Grafissimo/E+ by means of Getty Images

Whether you’re a retail financier or a monetary market specialist, it’s most likely that you recognize with Robinhood ( NASDAQ: HOOD), the leading low-priced retail brokerage platform that went public a couple of years back.

The business was notorious in the monetary neighborhood before the pandemic due to its zero-commission company design, which our company believe required larger incumbents like TD Ameritrade and ETRADE to follow its lead in cutting commission charges to no.

Nevertheless, regardless of the business’s industry-shaping effect, Robinhood ultimately ended up being most well-known for its function in the GameStop ( GME) meme stock trend in early 2021, throughout which the brokerage company briefly avoided clients from acquiring GME stock (and other stocks) as they increased.

While the action was sensible and basically mandated by the NSCC due to HOOD’s little balance sheet, the relocation created a remarkable quantity of debate and triggered numerous conspiracy theories from HOOD’s primary consumer base of retail traders.

In extra to the reputational damage (that the company is still shaking off), the business’s stock has actually likewise had a hard time given that IPO, down more than 85% from its all-time high of $85 per share.

Behind the decrease are concerns around profits predictability, market cyclicality, and high rate of interest, which have actually harmed fintech multiples throughout the marketplace.

Nevertheless, our company believe that the business has actually formally turned a corner, and now stands to create enhancing monetary outcomes as an effect of its ongoing company execution and item shipping speed.

Well placed in its market, and with various drivers set to introduce in the coming months, we anticipate that if interest in the stock gets re-ignited, then financiers might see some severe benefit in future quarters.

Today, we’re having a look at where things stand with the business, and how approaching drivers might send out the stock skyrocketing with a brand-new core story concentrated on the business’s combined item offering.

Sound excellent? Let’s leap in.

Where Things Stand

While Robinhood has a great deal of luggage in the minds of the public due to the previously mentioned debate around GameStop (which has actually been just recently re-enforced by the release of “ Dumb Cash“, a motion picture about the occasions of January 2021), management has actually mainly avoided the business’s abject track record and bad stock cost efficiency from affecting company execution.

Given that the business’s IPO, there has actually been development on numerous fronts.

First Of All, HOOD is less dependent on deal incomes than ever in the past.

In the duration right before Robinhood’s IPO, almost 6% of all incomes were from Dogecoin ( DOGE-USD) trading:

For the 3 months ended March 31, 2021, 17% of our overall profits was originated from transaction-based incomes made from cryptocurrency deals, compared to 4% for the 3 months year ended December 31, 2020. While we presently support a portfolio of 7 cryptocurrencies for trading, for the 3 months ended March 31, 2021, 34% of our cryptocurrency transaction-based profits was attributable to deals in Dogecoin.

In addition, a lion’s share of overall profits was originated from PFOF, or “Payment for Order Circulation”, a questionable practice where Robinhood offers orders to market markets and pockets a refund:

S-1

As a side note; in theory this does not trigger an even worse cost effect for clients, however that has actually been contested

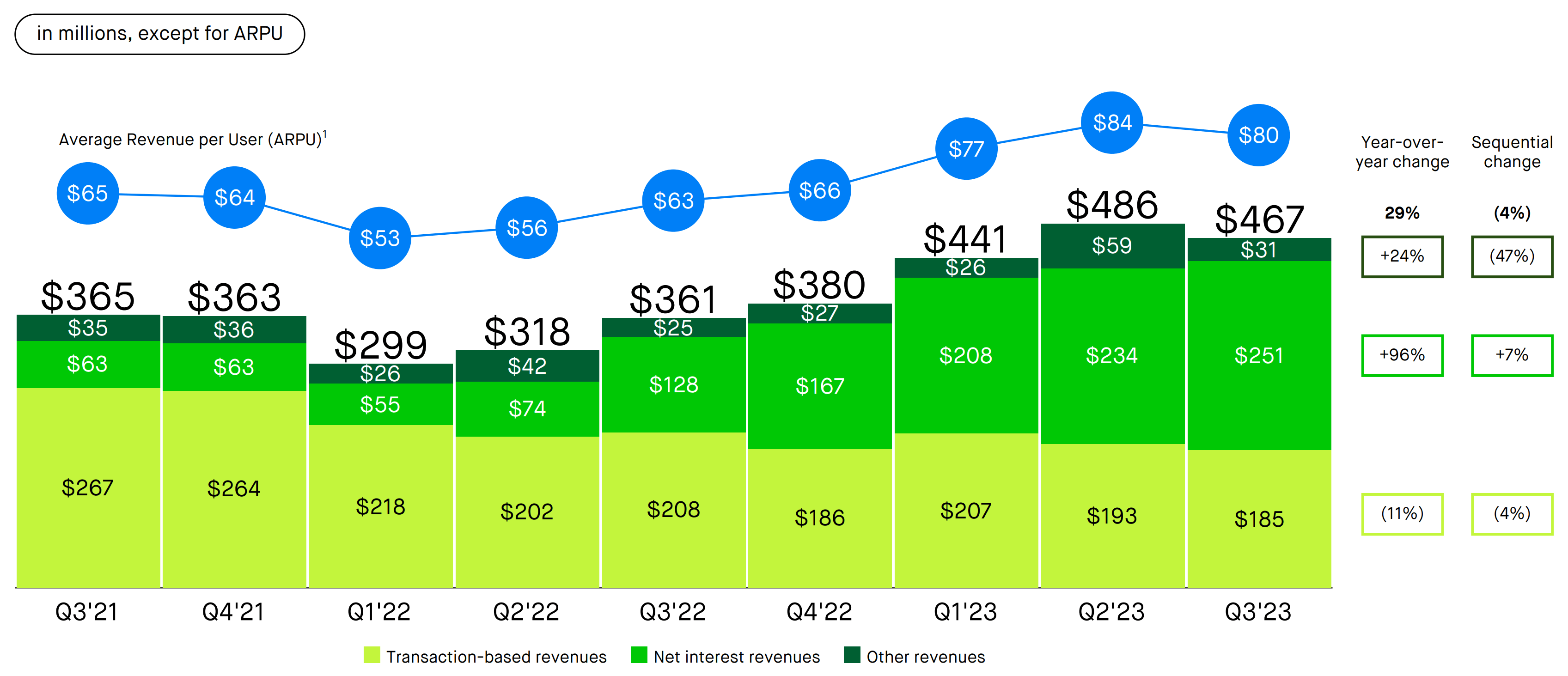

Total though, deal profits comprised completely 75% of profits in 2020 for Robinhood. This is an extremely cyclical company, and when the trading boom collapsed in 2022, so did HOOD’s stock cost.

Nevertheless, that has actually altered in current quarters, and in Q3, HOOD reported that less than 40% of incomes were transaction-based:

Revenues Discussion

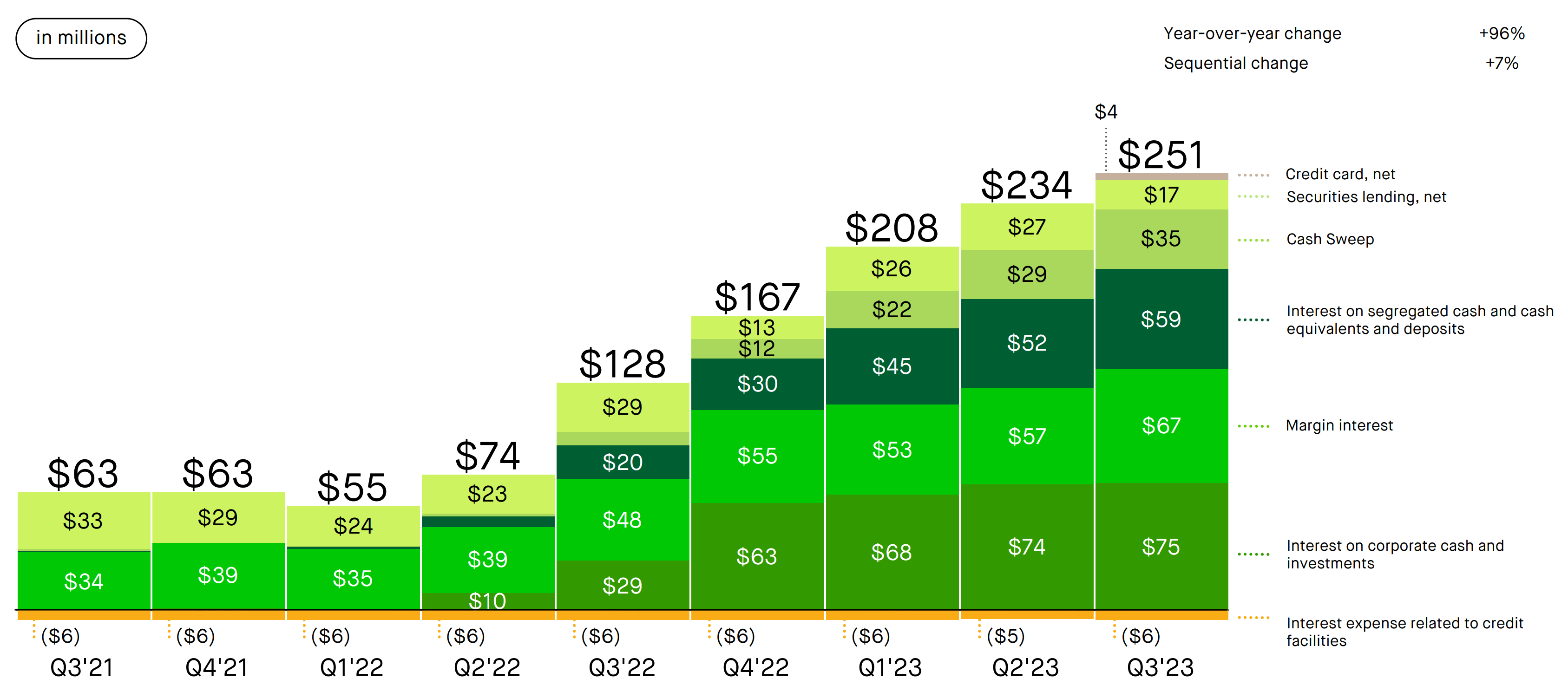

This is an outcome of enhancing interest incomes, which have actually been driven by greater rates, affecting business money interest, sweep incomes, and segregated money that HOOD makes a spread on:

Revenues Discussion

While rates aren’t anticipated to remain high permanently, as we have actually talked about here and here, Vlad Tenev, Robinhood’s CEO, has actually revealed that to some degree business is self-hedging:

Among the great aspects of our company is that it’s naturally hedged for modifications in rate of interest. Trading incomes and interest earnings tend to relocate opposite instructions. So we believe we’re quite well placed to carry out economically no matter the rate environment.

We have actually seen this play out over the last couple of years. In the lower rate environment, trading incomes were strong. However with rates moving greater, trading profits eased off some, however interest earnings has actually gotten.

This stays to be seen throughout longer cycles, however the vibrant here resembles the one we have actually talked about in Coinbase ( COIN).

As Coinbase has actually diversified its profits streams, it has actually enhanced its company by leaps and bounds while likewise placing itself for substantial gains in the next prospective crypto booming market.

Likewise, as brokerage deal profits has actually dried up, HOOD has actually continued performing, diversifying its profits sources and growing market share by releasing and enhancing its item suite.

No longer is Robinhood just an app you can utilize to trade stocks; it’s an all-in-one platform with a costs, conserving, and retirement offering, all looped with a synergistic subscription membership program called “Robinhood Gold”.

When integrated with strong current changed success and a GAAP earnings in Q2, things seem trending in the ideal instructions.

Future Drivers

As Robinhood launches brand-new items and enhancements, Gold’s worth proposal just looks more powerful, which must serve to more boost profits variety, which is what must drive long term operating take advantage of – as 90% of HOOD’s expense base stays set.

Therefore, brand-new item launches must even more boost the environment and the Gold offering particularly.

However what is Robinhood ready to introduce?

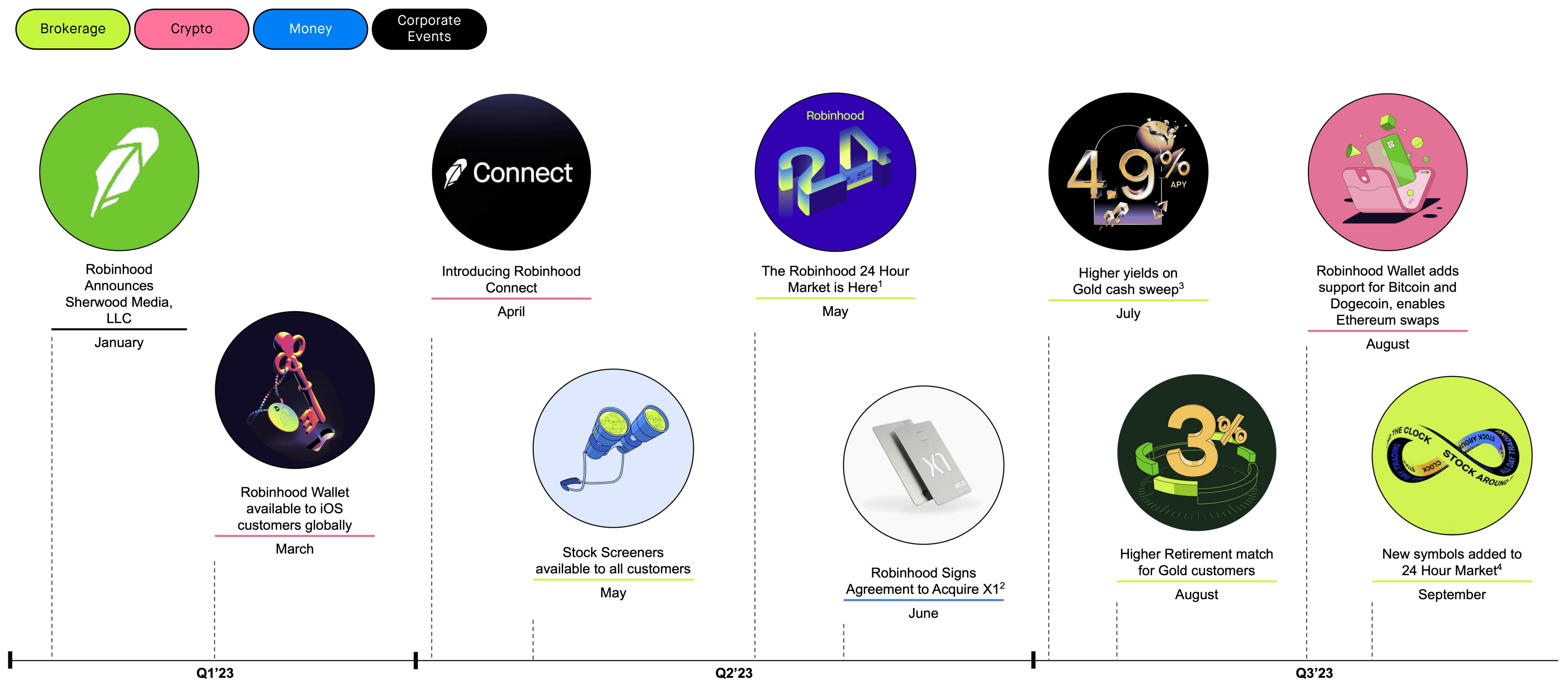

First Off, Robinhood is set to introduce its equity offering in the UK. This would mark the very first worldwide growth by the business, which is amazing.

This is necessary for a couple of crucial factors. Initially, worldwide retail brokerage has actually not seen the pressure that U.S. brokerage has. Competitors must be light, particularly for equity trading, as a big part of foreign trading is done by means of CFD, not physical settlement.

2nd, getting Robinhood’s feet damp is crucial to releasing in increasingly more jurisdictions in the future. This is twice as real as the CEO has actually preserved that introducing is not a technical concern, however just a regulative one:

So I did discuss that equities trading, in specific, 24-hour market will be readily available at launch. In regards to the other worth props, once again, would rather not run ahead of the statement, like we’ll learn soon. The advantages of doing our worldwide growth naturally is we can take advantage of the very same platform. That’s why Robinhood 24 hr Market is readily available at launch. It’s all on the very same platform. So there’s truly no technical restriction to making our services readily available anywhere that we run. It’s all simply a matter of licensure and ensuring that we have the proper licenses for all the various items we provide. And I believe you’re truly going to begin to see the natural technique paying dividends as we continue to broaden throughout numerous jurisdictions, and we include things here in the United States and we include– we link to various market centers overseas. You’ll see that the worth accumulate both to our United States clients and the clients in brand-new jurisdictions.

This is necessary, as it indicates that the worldwide company might end up being a big part of HOOD’s overall profits in the future. Structure with this modularity must result in faster-than-expected launches moving forward.

In addition to the UK launch, HOOD is likewise releasing its Crypto offering in the EU. This is another chance to improve the worldwide technique with a reasonably low quantity of danger to the core U.S. company.

2nd, Robinhood will be releasing a Charge card offering in the coming months.

The offering is stated to be constructed into Robinhood Gold, which enhances the moat around subscription.

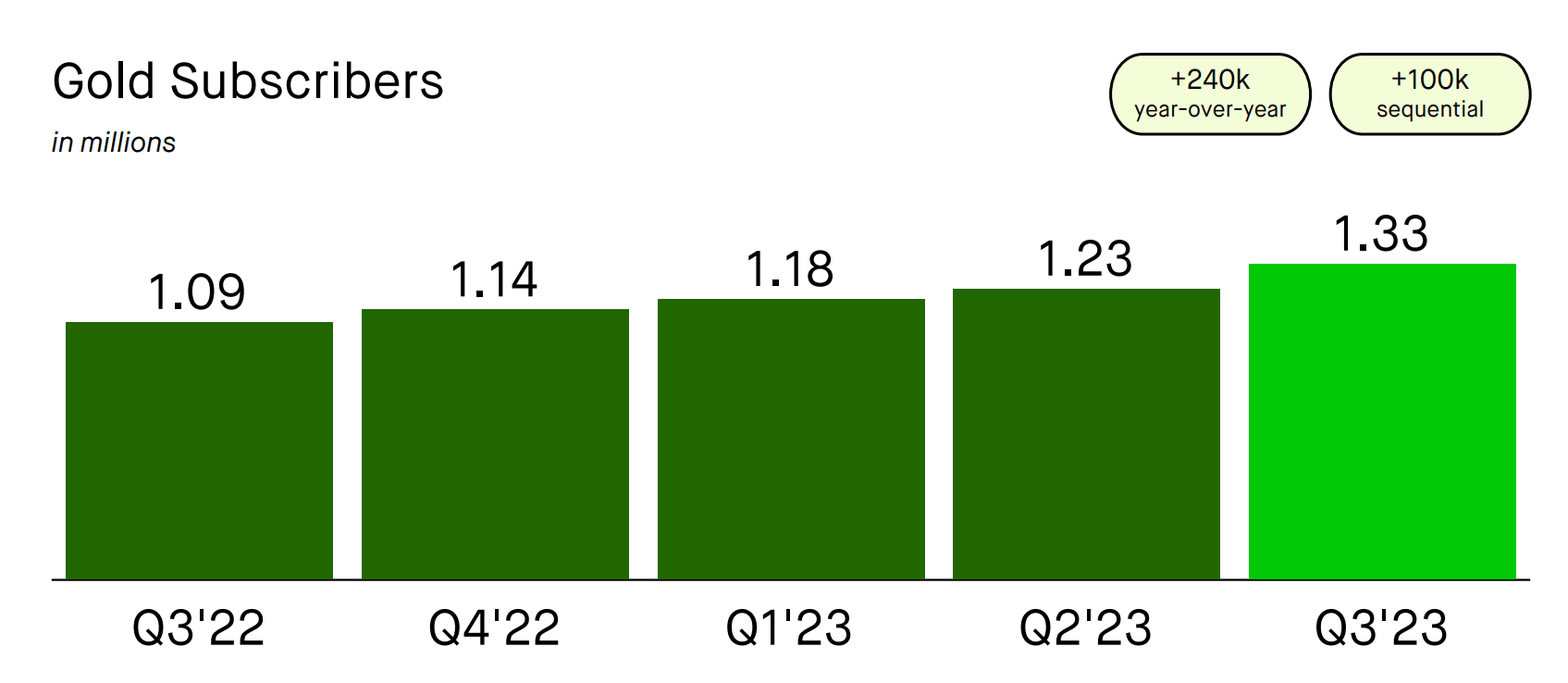

This must develop gold momentum, which has actually been extremely strong since late, up 22% YoY:

Revenues Discussion

Here’s some more information about the charge card offering, direct from the CEO:

We in fact simply examined and authorized the last styles for what’s going to end up being the Robinhood charge card recently, so we have actually been making great development. The group is incredibly inspired to introduce it. And we do prepare for there will be a duration of knowing. Naturally, X1 has actually had some information from their consumer base. However we prepare for when we launch this brand-new item, the scale of Robinhood’s consumer base is much larger.

…

After obtaining X1 in July, our group has actually been hard at work, producing a remarkable charge card and we have actually got something unique prepared for Gold clients.

As HOOD continues to expand its item offering, it starts to look increasingly more like a one stop store. As the platform integrates in size and scope, there are increasingly more chances for HOOD to monetize its userbase, which must result in long term leading line development.

Lastly, Robinhood is wanting to introduce futures in 2024. The CEO just recently pointed out that he believes this has the prospective to be a 9-figure profits company, which would be a major benefit to HOOD’s present monetary circumstance:

Let me now discuss futures. We’re getting closer to revealing our offering there. And we have actually been hard at work, constructing what our company believe is the best-designed futures item, especially on mobile. Rivals create numerous countless yearly profits from futures trading. So as we continue to carry out, our company believe we have a genuine chance to broaden the marketplace, take market share, and develop a nine-figure profits company in time.

In addition to the effect of a brand-new profits stream, this must likewise assist HOOD capture share.

Today, our company believe Robinhood is still seen by expert traders as a rather unsophisticated platform that can’t take on more completely included software application, like NinjaTrader, TradingView, or Sterling. Nevertheless, if HOOD has the ability to develop out a strong, vertically incorporated, commission-free futures offering, then it will seriously assist HOOD’s objective of developing their advanced trading offerings, which must drive loads more profits:

Speaking about our active trader offerings, as I pointed out previously, our objective is to be the top platform for active traders and we have actually been getting share. And for the last 3 quarters sequentially, we have actually seen our market share of alternatives and equity deals continue to increase.

A well considered futures offering must enhance monetary outcomes considerably.

All in all, these item launches might result in brand-new interest in the business from both clients and financiers, which might result in more powerful monetary outcomes, along with an enhanced numerous.

The Appraisal

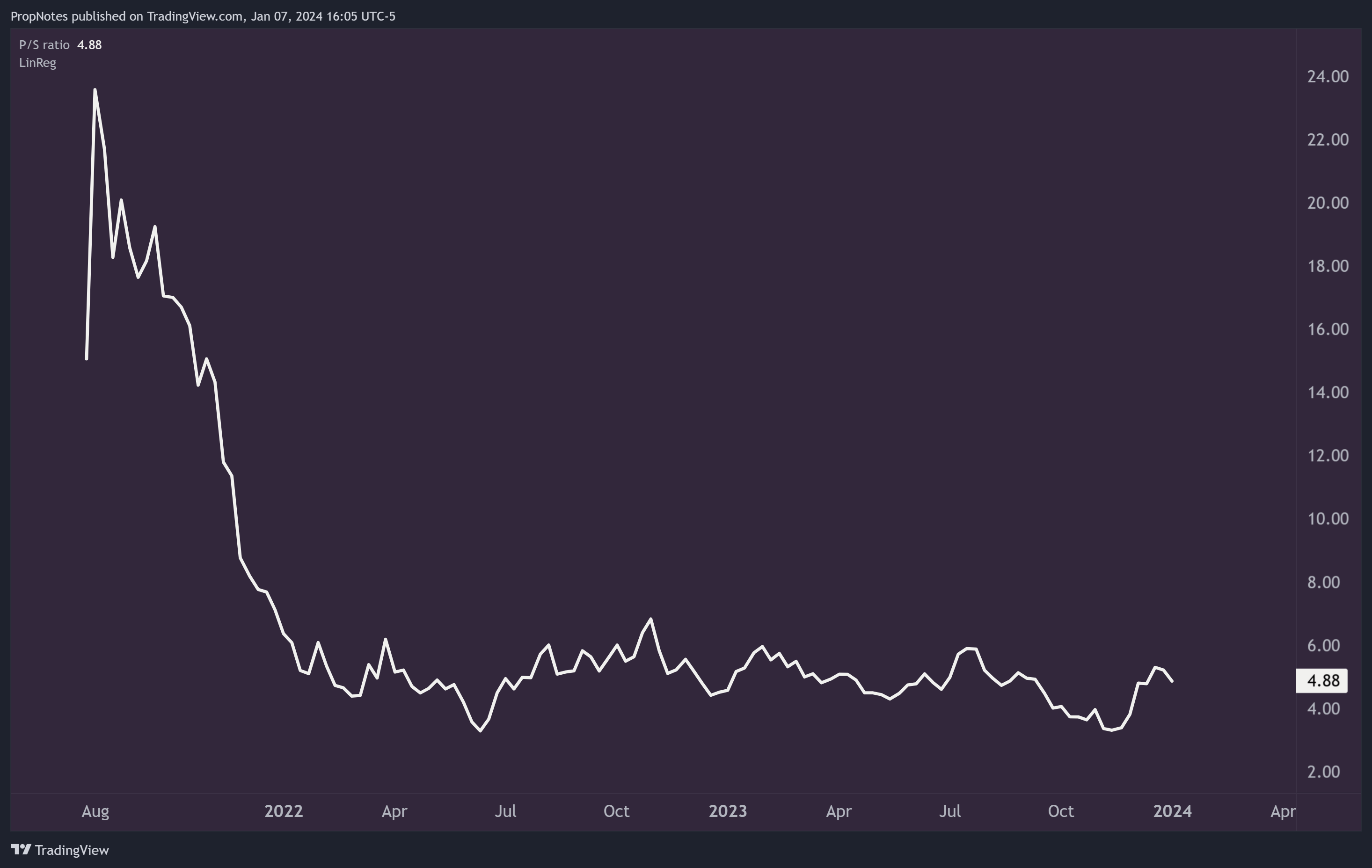

Considered That all of these item launches are anticipated to come in the very first couple of months of 2024, it appears that the stock might be underestimated:

TradingView

Trading at just 4.8 x profits, the stock is trading at the low end of its historic numerous, and listed below other high-growth stocks that are likewise turning the corner on success, like Nubank ( NU).

As we anticipate the worldwide growth, the charge card, and the futures item launches will create considerable brand-new company for HOOD (on the business’s reasonably set expense base), it appears as however genuine, continual favorable GAAP earnings is on the table considered that the business is currently primarily breakeven.

Integrated with the deal company and subsequent diversity story that has actually been playing out, the setup in HOOD today advises us of COIN, which has actually had rather the run given that we called it out in 2015.

In our view, HOOD might see its numerous double to ~ 10x, out of the appraisal trough it presently discovers itself in, and closer to other high development, brokerage/like peers like COIN.

If the stock winds up re-rating greater, when integrated with some leading line development as an outcome of ongoing item execution, then it’s possible that shares might double to ~$ 23 by 2025.

Dangers

There are some threats when it pertains to purchasing HOOD.

The top danger to be knowledgeable about is around HOOD’s deal company. if PFOF is ruled unlawful or managed out of presence by the SEC (or any other market regulative firms), then HOOD might lose a huge portion of company. There was some chatter about this a while back, however it’s waned for the time being.

That stated, there is still severe heading danger there.

Other threats to be knowledgeable about consist of the reality that our thesis here is rather speculative in nature. HOOD might stop working to introduce these items, or they might stop working to create considerable leading line development that would eventually assist in a better leading line multiple.

Nevertheless, if you take a look at HOOD’s execution performance history, we have every belief that the business will have the ability to satisfy its item objectives in 2024, provided how well it has actually performed traditionally:

Financier Discussion

Aside From that, the story has actually been considerably de-risked given that the GME mess. Robinhood has more than $5 billion in business money on the balance sheet, which must strengthen the business from a lot of other threats.

Summary

Eventually, while there are some threats in play, particularly around PFOF as a service practice, HOOD has actually done a terrific task constructing its app into a one stop buy costs, investing, conserving, and retiring.

With every brand-new item release, HOOD’s ‘gold’ membership offering gets more powerful, and as the business seeks to deepen, broaden, and generate income from each user relationship, we believe the future looks brilliant.

Offered the presently depressed appraisal, now is the time to purchase some stock before the marketplace completely recognizes the effect of the business’s future item launches and leading line profits capacity.

If all goes according to strategy, we believe that shares might double by 2025.

Cheers!