Wasan Tita

Welcome to another installation of our BDC Market Weekly Evaluation, where we go over market activity in business Advancement Business (” BDC”) sector from both the bottom-up – highlighting specific news and occasions – along with the top-down – supplying a summary of the wider market.

We likewise attempt to include some historic context along with appropriate styles that seem driving the marketplace or that financiers should bear in mind. This upgrade covers the duration through the 2nd week of November.

Market Action

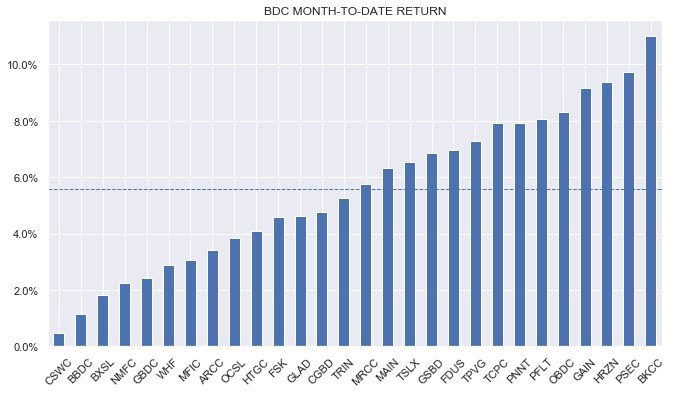

BDCs were flat on the week as markets combined after a sharp run-up over the previous number of weeks. Month-to-date, all BDCs in our protection remain in the green.

Organized Earnings

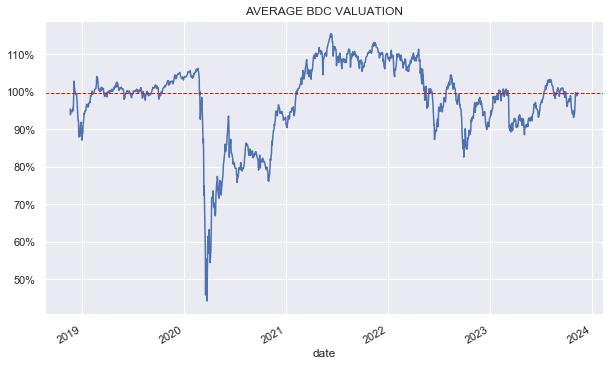

Appraisals stay near 100% after briefly dipping towards the low 90s location – when we handled to squeeze in an upsize to our BDC position. BDC revenues have actually been can be found in extremely strong so this is most likely to support the sector over the coming weeks.

Organized Earnings

Market Styles

MidCap Financial Financial Investment Corp. ( MFIC) revealed a merger arrangement with 2 Apollo loan CEFs ( AIF) and ( AFT). MFIC is a previous Apollo BDC (AINV) so there is a connection there. As a sweetener for the proposed merger, the 2 CEFs get an extra $0.25 (a bit less than 2% of NAV) on closing.

We do see numerous BDC mergers (FCRD, BKCC and so on) and CEF mergers (a lot of to count) nevertheless we do not see a great deal of BDC/ CEF mergers. On the face of it possibly we need to considering that BDCs hold “loans” as do “loan” CEFs like AIF and AFT.

Nevertheless, while both can hold loans, the loans themselves are extremely various in between the 2 kinds of cars. BDCs hold personal loans that they themselves usually work out with business that they tend to have a close relationship with. There are extremely couple of exceptions such as OCSL which likes to punt in the general public loan market however even there the size of its public loan position is extremely little.

CEFs, on the other hand, hold public i.e. bank loans that they obtain in the secondary market. Once again, there are a handful of exceptions such as the Barings CEFs which are actually more BDCs at heart than CEFs.

The 2 various kinds of loans have essential ripple effects. If MFIC gets the portfolios of AIF and AFT much of the worth of the BDC wrapper vanishes for those possessions. Public loans need to be marked-to-market – they have far more unstable evaluations than personal loans. This is why loan CEFs have much lower take advantage of levels than BDCs.

The capability of MFIC to “handle” its NAV as other BDCs do will likewise be substantially minimized. BDC are less at threat for a forced deleveraging than the lower-leveraged CEFs since of their capability to mark-to-model instead of mark-to-market. This, naturally, keeps BDC NAVs far more steady than loan CEF NAVs. A boost in public loans within the portfolio might trigger MFIC to call its take advantage of down in action to the greater volatility of its possessions, losing much of the BDC wrapper advantage.

2, MFIC will not have a relationship with the business whose loans it gets from the funds so there will be absolutely nothing for it to do to handle them (e.g. transform to PIK, provide management help and cross-selling chances and so on) if they degrade other than to offer them. Unlike in personal loaning, public loans are normally held by numerous financiers, making it extremely challenging to collaborate help to the customer.

So, what is going on? The most basic response here is that this appears to be a grab for possessions. MFIC trades listed below the NAV that makes it challenging to grow its possession base by means of at-the-market share sales and public offerings. Another essential advantage is charges. MFIC has a charge that’s two times that of the CEFs so, suddenly, you double your charges on the exact same possessions – magic!

Eventually, we believe MFIC will relax all of the AIF/AFT portfolios and rake the cash into brand-new personal loaning. This will permit it to grow its overall possession base above and beyond the possessions held by the 2 funds as MFIC runs at a greater level of take advantage of.

MFIC stated that the combined business will have higher scale and diversity – the scale point is reasonable enough nevertheless the diversity point is not apparent. MFIC and AIF have about the exact same variety of positions nevertheless the biggest MFIC positions are “chunkier”. Plus, since of its greater take advantage of, each position is a greater percentage of the NAV than in AIF. This is not to point out the 8% Air travel tradition portfolio. For an MFIC investor, there will be extra diversity nevertheless for an AIF investor there will probably be less diversity.

It stays to be seen whether the merger will close. As a holder of the CEFs, it’s not apparent that this merger makes good sense as it reduces the swimming pool of loan CEFs and supplies no assessment upside for the CEF holders offered the large MFIC discount rate.

Market Commentary

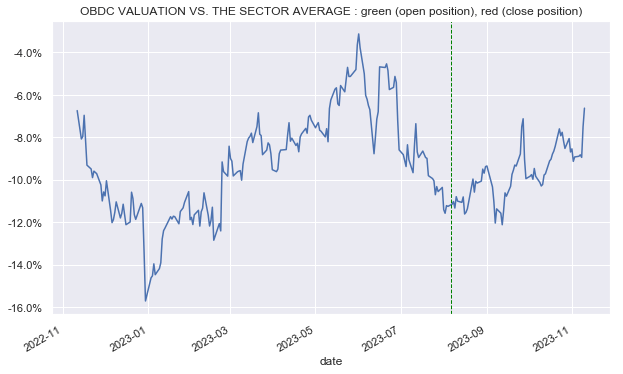

Blue Own Capital Corp ( OBDC) provided excellent outcomes with a 3.6% overall NAV return. Both net interest earnings and the NAV increased partially. Non-accruals stayed the exact same.

The stock stays appealing in the sector. In the previous year it has actually outshined the wider sector with a return double of the typical BDC nevertheless it continues to trade at a considerable discount rate to the sector.

This discount rate has actually continued to narrow considering that our preliminary allotment to the stock when it was trading at more than a 10% larger discount rate. This merging needs to continue over the medium term.

Organized Earnings

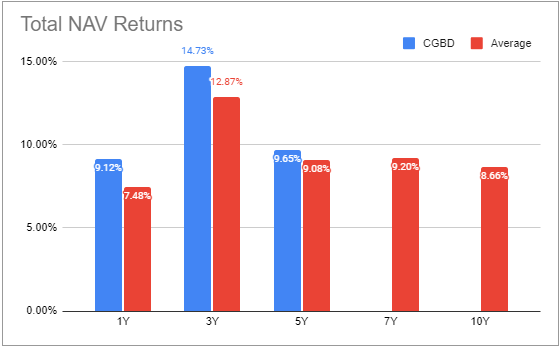

Carlyle Safe Loaning ( CGBD) reported excellent Q3 numbers for an overall NAV return of 3.5% over the quarter. Earnings was relatively flat – as net brand-new financial investments stayed unfavorable and a high level of floating-rate liabilities was a headwind. Non-accruals held constant.

In general, the business continues to do effectively however trades well listed below the sector typical assessment. If its outperformance continues we need to see ongoing enhancement in its assessment.

Organized Earnings BDC Tool