A_Columbo/ iStock through Getty Images

Intro

The cement sector has actually exceeded my expectations in 2023 and in a current short article I released on Titan Cement ( OTC: TTCIF), I described that although the very first 9 months of 2023 were strong, some business began to caution of a weaker need in Q4 2023 and Q1 2024. Buzzi is a bit more positive as the business prepares for that government-mandated building activities will alleviate the effect of lower need from domestic building activities. Buzzi ( OTCPK: BZZUF), an Italy-based cement manufacturer where the Buzzi household owns in excess of 50% of the shares, anticipates a quite steady outcome moving forward. Which’s not always a bad thing as I believe the business is trading at a quite appealing appraisal even if there is no instant development to be anticipated. I formerly discussed this business in 2019 in my ‘ Concentrate On Europe’ short article series

Yahoo Financing

Buzzi’s main listing is on Euronext Italy where it is trading with BZU as its ticker sign on the Milan stock market. The typical everyday volume is practically 190,000 shares, making the Milan exchange without a doubt the most liquid exchange to sell the business’s securities. The Milan listing likewise has alternatives readily available. The business presently has 185 shares impressive, leading to a market capitalization of around 5.3 B EUR. I will utilize the Euro as the base currency throughout this short article.

The European cement sector stays extremely strong

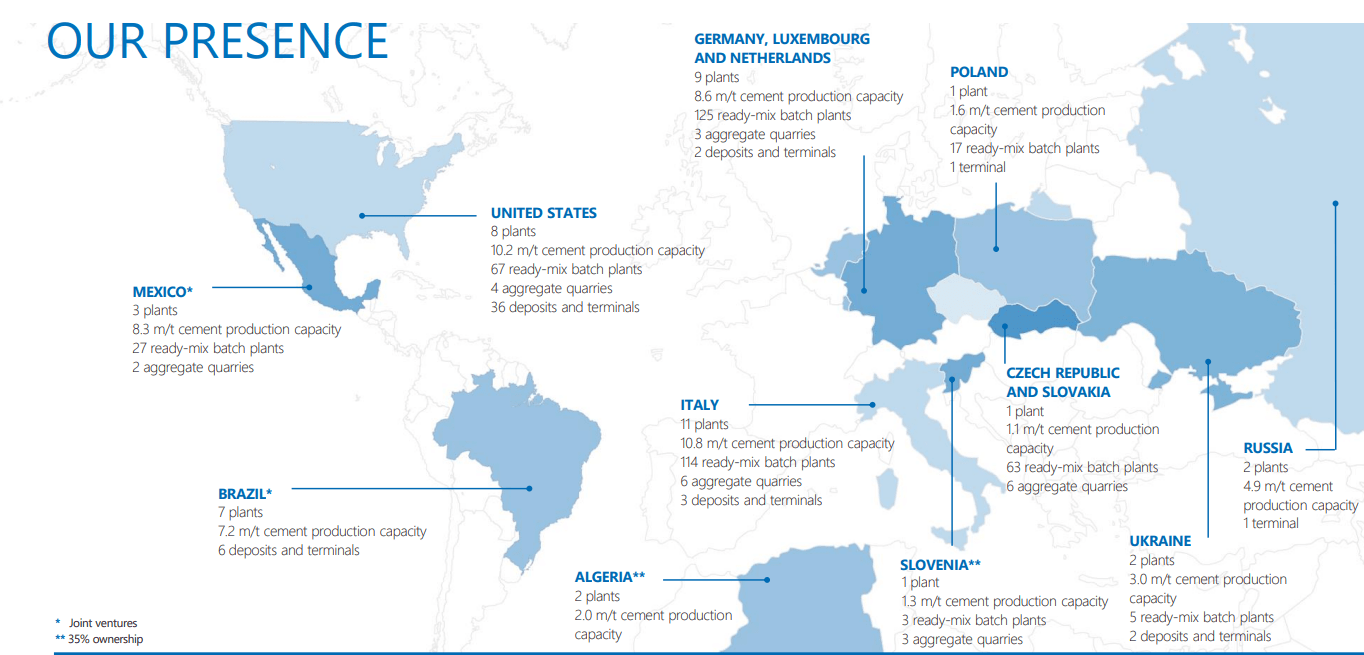

As described in my just recently released short article, Titan Cement’s monetary efficiency was quite strong in the very first 6 and 9 months of the year and although Buzzi discussed the ‘worldwide financial activity continued to be punished by the determination of inflation’, its monetary efficiency stayed extremely strong throughout the very first 9 months of the year. Luckily, the business has a around the world existence which assists to alleviate the effect of some economies being weaker than others.

Buzzi Financier Relations

As Buzzi just releases in-depth monetary outcomes, I will initially take a look at the in-depth financials supplied in the H1 2023 report before taking an action back and take a look at the Q3 trading upgrade (which does not include an in-depth earnings declaration or capital declaration).

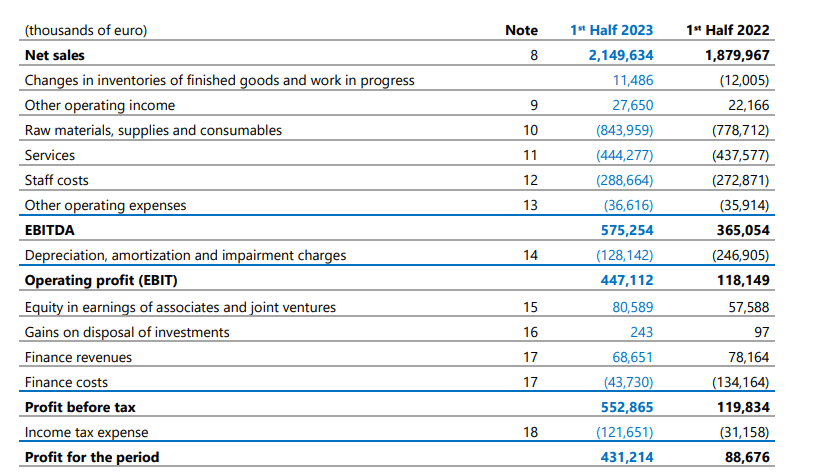

Throughout the very first half year of 2023, Buzzi reported an overall profits of 2.15 B EUR, a great boost compared to the 1.88 B EUR in the very first half of 2022. The EBITDA leapt by in excess of 50% thanks to the business having the ability to keep its COGS under control (these increased by less than 10%) while the SG&A costs increased by simply over 3.2%.

Buzzi Financier Relations

The extremely strong EBITDA result clearly likewise led to a really strong net outcome. As the earnings declaration above programs, the EBIT was available in at 447M EUR which was practically 4 times greater than the H1 2022 EBIT however that’s not a reasonable contrast as Buzzi reported a nine-digit problems charge throughout the very first term of 2022.

In any case, Buzzi’s bottom line reveals a quite remarkable outcome with a net earnings of 431M EUR for an EPS of 2.33 EUR. A really remarkable outcome thanks to the margin growth. Whereas Buzzi reported an EBITDA margin of 19.4% in the very first half of 2022, this increased to practically 27% in the very first half of the present fiscal year.

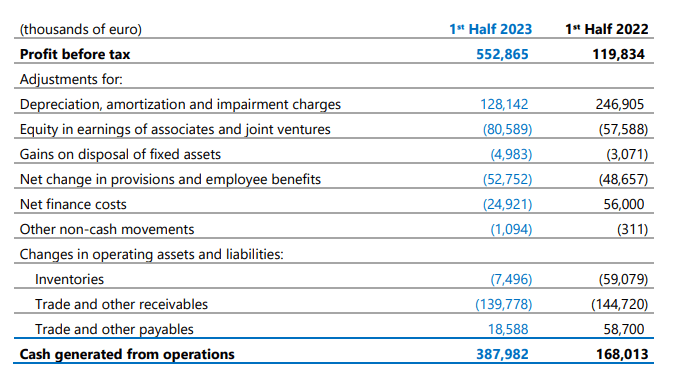

And the capital declaration validates these weren’t simply paper revenues as Buzzi take advantage of a really strong money inflow too. The beginning point of the capital declaration is the ‘money created from operations’ which was available in at 388M EUR however thankfully, the footnotes to the monetary outcomes include more information on how the business gotten this outcome.

Buzzi Financier Relations

According to the footnote, the 388M EUR in money created from operations consists of a 129M EUR financial investment in the working capital position. This implies the operating capital before working capital modifications wasn’t 305M EUR as revealed listed below, however around 434M EUR. That being stated, Buzzi just paid 63.3 M EUR in money taxes although it owed the tax male in excess of 120M EUR based upon the H1 gross income. I choose to subtract the 58M EUR inconsistency and am likewise subtracting the 11.3 M EUR in lease payments. This leads to a hidden operating capital of 364M EUR.

Buzzi Financier Relations

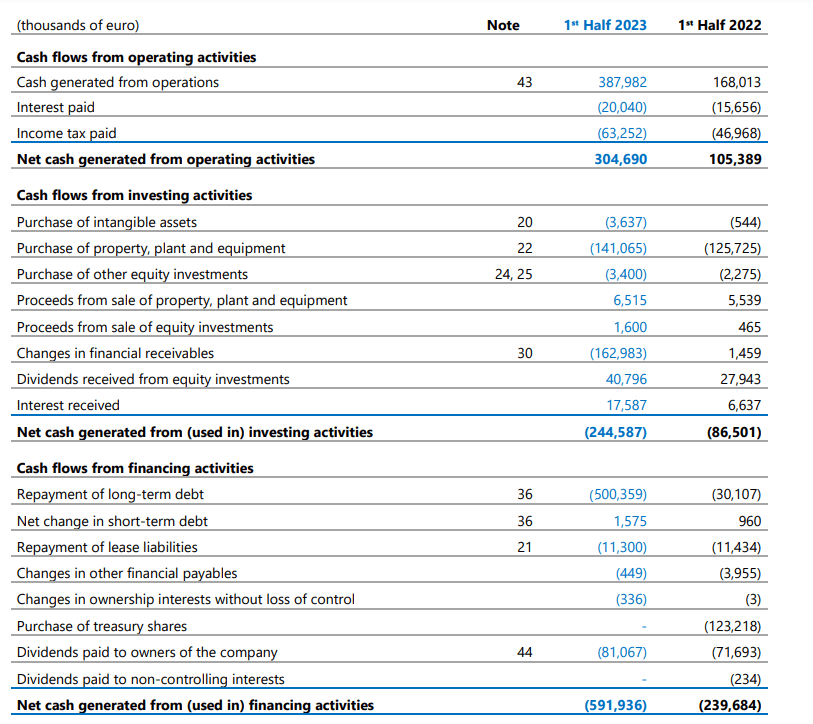

The overall capex was around 141M EUR, as revealed listed below, however these financial investments were mostly compensated by the 58M EUR in dividend and interest earnings. This implies the underlying complimentary capital in the very first half of the year was around 281M EUR. Divided over a share count of around 185M shares, the FCFPS was 1.52 EUR. Lower than the reported earnings however the description is quite basic: Buzzi reported an overall capex + lease payments of 153M EUR while the overall devaluation and amortization expenditure was simply 128M EUR. Furthermore, the net equity profits of partners and JVs surpassed 80M EUR however just 40.8 M EUR was efficiently paid as a dividend.

In any case, Buzzi remains in an outstanding position to continue to take advantage of a fairly steady need for its cement items. And even if 2024 is a bit more unsure, its incredibly strong balance sheet must assist the business to browse through unpredictable times without excessive of an effort. At the end of June, Buzzi had 787M EUR in money on the balance sheet and simply over 560M EUR in financial obligation, leading to a net money position of practically a quarter of a billion euros.

The net money position even enhanced in the 3rd quarter as the business verified a net money position of 673M EUR This shows the business’s 3rd quarter was likewise quite strong (and it is a pity no in-depth monetary outcomes were released) while a part of the working capital aspects were most likely transformed into money.

Financial investment thesis

Using the Q3 net money position, Buzzi’s business worth is simply 4.7 B EUR and with an expected EBITDA of 1.15 B EUR (the midpoint of the main assistance) and an EBITDA of 1.13 B EUR leaving out lease amortization, the business is still trading at simply over 4 times EBITDA which is quite low-cost for a recognized business with no monetary sadness. Taking a look at the agreement price quotes, Buzzi’s EBITDA is anticipated to stay steady which implies that the strong money streams in mix with the reasonably low dividend (0.45 EUR payable over FY 2022) will lead to the net money to increase by a nine-digit quantity annually. The agreement price quotes are pointing towards a net money position of 1.8 B EUR by the end of 2025 which would decrease the business worth to simply 3B EUR and the EV/EBITDA to simply 3.

This makes Buzzi a fascinating prospect for a family-led take-private offer. There are just 83.2 M shares that aren’t owned by the Buzzi household. This implies the year-end net money of 1.8 B EUR by 2025 in addition to including some take advantage of to the balance sheet would lead to the Buzzi household having the methods to introduce a go-private deal.

That is, nevertheless, not my base case situation. I am simply wanting to develop a long position to ideally take advantage of a re-rating. Holcim ( OTCPK: HCMLF) ( OTCPK: HCMLY) and Heidelberg Products ( OTCPK: HDELY) ( OTCPK: HLBZF) are presently trading at 6.5 and 5 times EBITDA respectively. If I would use a several of 5.5 times the EBITDA of 1.2 B EUR by the end of 2025, the reasonable business worth would be 6.6 B EUR. Including 1.6 B EUR in net money (which has to do with 12% listed below the agreement approximates net money position) would then lead to a reasonable market capitalization of 8.2 B EUR which exercises to 44 EUR per share. Discounting that back by 9% annually previously leads to a reasonable worth of 36-37 EUR per share versus the present share rate of simply under 29 EUR. This implies I will likely start a long position in Buzzi in the next couple of weeks or months as I believe any weak point in its share rate might be a buy chance.

Editor’s Note: This short article goes over several securities that do not trade on a significant U.S. exchange. Please understand the threats connected with these stocks.