adventtr/iStock by means of Getty Images

I last discussed Schrodinger, Inc. ( NASDAQ: SDGR) in July; I ranked them a hold, stating I was waiting to purchase this AI winner. The stock consequently fell from $47 to a November low of $20.80; it was a excellent choice, preventing a fall of 56%. In this short article, I will provide my view of SDGR’s efficiency for 2023 and reevaluate my hold ranking.

Simply put, I believe SDGR has actually lost momentum relative to its peer group, its share cost is no longer leading the pack, and all 4 earnings streams appear to be under pressure. Its essential consumer has actually drawn back from some partnerships, expenses are increasing, Wall Street experts have actually minimized their cost targets, and the Looking for Alpha quant system has actually moved from Buy to Hold.

For pre-profit business to preserve share cost momentum, they require favorable news; SDGR has actually fallen back its peer group in this location.

Peer Group Efficiency

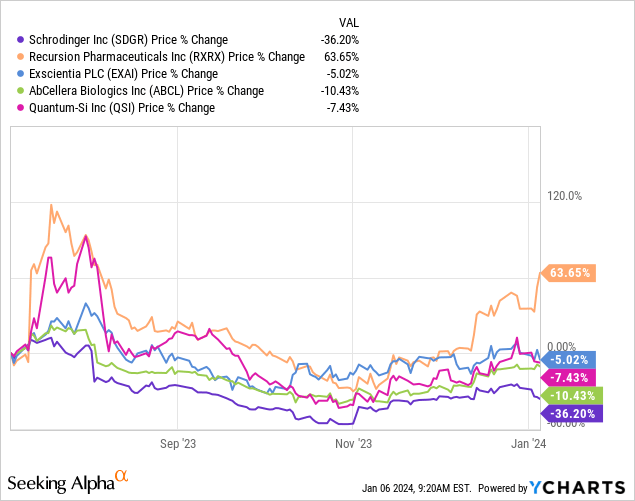

The 4 business I think about SDGR’s peer group discovered a rate low in early November and have actually moved higher ever since. SDGR depends on $31 at the time of composing. With a prospective bottom in location for this group of business, it might be a great time to buy among them; they are all pre-profit, so they must all be thought about high-risk financial investments.

At the time of my very first short article, the SDGR share cost carried out substantially much better than the rest. In truth, in the 12 months before the short article, it was the only one revealing a favorable return up 58%; the next finest was Recursion Pharmaceuticals ( RXRX) at -10%. Because that short article, the space in between them has actually closed, and SDGR is no longer the front-runner, it is now in last location.

2023 News SDGR might be delayed

One location I keep an eye on and gather information from is journalism launches released by business; in these pre-profit business, info from news release can offer a stock momentum. With no favorable news, the shares frequently lose their momentum.

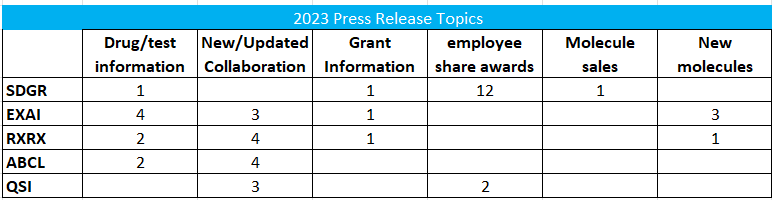

Temptation grants to existing and brand-new workers control SDGR’s news release; they have actually offered couple of updates on drug development or brand-new partnerships. The following table is a tally of news release from each business. It does not consist of several news release associating with the exact same information.

Tally of Press Releases (Author)

Obviously, this might be a bad press department or a reflection of SDGR’s penetration of the drug business market, however it contributes to my basic view of a loss of momentum in 2023.

Income Prospective

All business should ultimately earn a profit to make it through, which should originate from earnings generation. SDGR has 4 earnings funnels, all of which are a cause for issue.

The Exclusive Drug Pipeline

The prospective to make revenues here is massive. If they can get a brand-new drug authorized, then their earnings might be off the charts. Development in Drug advancement is constantly sluggish; it needs to go through a minimum of 4 screening stages. Pre-clinical is required to get FDA approval to start screening; a Stage 1 test on healthy people guarantees the drug is safe. Stage 2 screening is a fairly small test of the drug’s capability to treat its targeted condition effectively. Stage 3 is a massive test to gather adequate information for an application to license the drug. Generally, it takes in between 10 and 15 years in the cancer field targeted by SDGR.

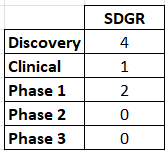

Proprietary Drug Pipeline (December 2023):

Drug Pipeline (Author from SDGR)

The programs in Stage 1 would not seem distinct drugs. Among them, SGR-1505, is a MALT1 inhibitor, and the FY 2022 page 73 stated.

with regard to SGR-1505, our MALT1 inhibitor, which we are advancing for the treatment of clients with fallen back or refractory B-cell lymphomas, we understand numerous MALT1 inhibitors in scientific advancement, consisting of by Janssen Research study and Advancement, LLC, a Johnson & & Johnson business, Ono Pharmaceutical Co., Ltd., AbbVie Inc. and Zentalis Pharmaceuticals.

Competitors is constantly a problem, and with these drugs, SDGR does not have a distinct idea; they might not get to market initially, might not have the very best drug, and will deal with problem taking on these substantial pharmaceutical business.

Even if the drug shows reliable and safe, it might not create adequate earnings to cover the research study expenses being raked into it.

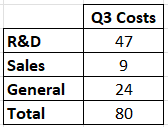

I do not anticipate any earnings from this pipeline in the next 10 years; nevertheless, it is expensive to perform this work. SGDR does not report the R&D expenses of each earnings section independently; nevertheless, the Q3 2023 profits report revealed a considerable boost in R&D costs. For the very first 9 months of 2023, it increased to $130 million from $92 million over the 2022 comparable duration. The CFO stated in the profits report.

A considerable part of this boost is because of redeployment of our existing workers from partnerships to exclusive programs and from consumer dealing with structural biology services to internal programs.

The result is that the exclusive drug pipeline is increasing expenses for SDGR. The drugs will likely deal with competitors if authorized, and the prospective earnings is most likely more than 10 years away.

Collective drug discovery

SDGR has numerous contracts with pharmaceutical business where they collectively research study potential drugs. SDGR can get turning point payments for this work as the drug prospect overcomes the regulative system and will get a share of future sales. It is a lower threat as the expenses are shared, and it implies that if the drug is authorized, a significant pharmaceutical business will offer it instead of SDGR requiring to.

Bristol Myers Squibb ( BMY) is SDGR’s main partner, and last quarter, they canceled the deal with 2 of the programs the CEO stated i n Q3 profits (he utilized BMS not the ticker)

Today, we reported that rights to 2 associated oncology discovery programs within the BMS cooperation went back to us after BMS chosen not to continue with additional advancement for tactical factors.

The SDGR personnel included with the research study have actually gone back to SDGR, and the business is evaluating what to do with the 2 programs. They might include them to the exclusive list or look for another partner. I see this as rather an unfavorable; BMS will not have actually taken the choice gently, and it needs to show their view of the programs.

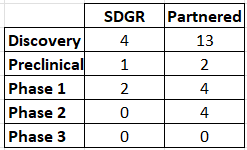

The BMS cooperation has 3 active research study programs (down 40% this year) and one discovery particle. The less active research study programs will decrease future turning point payments, representing 32% of SDGR’s earnings. (Q3 2023 10Q p10 drug discovery earnings) Drug Discovery’s gross margin was 13% for the quarter, so it is assisting to cover R&D expenditures in the exclusive location.

Drug programs (Author)

The collective screening program covers 3 times as lots of particles as the exclusive one, which should increase the possibility of discovering an effective drug. SDGR gets cash for these programs at a favorable gross margin in real dollars; it was $1.7 million in Q3 2023. It would take a huge boost in this location to have any genuine influence on SDGR’s financial resources.

I still can not see any earnings from sales of drugs in this pipeline this years; the 4 stage 2 partnered programs are better to market than the exclusive pipeline however will likely not be authorized up until the 2030s.

Sales of Software Application

The software application platform established by SDGR is its primary possession; the software application utilizes AI, physics, chemistry, and medical understanding to assist scientists establish brand-new substances that might have healing results. The platform is amazing, and its functions are continuously being updated. It is moving the drug market along faster than ever previously. I am persuaded it will result in groundbreaking drug discoveries to treat illness and aid clients without any offered treatment. I do not believe anybody can check out this platform and not be impressed with it. I think all of mankind would benefit if SDGR was successful.

My concern is not the item however the revenue. I composed in my very first short article that the platform currently had enormous market penetration; all of the leading 20 Pharmaceutical business utilized it, and at the end of 2022, they had 1,748 active clients. Growing the earnings here will have to do with increasing the quantity clients invest instead of getting brand-new clients, as really couple of are left.

The short-term potential customers here require explanation. Experts attempted to focus on this concern in the Q and An area of the Q3 profits call. Michael Ryskin of Bank of America stated in his concern that he had actually been notified that lots of pharma business were starting reorganizations, refocusing advancement programs, and cost-cutting. He asked how that was opting for SDGR. The CEO stated they had actually not yet been impacted however knew these conversations. He repeated the assistance for Q4 however steadfastly declined to be made use of any assistance for 2024, despite the fact that he was pushed numerous times.

The software application organization is important to SDGR; it supplies continuous, trustworthy, high-margin earnings. In Q3, this section provided $29 million in earnings at a gross margin of 76%. It is a terrific organization however too little to cover operating expense.

Q3 expenses (Author Database)

Management assisted a boost of sales in between 15% and 18% from 2022 to 2023. Even if this development rate continues, it will be several years before these expenses are covered.

Equity Investments

SDGR has actually made substantial equity financial investments in little and early-stage business that utilize its software application. The capital development on these equity positions and cash gotten from them can represent a considerable source of revenue or loss. In 2023, SDGR got $147 million ( max) from the disposal of a substance by among the business it has actually purchased Nimbus Rehabs. That is a considerable quantity of cash, which I went over in my very first short article. SDGR has numerous financial investments in business that might establish comparable outcomes. It is challenging to evaluate the most likely earnings from these financial investments. Additional offers like the Nimbus one might be struck, and it is not uncommon for big Pharma business to purchase the pipelines of smaller sized rivals.

Obviously, as these business’ share costs go up and down, it impacts the SDGR results.

In the Q3 profits call, the CFO stated.

Our other earnings was when again impacted by substantial modifications in the worth of our equity positions in openly traded biopharma business. Modifications in these appraisals led to a $14.5 million loss in Q3

Equity financial investments grew from $26 million in Q3 2022 to $92 million by Q3 2023, looking like long-lasting properties on the balance sheet. The other substantial part of long-lasting properties is rights of usage properties, running leases at $120 million.

The concentration of earnings for SDGR is high (Q3 10K Page 12). The 2 biggest clients represent 55% of overall agreement properties, a boost from 40% in 2022, and one consumer represented 29% of overall earnings.

It promises that BMS is among these 2 substantial clients, and earnings here might reduce with the return of 2 jobs.

If the experts asking concerns in the profits call are right and pharmaceuticals are wanting to cut expenses, it might impact SDGR earnings in all 4 of these revenue-generating locations.

SDGR Targets and Projections

I have actually currently stated that momentum has actually been lost, and there is some contract with this view in the market.

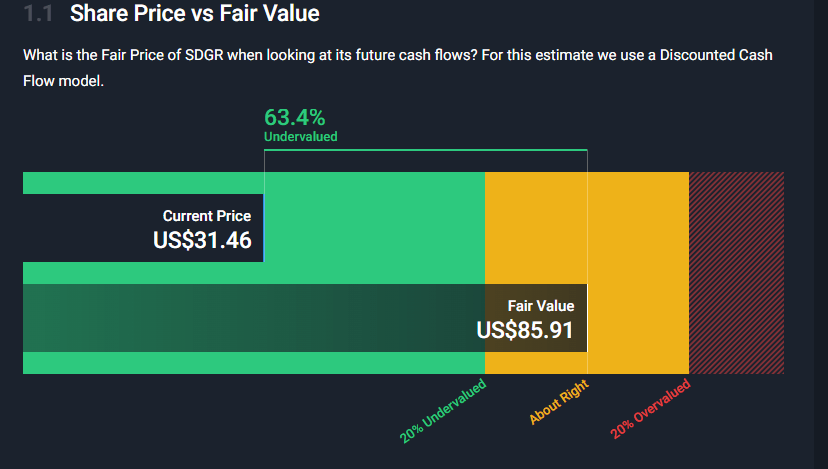

The Looking for Alpha Quant ranking dropped from Purchase to Hold at the start of November. The Simplywall.st reasonable worth computation I provided in my very first short article has actually fallen from $97.50 to $85.91

DCF reasonable worth (Simplywall.st)

Wall Street experts typical cost target reduced in October and November. Initially to $54 and after that to $44, one Expert now has a target cost of $29 listed below the existing worth. When I composed my very first short article, Wall Street had a target of $56, which was down 21% over the duration.

Income targets

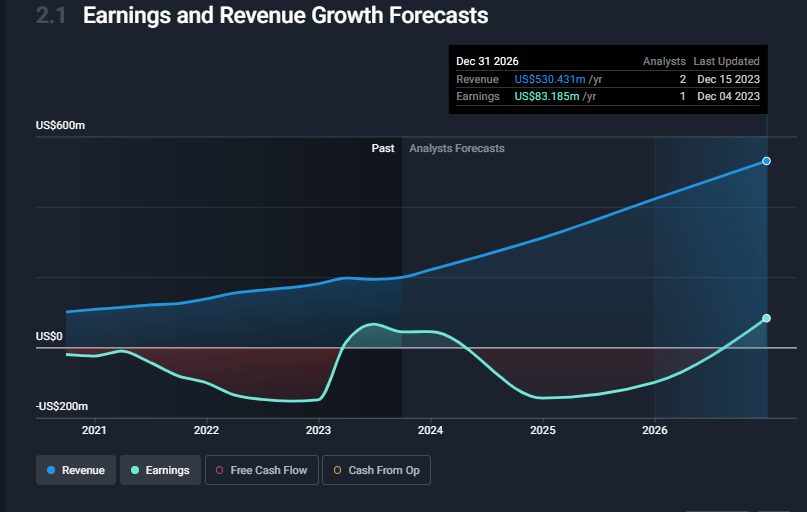

The experts that provide earnings targets for SDGR (7 offer targets for earnings 2026 and 2 for 2027) have actually not altered their view substantially considering that my very first short article; this would appear at chances with whatever else I have actually provided.

I anticipate earnings projections to be combined back in the coming weeks/months and the resulting breakeven date to wander. This will undoubtedly put a drag on the SDGR share cost.

Unchanged Income Projection (simplywall.st)

Financials

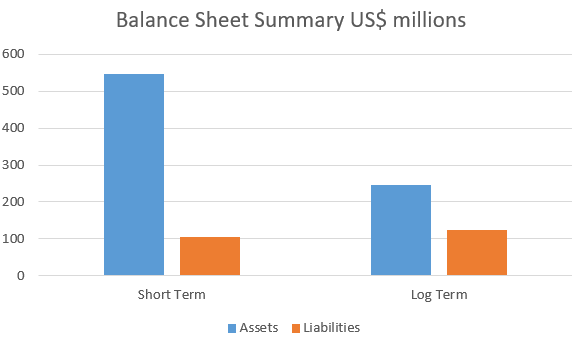

The SDGR balance sheet stays perfect; they have no financial obligation and ended up Q3 with $249 million in money.

SDGR balance sheet (Author Database)

The following chart is from Simplywall.st and demonstrates how SDGR makes and invests its cash. It is on a tracking 12-month basis.

Income generation and expenses (simplywall.st)

Wall Street’s very first year of favorable profits projection is 2027, recommending they have simply adequate money. Nevertheless, if I am ideal and these projections of break even and earnings drift by simply one year, things will not look as perfect, and the share cost will come under more pressure as a capital raise begins to come into view.

Conclusion

In my viewpoint, SDGR has actually had a bad year relative to its peer group; the potential customers for earnings seem dropping as the pharmaceutical business re-prioritize their research study and go through cost-cutting workouts.

The exclusive drug pipeline does not appear distinct, has a high expense, and is several years from earnings generation.

Bristol Myers Squibb returned 2 drug prospects, which may be the very first indication of pharmaceutical business cutting expenses in a manner that impacts SDGR.

The software application organization has nearly totally permeated the prospective consumer base, and development will need increased consumer costs. SDGR decreased to offer assistance for this in 2024, which contributes to my issue.

I preserve my hold ranking however have actually transferred to an unfavorable outlook and am no longer wanting to purchase into this story.