JHVEPhoto

Prologis, Inc. (NYSE:PLD) is a number one international logistics REIT excited about offering high quality commercial houses to consumers in key metropolitan distribution hubs.

Corporate presentation

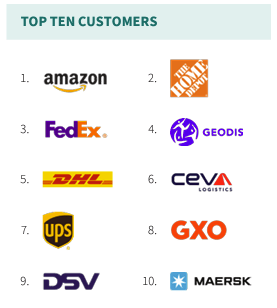

PLD’s expansive portfolio, spanning 19 nations, provides an excellent collection of logistics and distribution amenities that cater to a various set of tenants, together with notable e-commerce giants corresponding to Amazon (AMZN) and logistics suppliers corresponding to UPS (UPS), DHL and XPO Logistics (XPO). The highest buyer is Amazon.

Corporate Truth Sheet

This text will delve into PLD’ monetary efficiency, evaluation PLD’s strengths and weaknesses, establish attainable alternatives and threats, and supply an research of its valuation.

Monetary efficiency

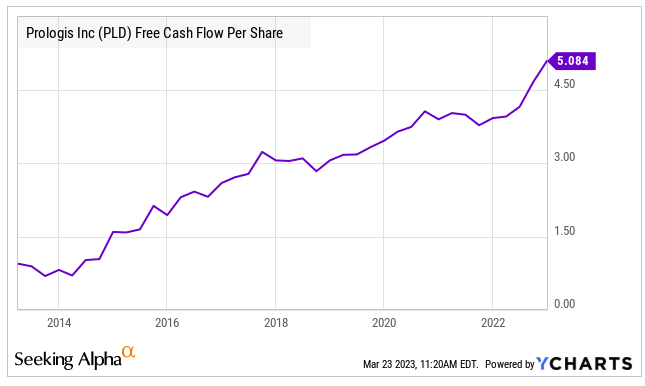

PLD has exhibited tough monetary efficiency, making the most of the sturdy tailwinds within the logistics and e-commerce sectors. Within the fourth quarter of 2022, PLD reported an excellent 98% occupancy charge, with its same-store money NOI rising at a wholesome 9.1%. Moreover, PLD’s loose money go with the flow according to proportion has demonstrated a gentle upward trajectory, pushed through its portfolio’s high quality property and strategic capital investments.

Ycharts

Strengths: Shoppers, strategic capital, and building pipeline

PLD stands proud as a pacesetter within the commercial actual property marketplace, with a large and geographically various portfolio of high quality logistics and distribution amenities.

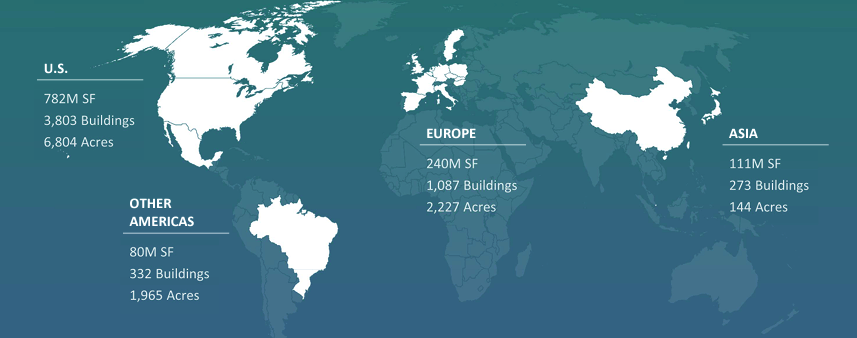

PLD has a wealthy historical past of making an investment in warehouses and is a key participant within the commercial actual property sector. With a limiteless international footprint that spans 19 nations, PLD holds a dominant place out there. In the USA by myself, it manages an excellent 570 million sq. toes of warehouse area, and globally, it manages over 1 billion sq. toes. As some of the peak landlords on this extremely sought-after actual property phase, PLD enjoys a management standing that provides it a vital aggressive benefit and lets in it to capitalize on enlargement alternatives.

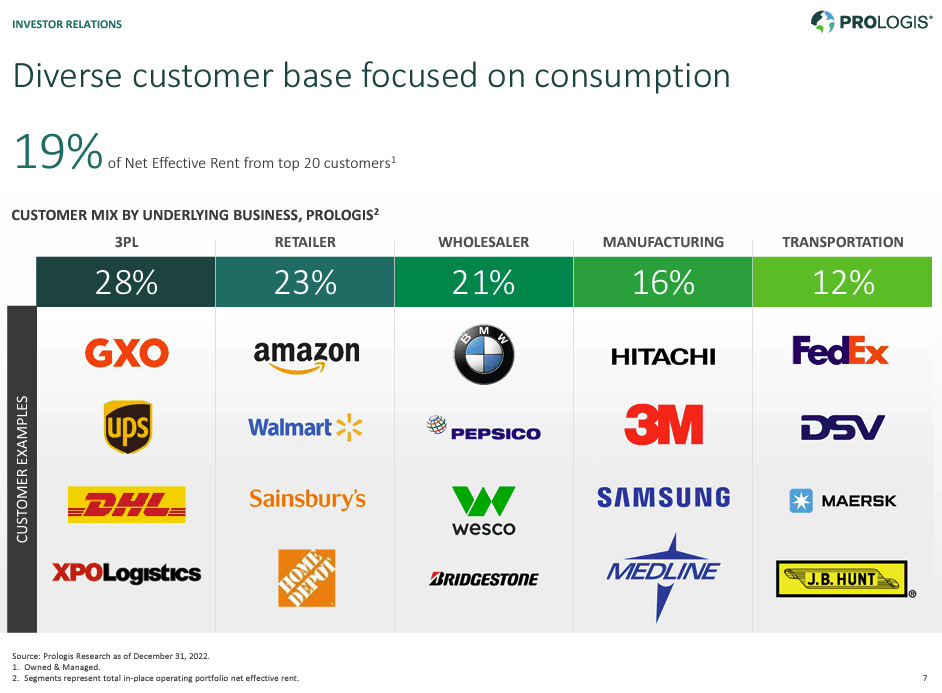

PLD has a various tenant base, which incorporates each e-commerce giants like Amazon (AMZN) and brick-and-mortar outlets like The House Depot (HD), in addition to third-party logistics suppliers corresponding to UPS (UPS). Even though third-party logistics is the highest revenue-generating phase for PLD, it handiest contributes to twenty-eight% of its overall revenues. Conversely, the transportation phase, which represents the smallest phase, contributes 12% of the overall revenues. PLD’s diverse tenant base is helping to cut back dangers related to tenant focus, thus making sure a extra solid and protected trade setting.

Corporate presentation

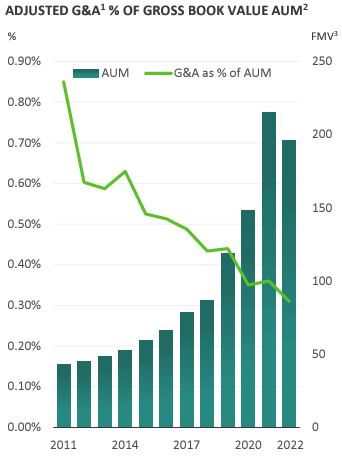

PLD has skillfully applied its strategic capital investments to spice up its scale and generate sustainable, long-term money flows. PLD’s strategic capital trade phase, which is most commonly composed of perpetual long-term ventures, provides further profit streams thru asset leadership charges, incentive charges, and belongings management-related charges. Over the last decade, PLD has constantly expanded its AUM, which recently stands at 196 billion, producing 844 million in FFO, with 47% of the profit coming from routine charges.

Corporate presentation

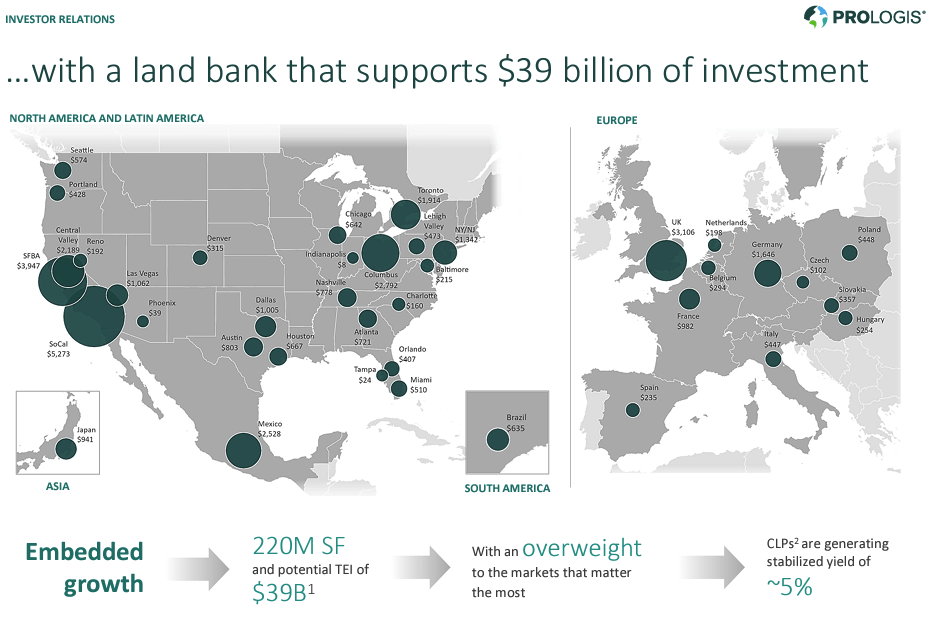

PLD has a powerful building pipeline, with tasks anticipated to yield round 5% which is subsidized through its strategically situated land financial institution.

Corporate presentation

Weaknesses: Restricted pricing energy

A weak point now not explicit to PLD, however moderately the business, is the fragmented and commoditized nature of the field with low obstacles to access and brief hire periods. This boundaries PLD’s pricing energy as commercial amenities are steadily regarded as commodities with a lot of substitutes to be had in key distribution hubs.

Alternatives: E-commerce

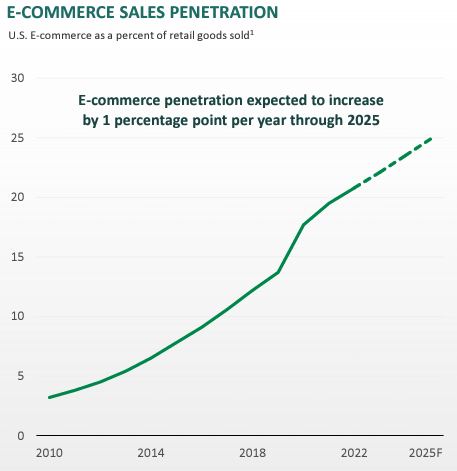

The secure enlargement of e-commerce is fueling the desire for warehouse and distribution area. To position this into point of view, each $1 billion build up in e-commerce gross sales calls for an extra 1.25 million sq. toes of distribution area to maintain this enlargement.

Corporate presentation

Threats: Inflation, rates of interest, vertical integration, and global political tensions

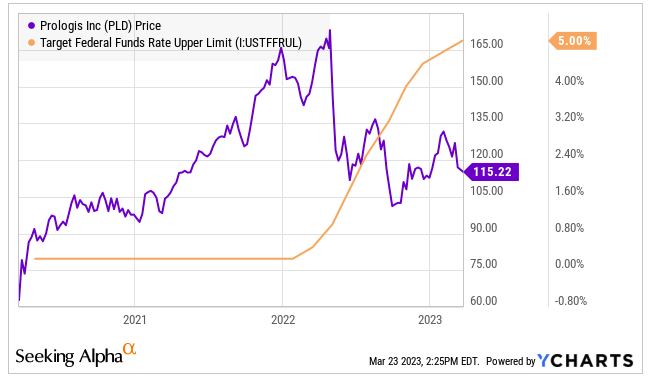

The opportunity of expanding rates of interest and inflationary pressures items a possible possibility to shopper spending, which might in the long run scale back call for for commercial area. In truth, the Federal Reserve raised rates of interest through 1 / 4 level these days, as a part of its efforts to struggle top inflation whilst additionally addressing monetary steadiness dangers. Markets are expecting an build up in each inflation and rates of interest because of emerging commodity costs and rising issues of financial overheating.

Ycharts

Additionally, a few of PLD’s main purchasers, corresponding to Amazon and FedEx (FDX), have made important investments in their very own distribution and logistics, which might doubtlessly lower their reliance on third-party logistics suppliers like PLD.

Moreover, PLD’s expansive international presence makes it extra at risk of global political and industry tensions than a few of its home competition.

Valuation

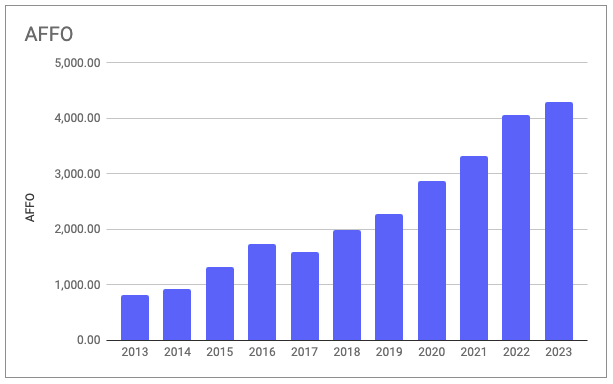

Since 2013, PLD has demonstrated an excellent 19.5% CAGR in AFFO, emerging from 820 million to 4.1 billion in 2022.

Writer estimates & corporate filings

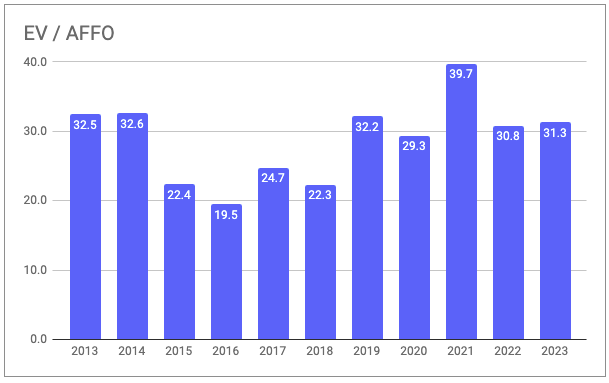

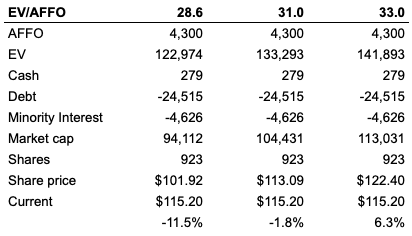

Whilst I await medium-term AFFO enlargement of five% to six% pushed through PLD’s building pipeline, I imagine the marketplace is recently pricing in quite upper enlargement expectancies. In response to my projections, I await AFFO to extend through 6% to 4.3 billion in 2023, ensuing out there valuing PLD’s stocks at 31.3x 2023’s AFFO.

Writer estimates, In search of Alpha & corporate filings

Then again, in an atmosphere of emerging rates of interest, it’s much more likely that the marketplace more than one will revert to the ancient reasonable of 28.6x moderately than enlarge any more. Due to this fact, I’d counsel conserving off on buying PLD’ stocks till extra horny access issues turn into to be had.

Writer estimates, In search of Alpha & corporate filings

Conclusion

PLD is a number one participant within the commercial actual property marketplace, boasting a limiteless and diverse portfolio of top-tier logistics and distribution amenities throughout other places. PLD’s sturdy monetary efficiency, strategic capital investments, and promising building pipeline make it well-positioned for long term enlargement. Then again, the character of the economic actual property marketplace limits pricing energy because of its fragmented and commoditized construction. Moreover, attainable dangers, corresponding to inflation, rates of interest, vertical integration, and global political tensions, may have an effect on PLD’s long term efficiency.

Given the potential of rates of interest emerging, it’s much more likely that the marketplace multiples for PLD will go back nearer to ancient averages as an alternative of increasing additional. Due to this fact, I like to recommend looking ahead to higher access issues.

Editor’s Observe: This text discusses a number of securities that don’t industry on a big U.S. alternate. Please take note of the hazards related to those shares.