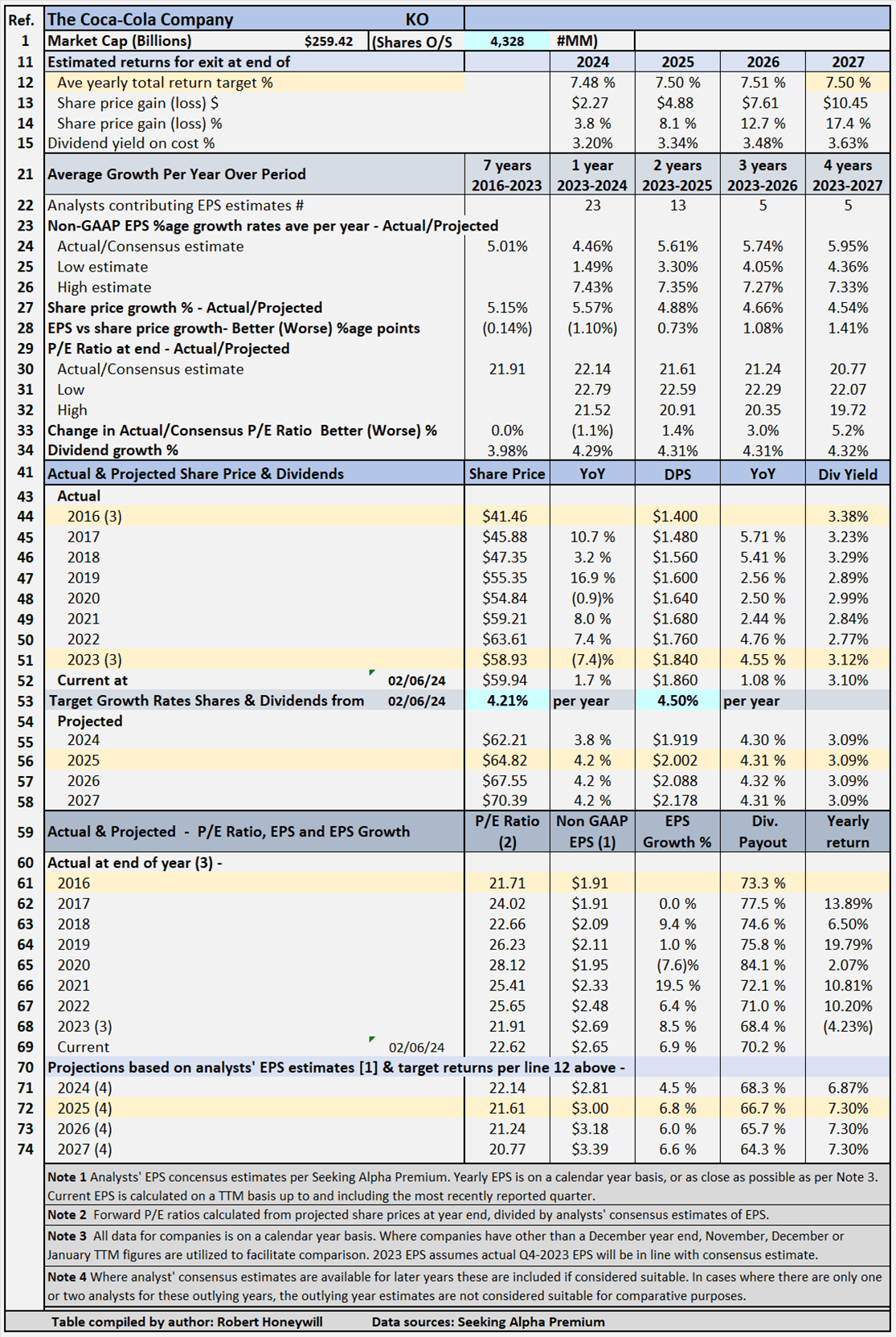

What I am basically searching for listed below are circumstances of marketplace mispricing of shares because of distortions to lots of the same old statistics used for screening shares for purchase/grasp/promote choices. I imagine the solution is to check projections, in keeping with analysts’ estimates out to the tip of 2025 or later, to previous efficiency. Summarized in Tables 1 and a pair of under are the result of compiling and examining the information in this foundation.

Desk 1 – Detailed Monetary Historical past And Projections

Looking for Alpha Top class

Desk 1 paperwork ancient knowledge from 2016 to 2023, together with percentage costs, P/E ratios, EPS and DPS, and EPS and DPS expansion charges. The desk additionally contains estimates out to 2027 for percentage costs, P/E ratios, EPS and DPS, and EPS and DPS expansion charges. (Word – whilst estimates are proven for analysts’ EPS estimates out to 2024 to 2027 the place to be had, estimates do generally tend to develop into much less dependable, the additional out the estimates pass. Those estimates are simplest thought to be sufficiently dependable if there are a minimum of 3 analysts’ contributing estimates for the yr in query). Desk 1 permits modeling for goal overall charges of go back. Within the case proven above, the objective set for overall price of go back is 7.5% in step with yr in the course of the finish of 2027 (see line 12), in keeping with purchasing on the Feb. 6, 2024, ultimate percentage worth stage. As famous above, estimates develop into much less dependable within the later years. I’ve determined to enter a goal go back in keeping with the 2027 yr, which has EPS estimates from 5 analysts, as it permits for the affect of the projected EPS expansion charges to be taken into consideration within the evaluation of the worth of Coca-Cola stocks. The desk presentations to succeed in the 7.5% go back, the desired reasonable every year percentage worth expansion price from Feb. 6, 2024 thru Dec. 31, 2027, is 4.21% (line 53). Dividends and dividend expansion account for the steadiness of the objective 7.5% overall go back. The 4.21% compares to precise percentage worth expansion during the last 7 years of five.15% (see line 23). This 5.15% percentage worth expansion compares intently to EPS expansion of five.01% over the similar duration.

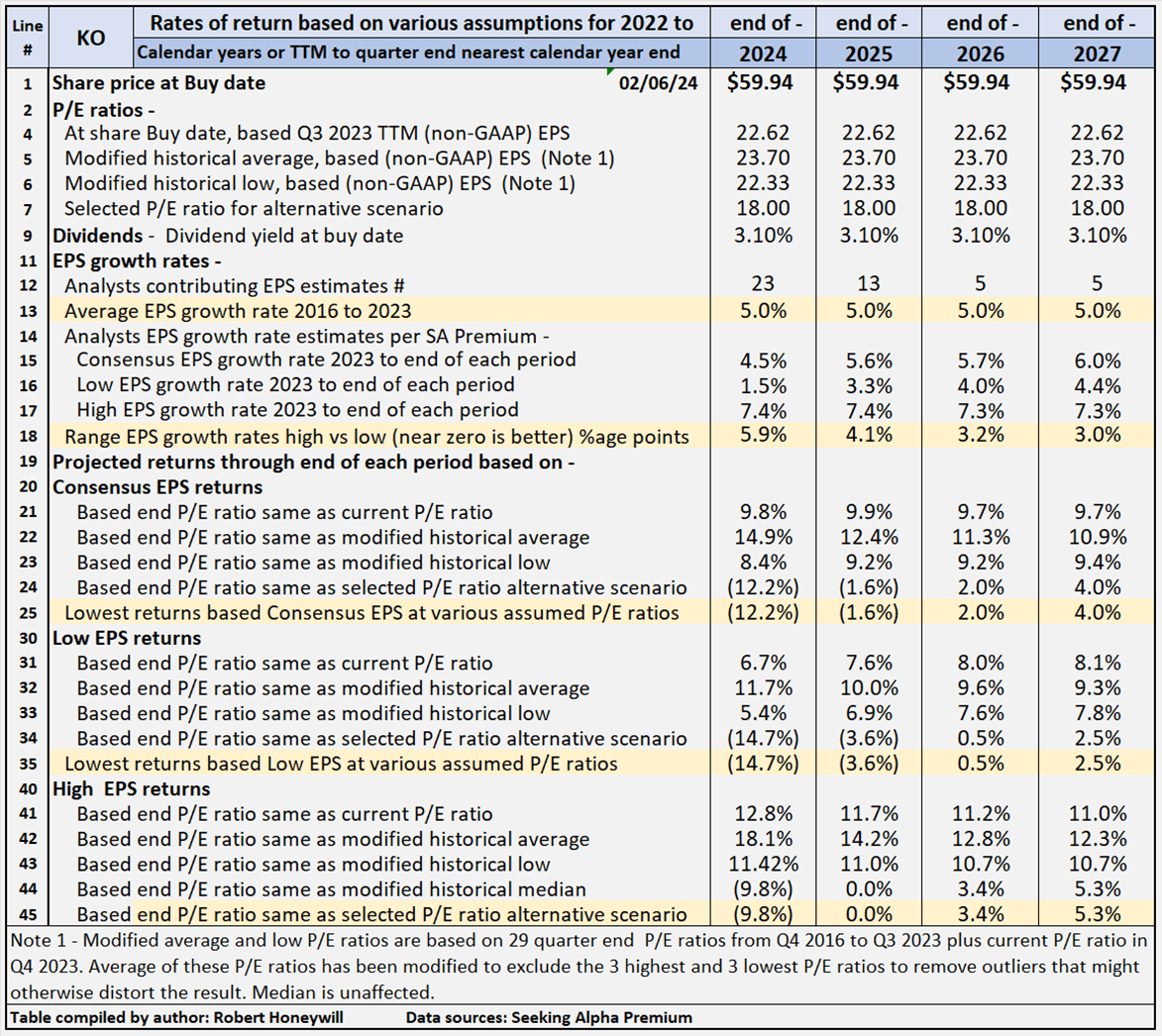

Coca-Cola’s Projected Returns Primarily based On Decided on Historic P/E Ratios Thru Finish Of 2027

Desk 2 under supplies further situations projecting doable returns in keeping with make a choice ancient P/E ratios and analysts’ consensus, low, and top EPS estimates in step with Looking for Alpha Top class thru finish of 2027.

Desk 2 – Abstract of related projections Coca-Cola

Looking for Alpha Top class

Desk 2 supplies comparative knowledge for getting at ultimate percentage worth on Feb. 6, 2024, and keeping in the course of the finish of years 2024 thru 2027. There is a overall of twelve valuation situations for every yr, made from 3 EPS estimates (SA Top class analysts’ consensus, high and low) throughout 3 other P/E ratio estimates, in keeping with ancient knowledge, plus a fourth P/E ratio decided on to supply an alternate situation. Coca-Cola’s P/E ratio is at the moment 22.62, which is under the ancient reasonable P/E ratio of 23.70. Desk 2 presentations doable returns from an funding in stocks of the corporate around the vary of P/E ratios This research, from hereon, assumes an investor purchasing Coca-Cola stocks nowadays can be ready to carry thru 2027, if important, to succeed in their go back targets. Feedback on contents of Desk 2, for the duration to 2027 column observe.

Consensus, high and low EPS estimates

All EPS estimates are in keeping with analysts’ consensus, high and low estimates in step with SA Top class. That is designed to supply a variety of valuation estimates starting from low to in all probability, to top in keeping with analysts’ tests. I may generate my very own estimates, however those would most likely fall inside the similar vary and would now not upload to the worth of the workout. That is specifically so in appreciate of well-established companies akin to Coca-Cola. I imagine the “low” estimates will have to be thought to be essential. It is prudent to regulate chance by means of figuring out the possible worst-case situations from no matter motive.

Choice P/E ratios used in situations

- The real P/E ratios on the percentage purchase date are in keeping with precise non-GAAP EPS for This fall-2023 TTM (observe for comfort the style assumes precise EPS for This fall-2023 will likely be in keeping with analysts’ consensus EPS estimates).

- A changed reasonable P/E ratio in keeping with 30 quarter-end P/E ratios from This fall 2016 to This fall 2023 and present P/E ratio in Q1 2024. The common of those P/E ratios has been changed to exclude the 3 perfect and 3 lowest to take away outliers that would possibly in a different way distort the end result.

- A changed low P/E ratio used to be calculated the use of the similar knowledge set used for calculating the changed reasonable P/E ratio, and calculated on a an identical foundation, with the 3 perfect and lowest P/E ratios excluded.

- A mean P/E ratio is calculated the use of the similar knowledge set used for calculating the changed reasonable P/E ratio. In fact, the median is identical whether or not or now not the 3 perfect and lowest P/E ratios are excluded. In terms of Coca-Cola, I’ve selected to make use of an assumed P/E ratio of 18.0 instead of the ancient median of 23.81 (very similar to the common). I’ve completed this to supply an concept of the affect on returns of the a couple of declining considerably under the existing stage and the ancient reasonable. The chosen P/E a couple of of 18.0 compares to the sphere median of 17.94 for PE Non-GAAP [FWD], in step with Looking for Alpha Top class metrics.

Reliability of EPS estimates (line 18)

Line 18 presentations the variety between low and high EPS estimates. The broader the variety, the better confrontation there’s between essentially the most positive and essentially the most pessimistic analysts, which has a tendency to signify better uncertainty within the estimates. There are 5 analysts masking Coca-Cola thru finish of 2027. In my revel in, a variety of three.0 share issues distinction in EPS expansion estimates amongst analysts is fairly low, and suggests some extent of walk in the park, and thus greater reliability.

Projected Returns (traces 19 to 45)

Traces 25, 35 and 45 display at Coca-Cola’s ancient reasonable P/E a couple of of 23.70, the indicative returns vary from 9.3% to twelve.3%, with consensus 10.9%. If Coca-Cola’s provide a couple of of twenty-two.62 continues thru 2027, returns starting from 8.1% to 11.0% are indicated, with consensus 9.7%.

At a decided on decrease P/E a couple of of 18.0, kind of in keeping with the sphere reasonable, Coca-Cola is conservatively indicated to go back between 2.5% and 5.3% reasonable in step with yr in the course of the finish of 2027. The two.5% go back is in keeping with analysts’ low EPS estimates and the 5.3% on their top EPS estimates, with a 4.0% go back in keeping with consensus estimates. The two.5% go back on the analysts’ low EPS estimate for 2027 and at a discounted P/E ratio of 18.0 presentations that certain returns are nonetheless conceivable even though EPS and a couple of fall in need of present expectancies, supplied the stocks are held for quite a few years. Against this, purchasing the stocks now and keeping simplest till finish of 2024 provides an indicative destructive (14.7)% go back below the low EPS and coffee P/E ratio situation.

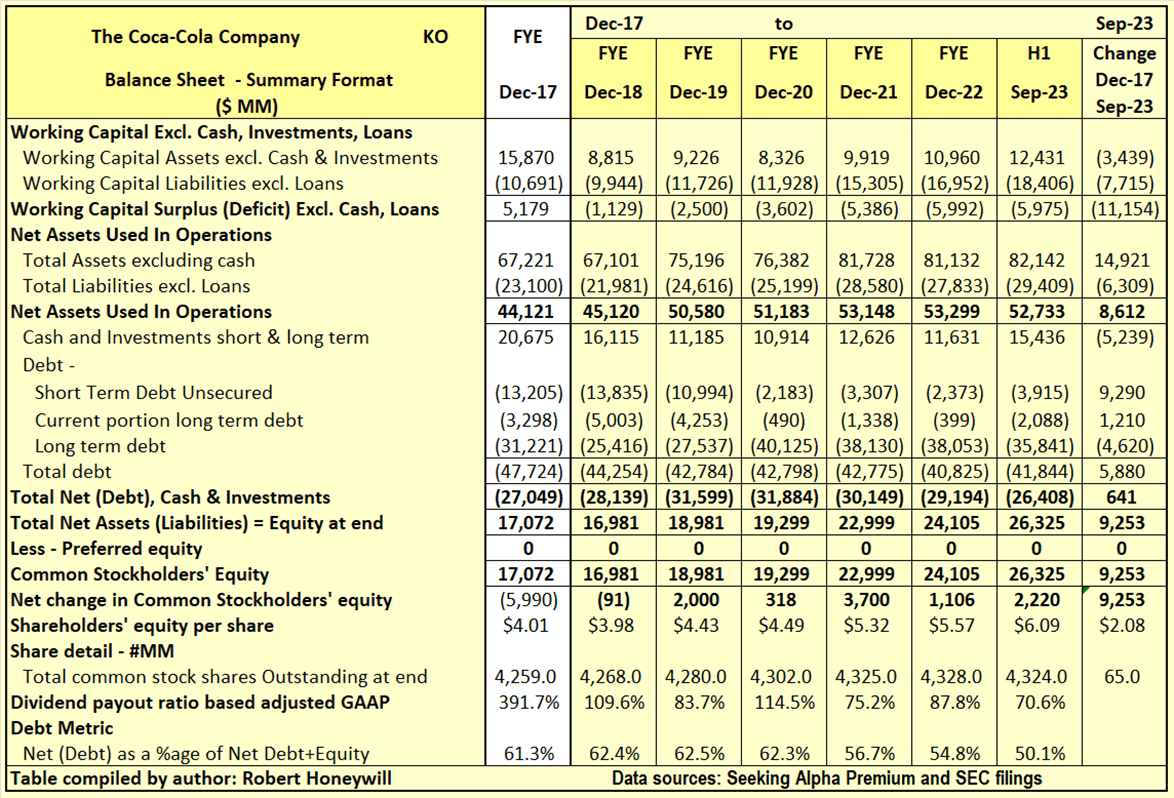

Checking Coca-Cola’s “Fairness Bucket”

Desk 3.1 Coca-Cola Steadiness Sheet – Abstract Layout

Looking for Alpha Top class and SEC filings

Over the 5.75 years finish of 2017 to finish of Q3-2023, Coca-Cola greater internet property utilized in operations by means of $8,612 million. This $8,612 million build up used to be funded by means of a $641 million build up in debt internet of money, and a $9,253 million build up in shareholders’ fairness. Internet debt as a share of internet debt plus fairness has lowered from 61.3% at finish of 2017 to 50.1% at finish of Q3-2023. It is noteworthy the advance in debt to fairness is basically because of retention of income for funding in expansion of the corporate, and percentage problems to workers, thus expanding shareholders’ fairness. Exceptional stocks greater by means of 65.0 million from 4,259 million to 4,324 million, over the duration, because of stocks issued for inventory reimbursement, partially offset by means of percentage repurchases. The $9,253 million build up in shareholders’ fairness during the last 5.75 years is analyzed in Desk 3.2 under.

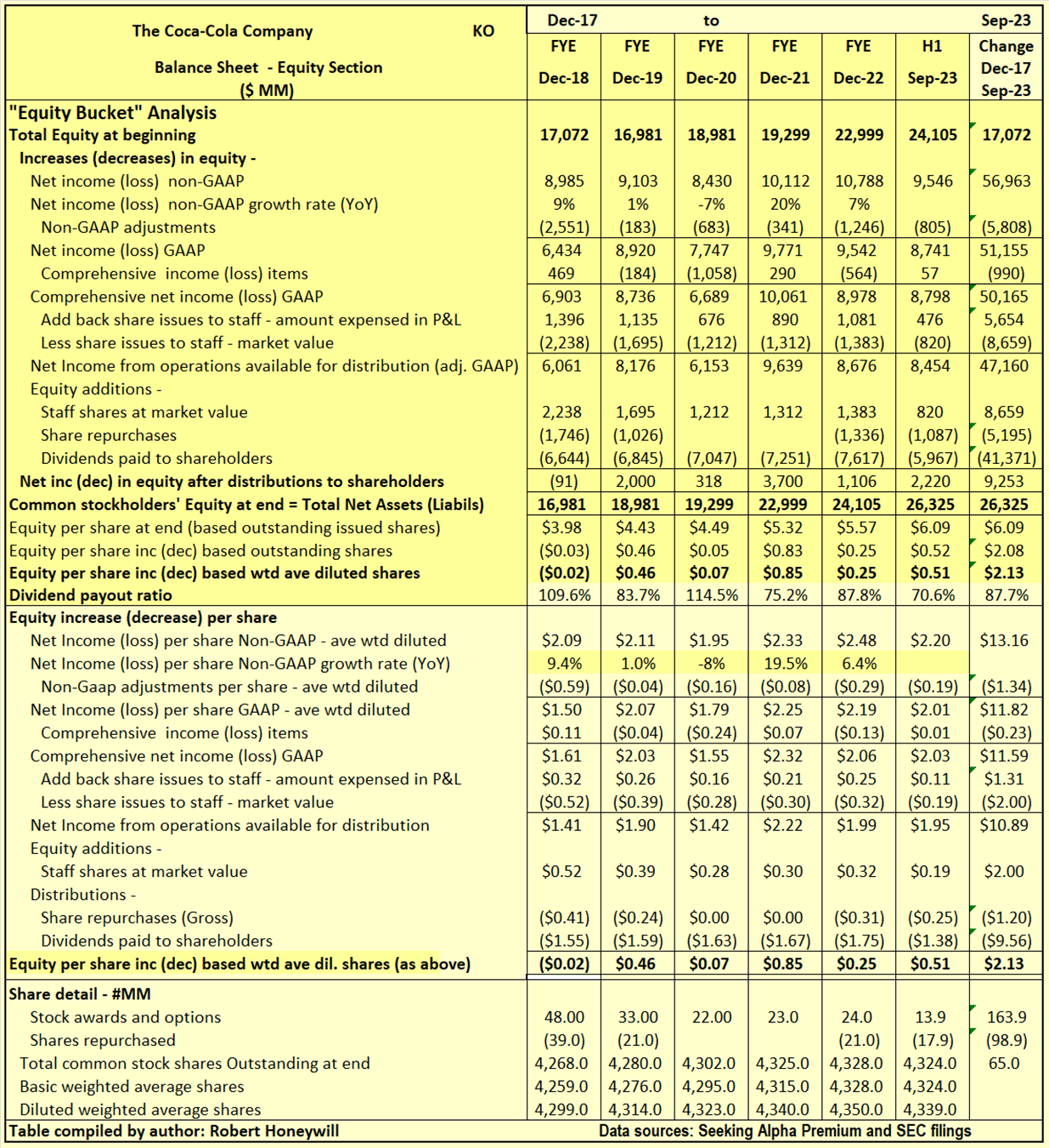

Desk 3.2 Coca-Cola Steadiness Sheet – Fairness Segment

Looking for Alpha Top class and SEC filings

I frequently in finding corporations document profits that are meant to go with the flow into and build up shareholders’ fairness. However frequently the rise in shareholders’ fairness does now not materialize. Additionally, there can also be distributions out of fairness that don’t get advantages shareholders. Therefore, the time period “leaky fairness bucket.” I search for proof of this in my research of adjustments in shareholders’ fairness. Coca-Cola’s “leaky fairness bucket” problems relate most commonly to non-GAAP changes and stocks issued for team of workers stock-based reimbursement.

Explanatory feedback on Desk 3.2 for the duration finish FY-2017 to finish Q3-2023.

- Reported internet source of revenue (non-GAAP) over the 5.75-year duration totals to $56,963 million, an identical to diluted internet source of revenue in step with percentage of $13.16.

- Over the 5.75-year duration, the non-GAAP internet source of revenue excludes a vital $5,808 million (EPS impact $1.34) of things thought to be ordinary or of a non-recurring nature so as to higher display the underlying profitability of Coca-Cola. It at all times is of outrage when corporations exclude prices yr after yr at the foundation they’re brief or ordinary.

- Different complete source of revenue contains things like foreign currency translation changes in appreciate to constructions, plant, and different amenities positioned in a foreign country and adjustments in valuation of property within the pension fund – those don’t seem to be handed thru internet source of revenue as they vary with out affecting operations and will simply opposite in a following duration. However, they do affect at the price of shareholders’ fairness at any cut-off date. For Coca-Cola, these things had been a internet lack of $990 million, EPS impact destructive $(0.23), over the 5.75-year duration.

- Quantity taken up in fairness to account for stocks issued to team of workers over the 5.75 years is $5,654 million. This compares to an estimated marketplace price of $8,659 million on the time of factor for those stocks. The true value of those stocks is larger by means of $3,005 million (EPS impact $0.69) than allowed for in arriving at non-GAAP EPS, a subject material distinction.

- By the point we take the aforementioned pieces into consideration, we discover, over the 5.75-year duration, the reported non-GAAP EPS of $13.16 ($56,963 million) has lowered to $10.89 ($47,160 million), added to price range from operations to be had for distribution to shareholders.

- This $47,160 million is enough to quilt dividends of $41,371 million, leaving an adjusted internet running surplus after dividends of $5,789 million. In this foundation, dividend payout ratio is 87.7%.

- Factor of stocks by means of inventory reimbursement successfully raised $8,659 million thru the problem of 163.9 million stocks to team of workers at a median marketplace worth of $52.83 in step with percentage (with out those problems this team of workers reimbursement would have required money of $8,659 million to supply an identical reimbursement get advantages (ignoring differing tax remedy for money as opposed to inventory reimbursement). Those team of workers percentage problems had been offset partly by means of repurchase of 98.9 million stocks for $5,195 million at a median worth of $52.53 in step with percentage. The online impact of stocks issued to team of workers much less stocks repurchased used to be an build up in shareholders’ price range of $3,464 million ($8,659-$5,195).

- The foregoing research presentations the $9,253 million internet build up in shareholders’ price range in step with Desk 3.1 above used to be made from the $3,464 million internet capital raised thru factor of stocks to team of workers offset by means of percentage repurchases, plus the adjusted internet running surplus after dividends of $5,789 million.

Coca-Cola: Abstract and Conclusions

The present dividend yield is 3.04% and dividend yield on value is projected to develop to a few.6% by means of finish of 2027, underpinning doable returns. There additionally seems to be a possibility for percentage worth good points from EPS expansion, which may well be additional magnified by means of a couple of expansions. Desk 2 above presentations a possible for 10% plus returns from purchasing now and keeping thru finish of every of years 2024 to 2027. In this foundation Coca-Cola is still rated a Purchase. The one caveat is the potential of Coca-Cola failing in its enchantment to Tax Courtroom choices upholding IRS claims for billions in tax bills in terms of the Brazilian operations. As mentioned above, an destructive result may have a vital destructive affect on percentage worth. On the other hand, Coca-Cola seems moderately able to assembly those doable bills from a liquidity standpoint. Additionally, a shareholder ready to carry long term would most likely reach decrease, however nonetheless certain returns, because of dividends and proceeding EPS expansion.