Robert Method

Back in July, I composed that JD.com ( NASDAQ: JD) was dealing with increased competitors which its service design was not as strong as some other Chinese e-commerce companies. With the stock down over -20% ever since, let’s capture on the name.

Business Profile

As a refresher, JD is among the biggest e-commerce business in China, where it runs as both a market along with an online seller. The business likewise owns some offline retail brand names consisting of JD Shopping center and the 7FRESH grocery store.

The business likewise owns a logistics and satisfaction network with over 1,500 storage facilities throughout China. The JD Logistics section likewise trades individually on the Hong Kong Exchange. The business is likewise associated with other endeavors, consisting of residential or commercial property advancement, health care, AI, and cloud computing.

Q2 Outcomes Fail To Excite Financiers

In my preliminary article, I kept in mind that Q2 was a huge quarter for Chinese online sellers, with the nation’s 618 shopping celebration falling in June. With the Chinese customer bewaring coming out of pandemic lockdowns, a variety of merchants consisting of JD presented big subsidiary programs to third-party merchants to get them on their platforms and to attract sales. For its part, JD presented a RMB10 billion ($ 1.4 billion) aid program.

The promos had actually the preferred effect on sales, with its JD retail system seeing income development of 5% to $34.9 billion. Electronic devices and house device sales blaze a trail with 11% development to $21.0 billion, while market income leapt 9% to $3.1 billion. General product sales were down -9% to $11.3 billion, harmed by its grocery store classification, which had actually benefited in 2015 from Covid-related lockdowns.

The business stated the variety of 3P merchants more than doubled year over year, which it has actually now seen 2 straight quarters of double-digit 3P development. It stated the majority of the development originated from marketing as more merchants assigned investing to the JD platform. The business has actually reduced platform service charge and take rates to assist attract brand-new merchants to its market.

Nevertheless, the boost in retail sales did not result in an enhancement in retail operating earnings, which was flat year over year at $1.12 billion.

Its JD Logistics section saw income grow 31% to $5.66 billion. Organic income was up 5%. On the other hand, running earnings for the section skyrocketed from $5 million to $70 million. The business stated external consumers represented 69% of the section’s income in the quarter.

In general, the business saw sales climb up 8% to $39.7 billion, topping the $38.5 billion agreement. Changed EPADS was available in at 74 cents, beating expert quotes by 6 cents.

Changed EBITDA increased 44% to $1. 4 billion. The business produced $6.1 billion in complimentary capital.

Gross margins was available in at 8.6%, and enhancement from 7.4% a year back.

On its Q2 incomes call, CEO Sandy Xu stated:

As the retail estate market and need of resilient items are still recuperating, the general house devices market has actually dealt with pressure. Nevertheless, JD’s house devices service meaningfully exceeded the market and continue to get market share. We associate this accomplishment to JD’s strong user mindshare and matched the shopping experience we supply and the qualified supply chain that we have actually been vigilantly constructed throughout the years. Additionally, our 3C classifications showcased a strong efficiency. This can be credited to our robust supply chain abilities, competitive rates and the deep user mindshare, remarkable shopping experience, consisting of benefit trade-in services and our active advancement in the O2O market. Especially, our sales of cellphones attained a double-digit development rate in Q2, exceeding the market level. It deserves highlighting that we have actually made substantial development in the advancement of an open platform community this year, with both merchant base and item supply broadening at a much faster rate. Development of 3P GMV has actually likewise sped up over the previous 2 quarters. Additionally, given that the start of the year, in spite of we have actually presented a series of supporting policies for our brand-new merchants, such as decreasing platform service charge and take rates, our 3P income development rate continued to surpass that of 1P in the very first 2 quarters, staying at double-digit variety.”

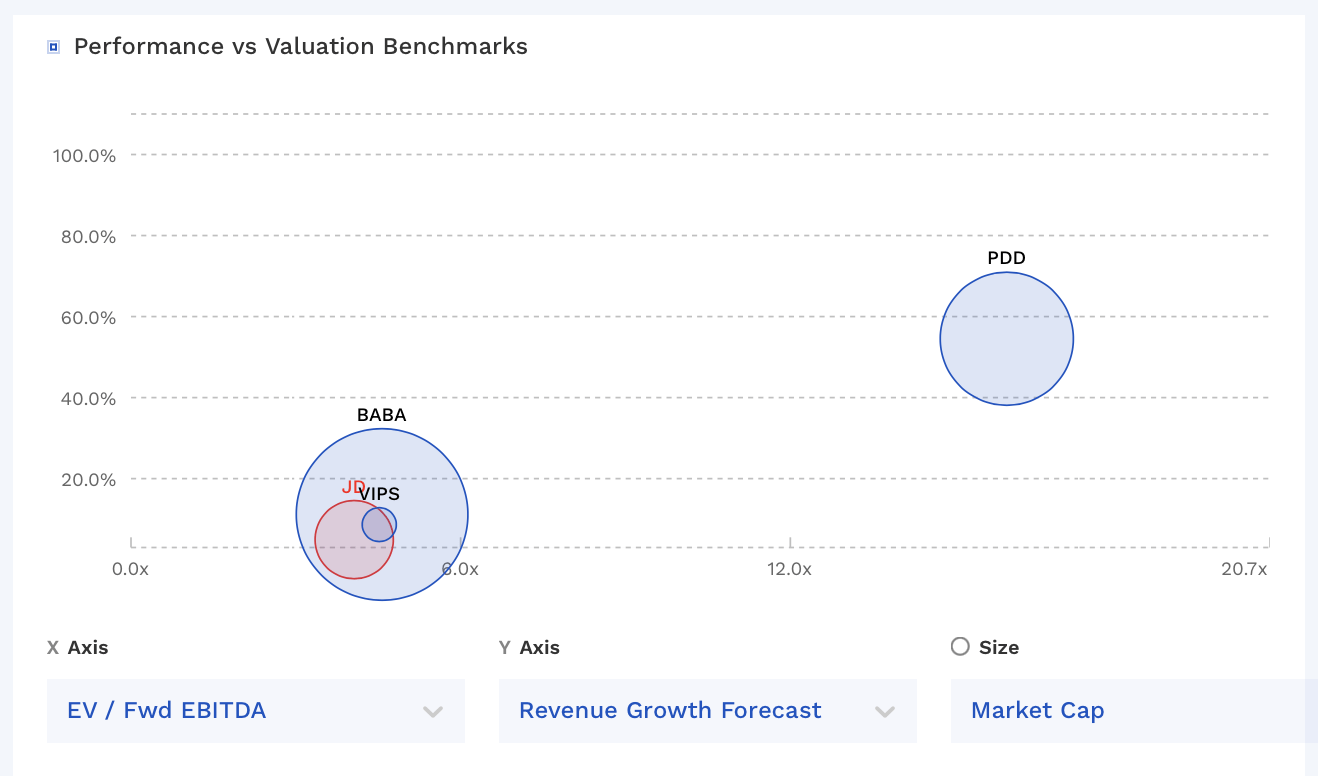

In general, JD published a good quarter in a difficult environment that saw a careful customer and a great deal of competitors seeking to complete on low costs. Nevertheless, its sales development tracked big rivals such as PDD Holdings ( PDD), which saw its Q2 income skyrocket 66% ( post here), and Alibaba ( BABA), which saw its retail income from Taobao and Tmall climb 12% in its June quarter. Vipshop ( VIPS), on the other hand, saw its Q2 income climb 14%. At the exact same time, JD needed to compromise margin to get its only 5% retail sale development, which caused no boost in running earnings for its retail section.

Where the business was strong, however, was with its Logistics system, which saw a rise in sales and success. The Logistics section is a little a gem, however simply much smaller sized than its Retail section. Not remarkably, while the business topped expectations, it still was inadequate to get financiers thrilled about the stock.

Evaluation

JD trades at 4.1 x the 2023 EBITDA of $5.75 billion and 3.5 x the 2024 EBITDA agreement of $6.79 billion.

On a PE basis, it trades at 10x EPS quotes of $2.93. Based upon the 2024 agreement for EPS of $3.42, it trades at 8.5 x.

It’s forecasted to grow income almost 5% in 2023 and 10% in 2024.

The stock trades at a comparable assessment to its Chinese e-commerce peers outside PDD, which is growing much faster than its peers.

JD Evaluation Vs Peers (FinBox)

Conclusion

Total, I continue to believe other Chinese e-commerce business are doing a much better task than JD and have more powerful service designs. The business is dealing with difficult competitive rates pressure, and its primary classification of electronic devices and home appliances has actually been pressed by careful customer costs in China.

That stated, I believe JD has actually gotten too inexpensive at this moment. The stock is affordable, as are its Chinese e-commerce peers, and it needs to take advantage of any healing with the Chinese customer. At the exact same time, its logistics system is strong and among the gems of the business.

As such, I’m going to update the stock to “Purchase.”

The most significant danger to the stock is that the Chinese customer stays weak which competitors continues to trigger additional rates pressure. The stock while affordable, presently does not have an instant driver, which might trigger the share cost to remain or perhaps simply continue to wander lower.