FilippoBacci

I’m back! I took the majority of the month of December off, as I do every year, to do some thinking. Per the title of this essay, the function of these year-end musings is to get some point of view. In the everyday, week-to-week, motions of the marketplaces it is simple to forget that we are investing with a timeline determined in years, and for lots of financiers, years. I compose a commentary weekly for 11 months of the year and I seldom do not have for something to blog about; there’s constantly something happening with the possible to effect markets and portfolios. A lot of weeks however, to be truthful, the news isn’t truly all that crucial for financiers. You can follow the financial reports as they’re launched however the majority of them are going to have to do with as anticipated. Yes, some will be off the agreement by a little, however does it truly matter if the current inflation figure was 0.1% greater or lower than “expectations”? The response to that is certainly no given that whatever is reported this month will get modified next month and most likely a number of times after that. The accuracy we desire in financial reports simply isn’t offered in real-time. Do you truly wish to tweak your portfolio based upon information that isn’t precise?

There are other matters that impact our financial investments, obviously, however the majority of them not as much as we believe. Politics can have an effect however the modifications from administration to administration tend to be incremental and the results are undoubtedly overemphasized by political leaders of both celebrations. Presidents simply do not have the power they or their advocates picture and both celebrations undergo the exact same lobbying from the exact same quarters. Washington, D.C. is simply as much a cesspool today as it was 100 or 200 years earlier, and I extremely advise disregarding the majority of what transpires there. Far more crucial than politics is the development from the economic sector that continues despite which celebration is in power. Scientific improvements over the last few years have actually been absolutely nothing except remarkable, and it makes me positive about the future. However it requires time and a great deal of experimentation to find out how brand-new discoveries will be used to enhance our efficiency, our lives, and our society. The majority of the capital bought the early years of the Web was squandered however what endured and adjusted made a big distinction in our lives. Social network is evidence that, years later on, it is still a continuous procedure. The exact same will likely show real of improvements like mRNA innovation, gene modifying, expert system, and other current advancements. To put it simply, the influence on the economy will be progressive; you do not need to hurry.

That does not suggest we must simply disregard the economy, although a little point of view does can be found in useful. There are legions of “experts” on Twitter and TikTok and blog sites who are more than delighted to make use of the current financial release to get you to part with some hard-earned money to register for their service. Social network has actually degenerated into mental warfare with masters (noticable “charlatan”) pontificating on the current financial release and how it validates their view of the world even when it does not. The only guideline for masters appears to be that a person can never ever confess to being incorrect. If the current information point is so certainly counter to their previous pontifications, they’ll move to some arcane topic that no sane individual can potentially understand – least of all the masters themselves – and discuss why that suggests that they’ll be vindicated in the end, simply you wait and see. With all this allowin’, reckonin’, and speculatin’ going on (as my dad utilized to state), withstanding the temptation to do something when you must most likely be not doing anything is harder today than ever previously. The only method to prevent the temptation is to get a little, you thought it, point of view.

This time of year, there are hundreds (thousands?) of financial and market outlooks offered, all concentrated on what is going to occur over the next 12 months. These “outlook” pieces are incredibly comparable from company to company, showing that task security on Wall Street is frequently discovered in agreement. They are likewise extremely comparable year to year (stocks are constantly anticipated to carry out near the long-lasting average although they never ever do) and this year is no exception, with a style incredibly comparable to in 2015’s – which ended up being stunningly incorrect. Everybody sees the economy slowing down, most to a soft landing, others to a moderate economic crisis, a couple of others to a tough landing, and a couple of outliers requiring something outside the standard (if in the beginning, you do not be successful …). Bonds are the favored financial investment lorry as the Fed and other reserve banks are commonly anticipated to cut rates as the economy slows. Quality stocks are to be stressed (exist times we should highlight low-grade stocks?) and the United States is typically the location to be, regardless of “difficult” assessments, as a number of companies put it so delicately.

Markets presently show the agreement of a slowing economy with Fed Funds futures presently revealing a 69% possibility that the over night loaning rate will be up to a variety of 3.5-4.25% by December 2024. That expectation of rate cuts next year is what moved stocks in the fourth quarter of in 2015; a lower discount rate suggests financiers can put a greater worth on future, frequently speculative, revenues. Obviously, revenues might be adversely impacted by a slower economy however if the economy prevents economic crisis, revenues should not be impacted that much. Certainly, if rates fall due to the fact that inflation continues to fall, margins might broaden, raising revenues regardless of slower small development. And the drop in rates, a minimum of up until now, does not suggest an economic downturn.

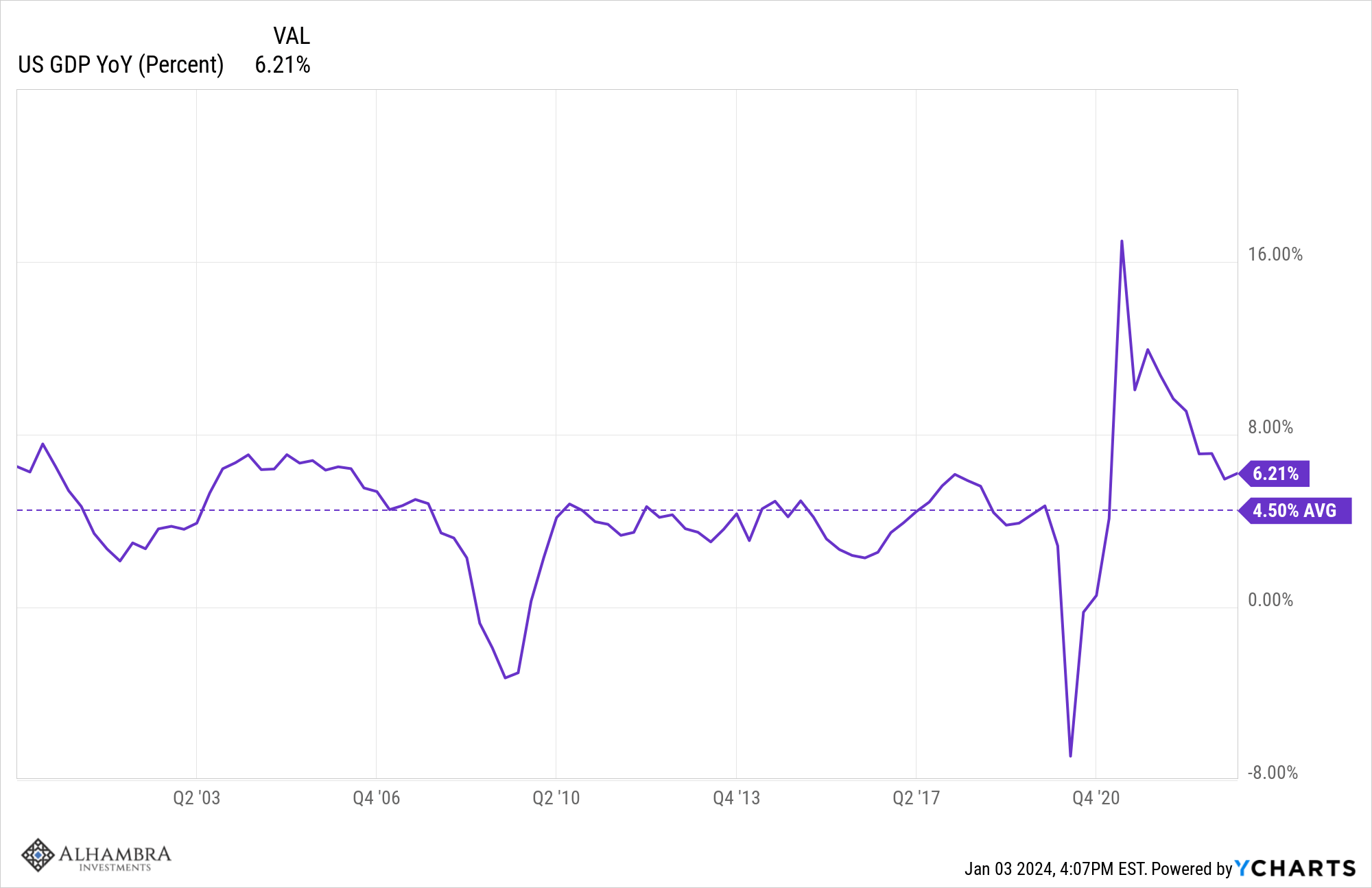

The 10-year Treasury rate is an excellent proxy for small GDP development and at the existing 4%, the bond market is simply considering a go back to trend genuine development of 1.8-2%. The year-over-year modification in NGDP after Q3 2023 was 6.2% and if inflation is going to continue to moderate that needs to boil down. NGDP is inflation + genuine development, however we never ever understand what the split is going to be. Over the in 2015 though, NGDP fell completely due to a fall in inflation. In Q3 2022, NGDP was up 9.1% yoy which was up to 6.2% in Q3 2023 while RGDP development increased from 1.7% to 2.9% yoy. The marketplace appears to be wagering that it will be duplicated and it might occur. Today the very best price quotes we have for genuine development and inflation for Q4 2023 originated from the Atlanta Fed’s GDPNow and the Cleveland Fed’s Inflation Nowcasting. Utilizing those 2 price quotes puts Q4 NGDP at 4.3% with 2.5% genuine development and 1.8% inflation.

What all that suggests to me is that the economy is going back to “regular” or what passes for it in the 21st century. The typical year-over-year modification in NGDP given that 2000 has actually been 4.5%.

That’s all we understand today, that the economy is almost back to its pre-COVID standard. That isn’t an unimportant accomplishment by the method and one that very few individuals anticipated. It appears quite apparent in retrospection given that COVID didn’t completely affect the important things that produce financial development – labor force development and efficiency development. The federal government loaning and investing a considerable amount of cash does not move the needle on either among those (other than perhaps in an unfavorable method). There have actually been some positives, mainly in the kind of home and business balance sheets, however the compromise was a worsening of the general public fisc; there are still no complimentary lunches. From a macroeconomic point of view, I believe that is a minor favorable however mainly a wash. Labor force development isn’t going to increase considerably due to the fact that it can’t, missing a huge modification in migration policy. Efficiency development, on the other hand, might well be the surprise of the next years or two. Innovation is the secret, and it appears to be bearing down a number of fronts, from AI to robotics.

Shorter-term, with everybody searching for a financial downturn, the surprise might be that we do not get much of one. Inflation is, at this moment, back to regular. Yes, rates are still raised over pre-COVID, however if you’re anticipating the Fed to tighten up enough to press rates pull back, you require to change your expectations. That simply isn’t going to occur. The 3-month modification in PCE inflation struck its peak in March 2022 at 1.97% and has actually given that been up to 0.35% in November 2023. The three-month modification in Core PCE inflation peaked in December 2021 at 1.61% and has actually been up to 0.54% in November 2023. The last 5 procedures of the three-month modification given that July are 0.58%, 0.39%, 0.55%, 0.58% and 0.54%. Perhaps there is more problem to come, however that appears like inflation has actually supported to me. Considered that and considered that existing financial policy is at least rather tight (see genuine rates of interest), the Fed might well feel warranted in an easing of policy. As I stated, existing levels of PCE inflation have to do with as regular as you can get, at best about the average given that 1990:

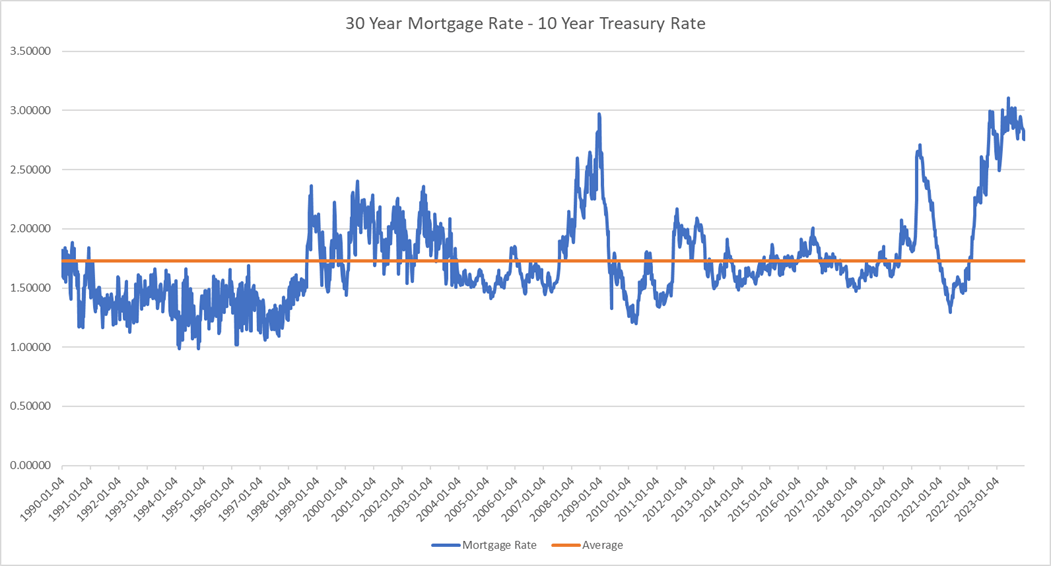

If the Fed does reduce and long-lasting rates of interest simply support at existing levels, there is the capacity for an upside financial surprise that does not worsen inflation. The only location of the economy hit in any considerable method by greater rates of interest was realty. With many house owners resting on home loans with 2 or 3 as the very first digit, existing home sales have actually cratered. Home mortgage rates rise due to the fact that of the Fed’s rate walkings, however they are even greater due to the fact that the spread in between the 10-year Treasury and the 30-year home loan rate is larger than regular:

The typical spread given that 1990 is 1.72% versus the existing 2.75%. If the 10-year rate stays where it is and the spread narrows to typical, the 30-year home loan rate would fall from the existing 6.6% to 5.6%. While that isn’t 3%, it is a lot less than the 7.8% peak in October of in 2015. I do not understand just how much real estate motion a drop like that would stimulate, however the best response definitely isn’t no. If home loan rates do fall that much, more activity in the real estate market might be a huge increase to the United States economy. Not just would more budget-friendly homes suggest more structure activity, however more current home stock might well keep rates in check. The ripple effects might consist of increased home enhancement activity and resilient products purchases related to real estate activity. The wholesale inventory/sales ratio is still raised from the COVID supply chain concerns, however stocks have actually succumbed to 11 months in a row. An uptick in sales related to real estate might quickly reduce the ratio and stimulate brand-new orders for a production sector that has actually remained in idle for over a year. All of that is speculative, obviously, and extremely depending on rates of interest a minimum of not increasing much from here, however if inflation really is tamed, a minimum of in the meantime, then it ends up being far more most likely.

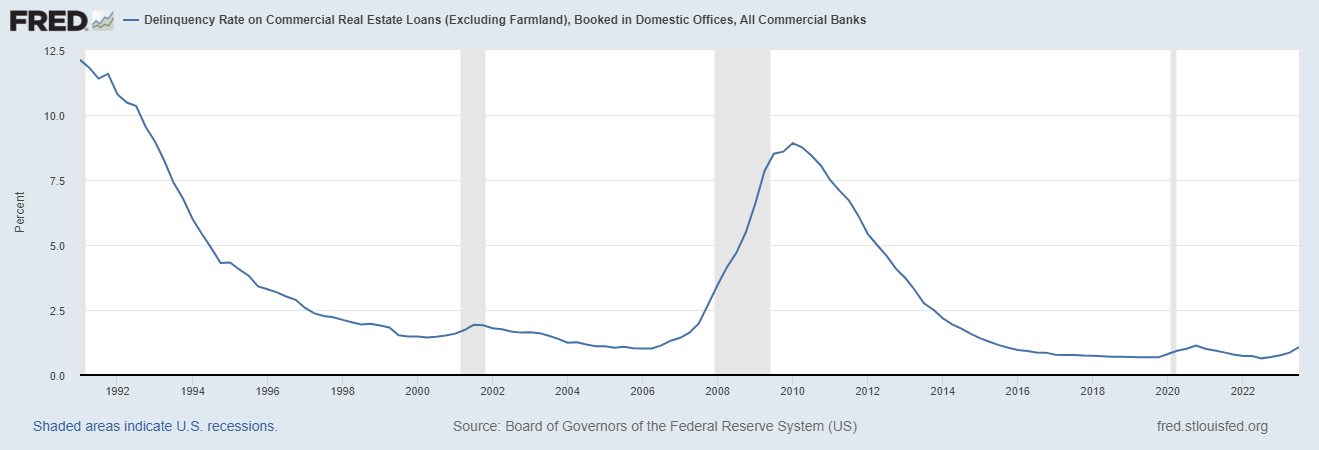

Lower rates would likewise be extremely welcome in industrial realty. Poor quality deals done over the last couple of years at extremely low rates are currently spoiling as cap rates increase and refinancings come due. While I do not believe openly traded REITs are much of an issue (with the exception of a few of the financing REITs which we prevent) most industrial residential or commercial property is independently owned. Banks have direct exposure there – although not as much as you may think from the headings in 2015 – however lower rates would resolve a great deal of these issues simply as they are resolving a great deal of the banks’ latent Treasury losses issue. A tightening up of home loan spreads will depend upon banks contending for loans and there is some possible great news there. The senior loan officer studies, carried out quarterly, reveal the portion of banks tightening up loaning requirements (for a range of kinds of loans) peaked in 2015. In any case, the delinquency rate on industrial realty loans is increasing, however it is still quite low, less than the late ’90s and the whole duration till the 2008 crisis.

The United States economy, in the meantime, is back to the pre-COVID development and inflation patterns. I see absolutely nothing in the existing information or market indications that threaten impending economic crisis. Rate of interest have actually come down with inflation, credit spreads are back near the lows of this cycle and as low as they got in the last cycle. Different variations of the small yield curve are still inverted, annoying those searching for guaranteed economic crisis indications and still not having much of an influence on the economy. The genuine yield curve, determined by pointers from 5 to thirty years, is flat and has actually been for the majority of the in 2015. Simply an idea, however perhaps genuine rates are more vital than small. We get in 2024 with the exact same worries as in 2015. Let’s hope they show simply as baseless.

Markets

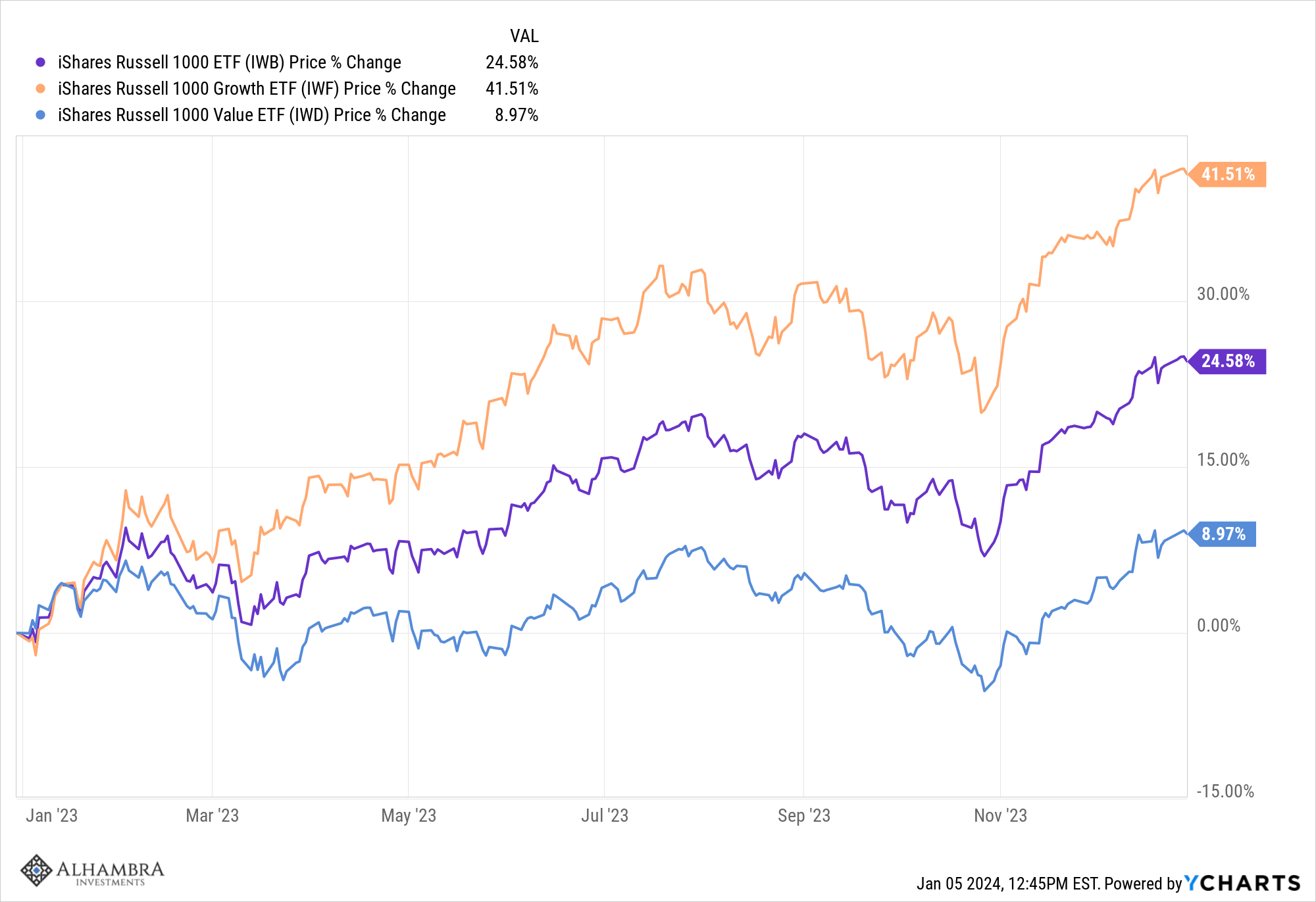

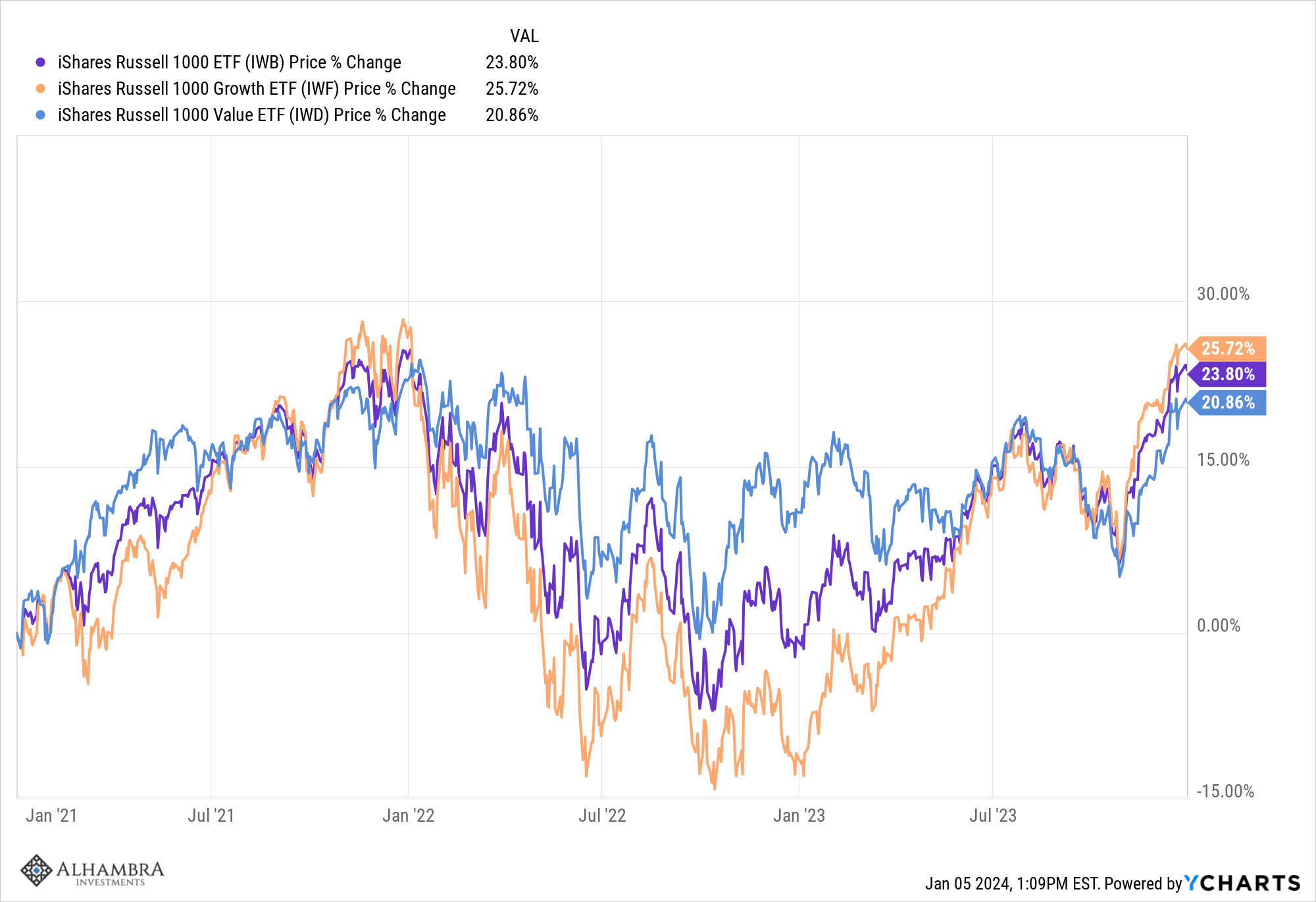

Just like the economy, it assists to zoom out when taking a look at market patterns. The huge news in 2015 was the outperformance of big business development stocks relative to whatever else. The Russell 1000 Development Index was up over 40% in 2015 while the worth part was up almost 9%, which would have been an excellent lead to practically any year however last.

However development’s outperformance in 2015 was simply offseting the huge underperformance the year before. Over the last 3 years, development still surpassed, however the distinction wasn’t almost as broad. More significantly, the trip was a lot simpler in the worth index. From the start of 2021 to the end of 2023, the worth index never ever traded more than 1% listed below the beginning worth while the development index tipped over 14%. The worst peak-to-trough drop – from the start of 2022 – for the worth index was 20% while the development index fell 35%. A 20% drop isn’t enjoyable, however it’s a heck of a lot simpler than 35%.

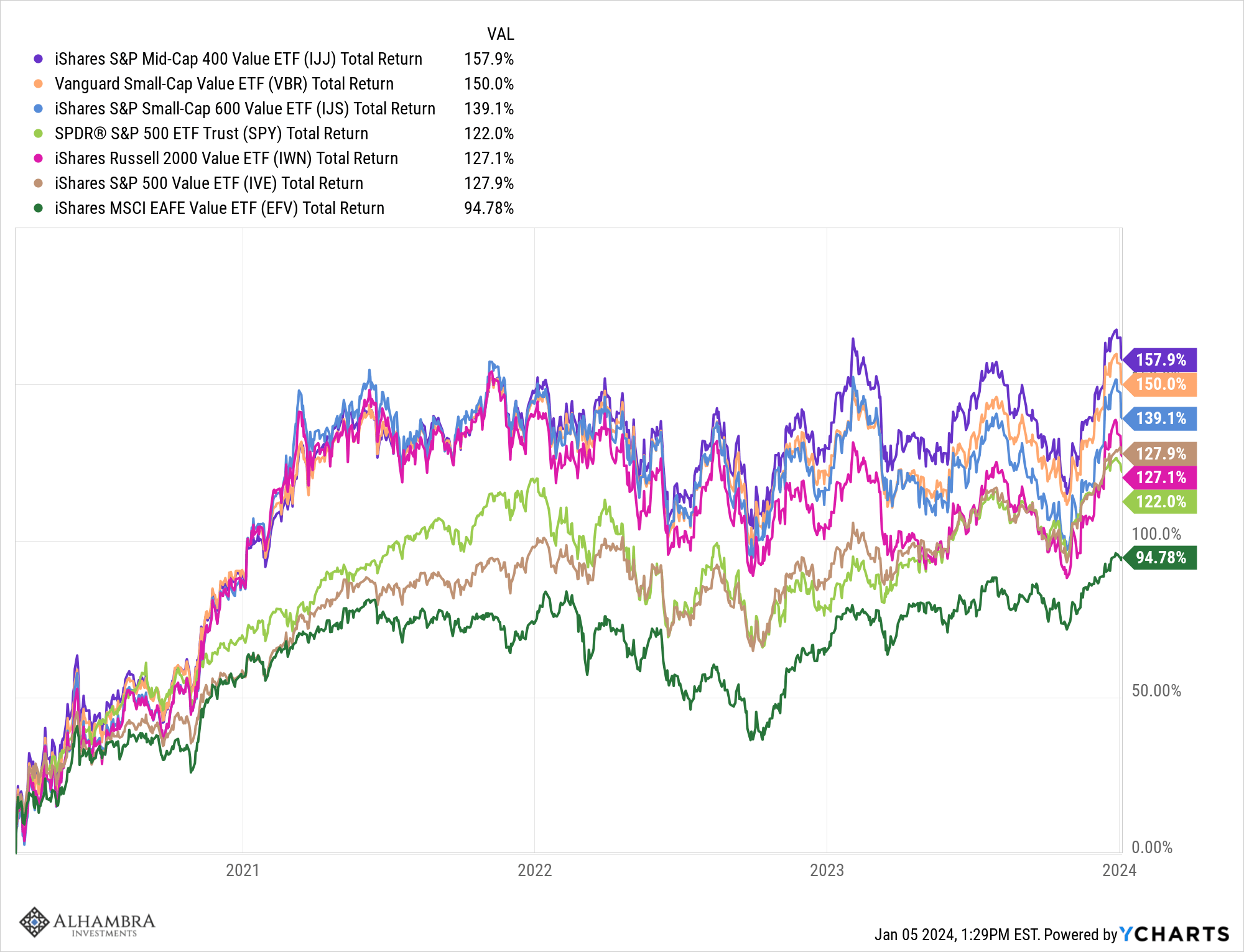

So, yes, if you were a value-oriented financier – and we definitely fit that classification – your portfolios didn’t do in addition to they would have if you had actually moved to development stocks in 2015, however we aren’t truly thinking about short-term patterns; we’re searching for patterns that will last years and we continue to think that the emerging one today favors worth, small/mid-cap, and worldwide. Considering that the bottom of the COVID drawdown in March 2020, worth has actually surpassed development in the S&P 500, S&P 600 (small-cap), S&P 400 (mid-cap), Russell 2000 (small-cap), CRSP United States Little Cap Index (utilized by Lead) and EAFE (worldwide industrialized). After 4 years of outperformance perhaps it isn’t a lot an emerging pattern as a. pattern. All of those worth indexes have actually likewise surpassed the S&P 500 given that the COVID nadir other than EAFE. International returns are greatly affected by the currency exchange rate though and once the dollar peaked in October of 2022, EAFE worth surpassed all the others by a respectable margin. A weaker dollar is another pattern we anticipate to sustain although it is presently oversold and due for a bounce.

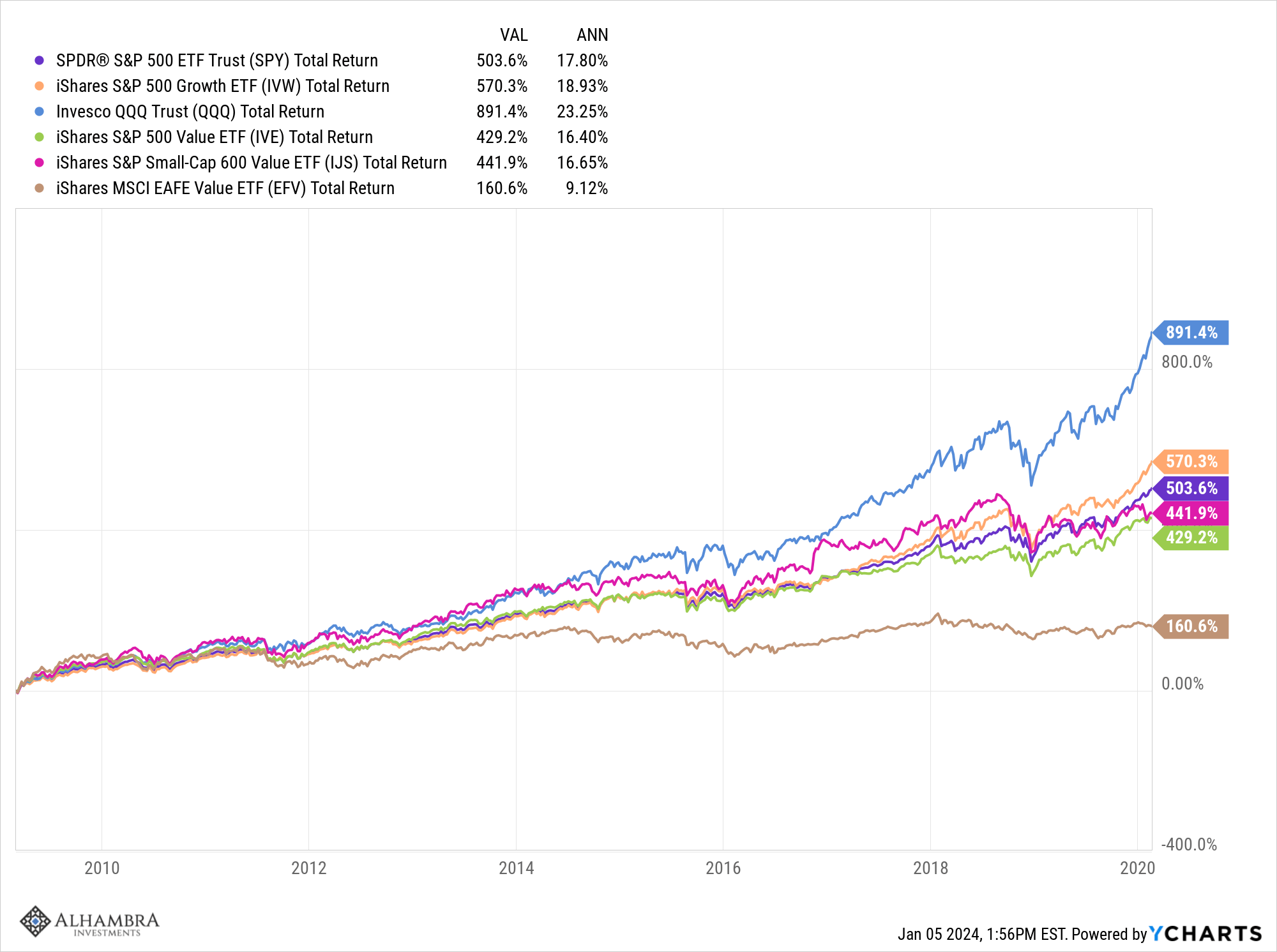

In the period of no rates of interest (ZIRP) and Quantitative Easing (QE), from the lows of the 2008 crisis in March 2009 to the peak in February 2020 at the start of COVID, United States development stocks ruled supreme. The NASDAQ skyrocketed almost 900% (23.25%/ year) while the S&P 500 development index just handled 570% (18.9%/ year). The S&P 500 worth index was adept at 429% (16.4%), however it is likewise now the highest-priced of the above worth indexes. Little and mid-cap worth stocks carried out well, however not in contrast to large-cap development. And worldwide worth, with the dollar increasing for the majority of that time, was the poorest carrying out of them all, increasing a portion of the S&P 500 development index.

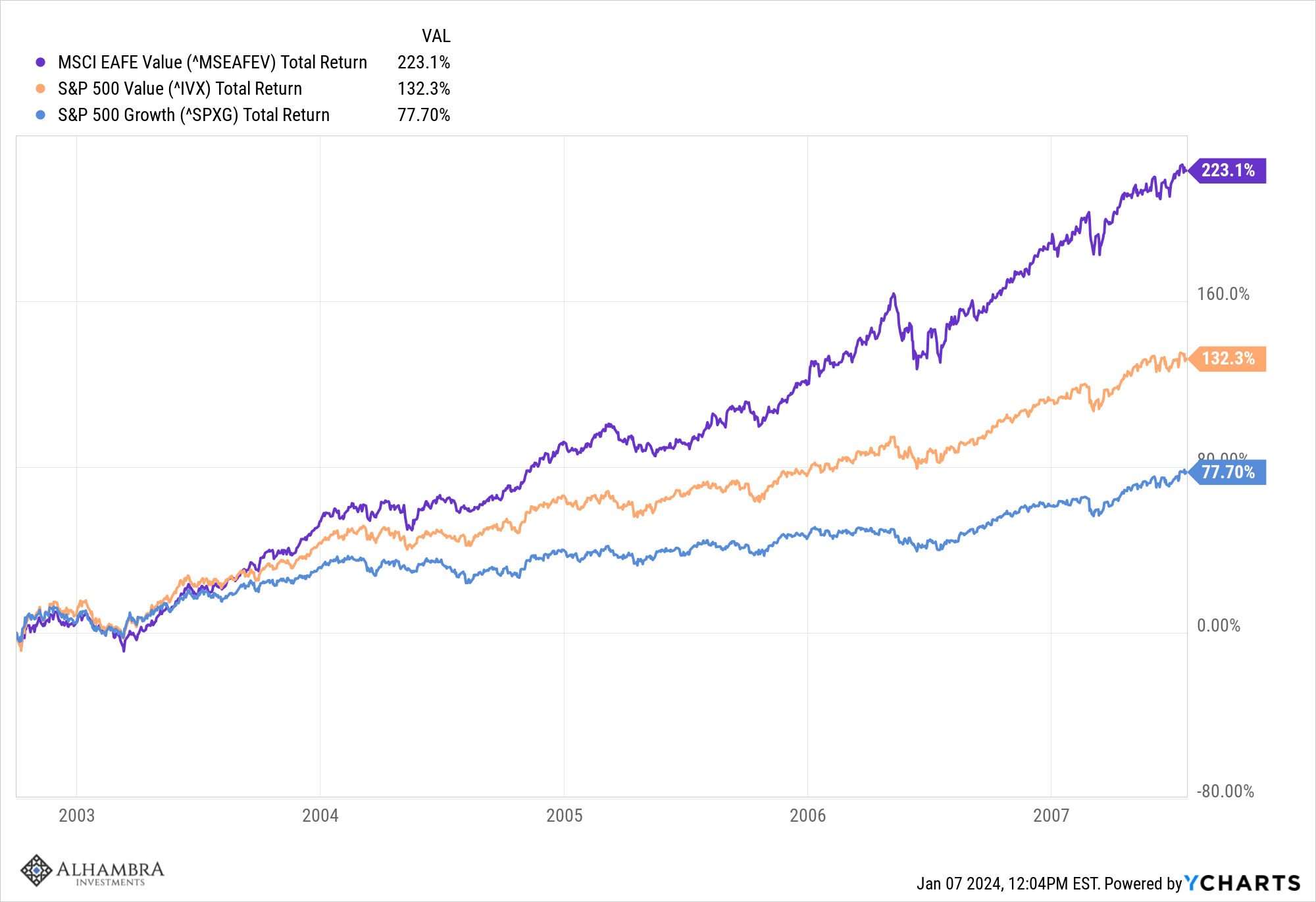

The outperformance of worth or development are patterns that tend to ins 2015. Before the post-COVID growth-dominated duration, we had a five-year duration of worth outperformance with the S&P 500 worth index almost doubling the returns of the development index. And in a weak dollar environment, EAFE worth beat them both by a broad margin.

Getting this one choice right, preferring development or worth at the correct time, can certainly pay massive dividends for financiers. This is the sort of pattern we are attempting to catch, long-lasting shifts that last 5 years or more. These patterns are, to some degree, determined by other patterns like rates of interest and the dollar, however they are truly determined by mindsets. Worth outperformance durations, which follow more speculative development durations, tend to be more sober, and more focused on genuine things. If development outperformance durations are controlled by FOMO (Worry of Losing Out), worth durations are marked by FOMU (Worry of Screwing Up).

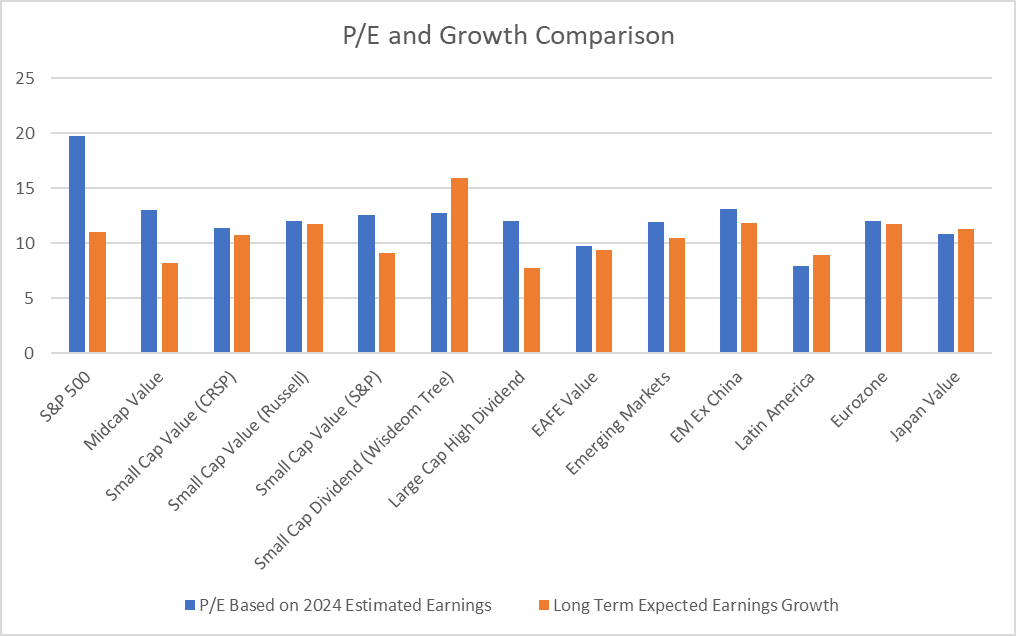

Where development’s current outperformance leaves us today is with large-cap stocks extremely extremely valued and whatever else far more sensible. And within the little, mid, and worldwide options, worth provides the very best risk/reward:

If the long-lasting drop in rates of interest that began in the early ’80s is over – and I believe it is – assessments general promise to fall. The 10-year Treasury yield peaked in late 1981 at almost 16% and began a fall that took it all the method to 0.5% in 2020. The Cyclically Adjusted P/E (Shiller) for the S&P 500 struck its post-Great Anxiety low in August of 1982 at 6.64. By 2021, it was over 38, a level just surpassed by the dot com bubble in 1999 when it struck 44; today it is still over 30. It is not a coincidence that assessments increased as rates of interest fell. Now, I do not occur to believe much of the Shiller P/E as a timing tool – and you should not either – however it does inform you about risk/reward. And I do not believe much of cap-weighted indexes either due to the fact that they are basically momentum methods with the biggest business getting the greatest weightings. In the S&P 500, the outcome is that 30% of the worth of the index remains in the leading 10 names. So a high Shiller P/E does not suggest all the stocks in the index are misestimated. However the leading 10 holdings, which control the index, are truly pricey. The development part of the index is simply a severe variation of the index as a whole. We decided, as a company, to prevent the index because of that in late 2021 which hasn’t altered.

Breaking the long-lasting drop in rates does not suggest they are going to shoot back as much as 16% anytime quickly. There will be cyclical ups and downs, however I believe rates will typically be greater over the next years than they remained in the last. If that holds true and assessments typically move lower, principles are going to matter once again. I believe a great deal of financiers forgot – or never ever found out – what it suggests to be a financier in the ZIRP/QE duration. Whatever simply ended up being a chase for the next hot thing with ETFs for each possible style (or meme). I believe the NFT trend characterizes this period of “investing” where things without any intrinsic worth at all were bid to insane heights. I am still amazed that anybody ever encouraged themselves that a digital picture of a severely drawn animation ape deserved more than a number of dollars. However that’s what occurs when cash is basically complimentary. However as I stated, I believe that period is now over. It’s time to return to the fundamentals of buying genuine business with genuine revenues, capital, and dividends to show it.

Editor’s Note: The summary bullets for this post were picked by Looking for Alpha editors.