Weekly highlights

- Asia-US West Coast costs (FBX01 Weekly) increased 4% to $ 1,564/ FEU

- Asia-US East Coast costs ( FBX03 Weekly) climbed up 3% to $ 2,213/ FEU

- Asia-N. Europe costs( FBX11 Weekly) increased 8% to $ 1,056/ FEU

- Asia-Mediterranean costs( FBX13 Weekly) fell 2% to $ 1,370/ FEU

- China– N. America weekly costs reduced 2% to $ 4.73/ kg

- China– N. Europe weekly costs climbed up 11% to $ 4.30/ kg

- N. Europe– N. America weekly costs increased 4% to $ 1.78/ kg

Dive much deeper into freight information that matters

Remain in the understand in the now with immediate freight information reporting

Analysis

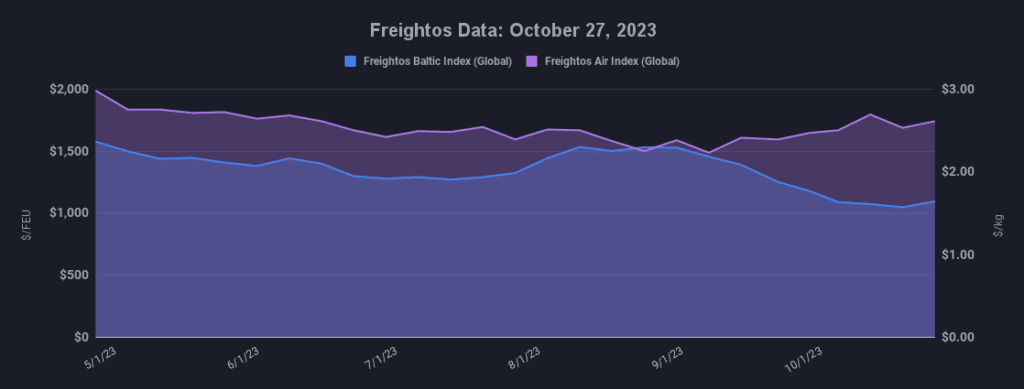

Transpacific ocean rates ticked up a little recently with costs level general given that early October. This relative stability reveals providers are having some success producing a brand-new rate flooring through capability decreases even as volumes ease and fleet sizes grow.

West Coast rates of $1,564/ FEU are 15% greater than 2019 levels while costs of $2,213/ FEU to the East Coast are 17% lower than in 2019. Also, West Coast rates stay 17% above mid-July, pre-peak season, levels while East Coast costs are now lower than in July, perhaps showing reports of some shift of volumes back to the West Coast now that labor problems there have actually been solved.

And however, up until now, low-water constraints in the Panama Canal have not appeared to effect container streams substantially, the Panama Canal Authority simply revealed that it will minimize everyday transits from 34– their level given that July– to 24 in November, 20 in January and down to simply 18 by February. This substantial decrease might increase the probability that more ex-Asia volumes will go to the West Coast or through the Suez Canal in the coming months.

Asia– N. Europe rates increased 8% recently and are simply 5% listed below 2019 levels however stay in loss making area as providers continue to have problem with overcapacity on the lane as shown in reports that providers will push prepared early-month GRIs to later on in November.

Providers are dealing with comparable problems on the transatlantic where some everyday rates dipped listed below $1K/FEU recently. Some providers revealed prepared GRIs for mid-November to press rates to $1,600/ FEU, however these boosts will just stick if liners can lastly bring capability to the level of need.

On the market level, overcapacity is approximated to peak next year, after which some providers anticipate the marketplace to cancel, while some experts anticipate the marketplace to be in some state of oversupply through 2028.

In air freight, there are indications that international volumes are increasing Freightos Air Index

China– N. America rates dipped by 2% recently, however at $4.73/ kg are 36% greater than in early August. Current increases in e-commerce volumes and substantially less guest flights than in 2019 are most likely adding to increasing rates. Asia– N. Europe costs increased 11% recently to $4.30/ kg, a 40% boost given that early September and their greatest level given that April.

Freight news takes a trip faster than freight

Get industry-leading insights in your inbox.