CaÃque de Abreu

Xeris Biopharma Holdings ( NASDAQ: XERS) is an intriguing biotech business that has actually made substantial strides in establishing and advertising treatments throughout a variety of fields.

I believe XERS is a speculative buy with some truly strong income development trading at an affordable assessment relative to sales and sales development. It has drastically diminished its losses and seems near to breakeven.

Nevertheless, as a little cap business (market cap is approximately $300 Million) that is not presently successful, the typical cautions use with concerns to little cap investing. Furthermore, as rates increased throughout 2022 and 2023, financiers have actually ended up being more critical with buying unprofitable business.

Ensure that you place size this properly if you do choose to acquire it. I likewise believe there’s a much better method to approach a position in XERS (see listed below) that decreases danger.

Xeris’s focus is on endocrinology, neurology, and gastroenterology with their exclusive formula platforms called XeriSol and XeriJect Both XeriSol and XeriJect address constraints of liquid formulas for specific drugs. They’re planned to have high stability and solubility.

XeriSol and XeriJect

XeriSol: XeriSol is a non-aqueous formula innovation that makes it possible for the subcutaneous and intramuscular shipment of extremely focused, ready-to-use formulas.

Subcutaneous shipment is shipment of drugs into the layer of fat that is in between the muscle and the skin. This kind of shipment is perfect for slow-release drugs into an individual’s blood stream. This is utilized for insulin for diabetics, human development hormonal agent and drugs for rheumatoid arthritis.

Intramuscular shipment is shipment of drugs straight into a muscle. This kind of shipment is perfect for faster absorption and is utilized for influenza and vaccine shots.

XeriSol intends to enhance the service life and stability of drugs. Usually, liquid drugs deteriorate relatively rapidly so the difficulty is enhancing their service life. XeriSol eliminates the water from the formula, therefore making the drug have a longer service life.

XeriJect: XeriJect is another exclusive innovation by XERS that concentrates on the formula of injectable drugs. It is created to transform typically freeze-dried drugs into steady liquid types. XeriJect assists in streamlining the drug preparation procedure, lowering the capacity for dosing mistakes, and enhancing client compliance.

Clients who take advantage of XeriJect consist of those who count on drugs that are usually offered in freeze-dried types and need blending before injection. XeriJect utilizes an exclusive strategy to change these drugs into ready-to-use liquids. This is particularly crucial for clients who self-administer their medications in your home or have minimal access to medical centers due to the fact that the administration of these drugs is a lot easier in liquid type.

What is “liquid formulas”?

Liquid formulas in drugs describes where the main solvent is water, which prevails in the Pharma market. They can consist of services, suspensions, and emulsions.

-

Solutions: In a liquid option, the drug is entirely liquified in water. These are clear liquids where the active component is dispersed throughout the option. Believe: oral cough syrup consisting of a drug that is entirely liquified in water together with other components like flavorings or sweeteners. These are frequently utilized for young kids or senior due to the fact that of their ease of administration.

-

Suspensions: A suspension is a formula where the drug particles are distributed in water however not entirely liquified. These generally need shaking before usage. An example is prescription antibiotics. Amoxicillin isn’t completely liquified in the water and needs shaking before administering to ensure the drug is dispersed throughout the liquid. Flavorings are likewise contributed to these and they’re likewise more effective due to the fact that they can be simpler to swallow.

-

Emulsions: An emulsion is a mix of 2 liquids (like oil and water), where one is distributed in the other in the type of small beads. These drugs generally consist of both oil and water stages and the drug is liquified in either stage. An example is a topical cream like hydrocortisone. hydrocortisone is distributed in a cream base which includes water and oil.

Kinds of liquid formulas ( Kinds of liquid formulas)

Source: Author

With that quick Science 101 class out of the method, let’s dive into what it is that Xeris does and see if it’s a worthwhile financial investment.

Commercially Authorized Drugs

The business now has actually 3 commercially authorized drugs – Gvoke, Keveyis and Recorlev – which integrated to produce $42 Million in earnings in Q3 2023, up 41% year on year.

Gvoke is a prepared to utilize glucagon item called Gvoke HypoPen and its earnings grew 30% year on year while prescriptions were up 52% in the very same period. The business thinks it has actually just scratched the surface area of the chance for this drug as they state that just 10% of individuals at danger for an extreme hypoglycemia occasion even have a glucagon drug offered on hand. They approximate this market to be as big as 15 million individuals (vs prescriptions of 58,000 in Q3 2023).

Recorlev earnings were up an impressive 221% in Q3 2023 to $8.1 Million. Recorlev reduces cortisol production and is viewed as a first-line treatment for Cushing’s syndrome post-surgery. Cushing’s is an endocrine condition triggered by extended direct exposure to high levels of the hormonal agent cortisol. It frequently arises from a benign growth in the pituitary gland and prevails among ladies. It is deadly if left unattended.

Keyevis earnings were up 19% year on year to $15.9 Million. Keyevis is a substance abuse to deal with main routine paralysis. This condition impacts muscle function, resulting in episodes of muscle weak point or paralysis. The drug is administered orally in tablet type.

Pipeline

XeriSol levothyroxine, a possible once-weekly sub-Q injection, remains in a stage 2 research study for the treatment of hypothyroidism. Registration started in Q2 2023 and has to do with 80% registered. The business intends to finish the research study in 1H 2024 with information offered in mid year. That will notify them on transferring to stage 3.

Collaborations

XERS has some notable partners utilizing the XeriJect platform, consisting of Amgen ( AMGN) and Regeneron ( REGN). Here is a quote from their Q3 2023 teleconference:

” We revealed that we effectively created the prespecified target item profile of XeriJect TEPEZZA and as such, we see the associated $6 million success payment from Amgen, which was just recently gotten by– which just recently obtained Horizon. We are waiting on their choice whether they wish to exercise their alternative for an unique license to XeriJect innovation in the main sign to enhance the advancement of XeriJect subcutaneous TEPEZZA. If the alternative is performed and Amgen continues medical advancement and ultimate commercialization of XeriJect sub-Q TEPEZZA, we might be entitled to get advancement turning points, regulative turning points, sales-based turning points and royalties based upon future sales. When it comes to the Regeneron partnership, we are presently creating the 2 particles of the platform program and anticipate to provide the prespecified XeriJect formulas for examination to Regeneron. Regeneron likewise has the alternative to choose extra particles for formula advancement at any time or to carry out a license for additional medical advancement and commercialization of any of the particles in the platform. In addition, we continue to go over extra XeriJect partnerships with many business.”

Source: Q3 2023 Quarterly Teleconference

Monetary Efficiency

The business has actually seen explosive income development from 2019. 2019 earnings were simply 2.7 Million. Here is the development in earnings ever since:

2019: $2.7 Million

2020: $20.4 Million

2021: $49.6 Million

2022: $110.2 Million

2023 (approximated): $162.5 Million

XERS Profits (Author) ( XERS Profits (Author))

Profits have actually grown at a CAGR of 178%.

The business hasn’t yet turned a GAAP earnings; nevertheless, operating earnings margins have actually enhanced substantially. Here are the operating losses by year:

2019: -$ 122.4 Million

2020: -$ 83.5 Million

2021: -$ 115.2 Million

2022: -$ 81.9 Million

2023 (TTM): -$ 49.3 Million

In Q3 2023, the business reported a GAAP operating loss of simply $4.9 Million on earnings of $48.3 Million. Running margins went from unfavorable 4,000% in 2019 to simply unfavorable 10% in Q3 2023.

The business is presently burning around $15 Million per quarter; nevertheless, money burn has actually been boiling down. They have about 4 quarters of money left and have $190 Million in long term financial obligation. I do not like the balance sheet and do anticipate that they will need to do another cap raise to money operations till breakeven.

The business isn’t offering assistance yet for 2024:

We likewise continue to keep a healthy money position, which supports our capability to continue to be a self-sufficient business. We are not offering 2024 monetary assistance at this time. Nevertheless, I wish to share a fast top-level outlook. We anticipate overall net income to grow from 2023 levels, business expenses to stay flat, continuing to minimize our money burn, and to once again have sufficient money at the end of the year to money our business, fulfill our responsibilities and continue to purchase the development of the business.

Source: Q3 2023 Quarterly Teleconference

Having stated that, the business trades at a low cost to sales of simply 1.9 X and if they can get to stabilized earnings margins of around +10%, the business trades at about 20X stabilize earnings margins on $162.5 Million in earnings. With income development in the 40% variety, this is a numerous that appears rather sensible.

Conclusion

I like this business. The assessment appears sensible, the business is growing really quickly. Nevertheless, I do believe they will be required to do another capital raise to bridge the space to success. If the stock increases, I hope they do a smaller sized raise and do not water down investors that much. I believe a $30 to $50 Million capital raise appears sensible eventually unless they enhance money burn significantly.

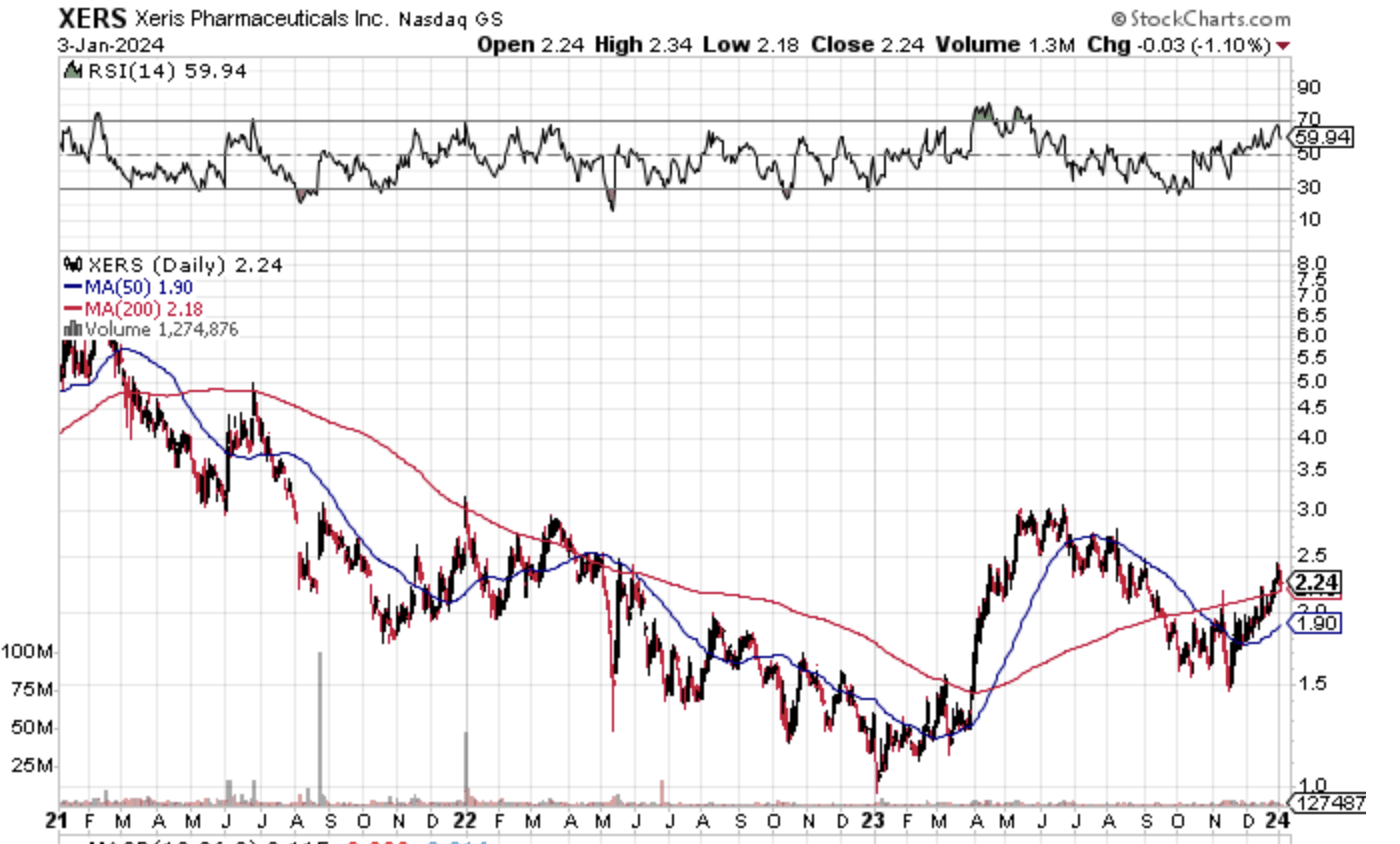

The chart looks great for a turn-around. The 200-day moving average has actually been increasing considering that last spring, and the stock simply recently cleared the 200-day moving average. I believe you can purchase some here and wait on Q4 2023 results to come out a long time in early 2024 to either contribute to the stock or offer it. I presently have no position, however will be enjoying it carefully.

XERS Stock Chart ( XERS Stock Chart)